Global Economic Perspective: November

Conditions Appear to be Coming Together for Fed Rate Rise

Steady improvements in US employment and relatively good economic growth figures mean that debate over when the US Federal Reserve (Fed) will begin to tighten policy continues to be the order of the day. US job growth increased at a fairly brisk pace in October, and numbers for the previous two months (already good) were revised higher. Since the start of 2014, US employers have added more than 220,000 workers on average each month, which should be sufficient to sustain economic momentum after an initial reading showed annualized gross domestic product (GDP) growth of 3.5% in the third quarter. Job gains mean the slack in the labor market is being steadily absorbed and is showing up in an unemployment rate that fell to a fresh six-year low of 5.8% in October. The latest figures supported a decision by the Fed in an end-October policy statement to change its characterization of labor market slack from “significant” to “gradually diminishing.”

In recognition of the improving US economy, the Fed announced the end of its two-year government- and mortgage-bond buying program in October. Yet, for the policy doves, there are still plenty of reasons for the Fed to remain cautious about tightening monetary policy. Despite the strengthening labor market picture, wage growth has remained tepid, according to the Bureau of Labor Statistics (BLS), with average hourly earnings for private-sector workers up just 2% in the 12 months to end-October, just above inflation. And while the labor force participation rate picked up slightly in October, it was still well below the levels seen before the financial crisis. Inflation has also been subdued, with the core personal consumption expenditures price index persistently coming in well below the Fed’s target rate of about 2% for over two years now (the rate was just 1.48% in September). Nor is economic growth necessarily as strong as the initial reading for the third quarter might suggest. Due in part to the steady rise in the value of the US dollar, the US trade deficit widened significantly in September, according to the Commerce Department, which may lead to a downward revision in the 3.5% GDP number for the third quarter. Just as important are the uncertainties hanging over the global economy.

But there are answers to most of these points. The participation rate should be expected to be lower than it was because of population aging. As for tepid income growth, statistics from the BLS’s latest report on productivity and costs, released on November 6, indicated that “hourly compensation” in nonfarm businesses rose at a healthy annualized rate of 3.3% in the third quarter. While still somewhat tepid, the BLS’s employment-cost index, a broad gauge of wage and benefit expenditures, rose for the second straight quarter in the three months to end-September. Just as significantly, many Americans are feeling a “wealth effect” that comes not just from rising prices for real estate and financial investments but also, and more immediately, from the sharp drop in oil prices since June. The combination of these factors, along with strong jobs growth, could, we think, spark a significant increase in consumer demand in the months ahead. Therefore, we continue to believe there is a possibility that US interest-rate increases could come faster than the market has been forecasting until recently, although the Fed’s resolve not to stymie the domestic recovery at a time when inflation is so tame could mean that any increases in base rates are small and gradual. A slow and cautious approach to hikes in base short-term rates could also avoid a rise in long-term rates to a level incompatible with the nation’s nominal potential growth.

Apart from monetary policy debates, elections on November 4 saw the Republicans take control of both houses of Congress. Although some observers fear the specter of a further dose of political brinkmanship of the sort that led to the brief shutdown of federal government services in 2013, other observers believe there is room to hope that an outgoing president keen to leave his imprint and a Republican party always considered close to business could lead to headway in areas such as trade and energy policy—and even corporate taxation—that could go some way to sustaining growth in the United States.

Japan Makes Aggressive Attempt to Boost Inflation

At the end of October, Japanese policymakers announced two unprecedented stimulus measures with global implications, boosting the price of Japanese “risk” assets.

In the first announcement, the Bank of Japan (BOJ) voted to expand its annual Japanese government bond (JGB) purchases to ¥80 trillion ($726 billion) up from ¥50 trillion. At the same time, the BOJ also decided to buy longer-dated government bonds of seven to 10 years’ maturity, instead of six to eight years. The announcement also removed the previous two-year time limit on quantitative easing (QE) and broadened the range of asset purchases to include exchange-traded funds (ETFs) and real estate investment trusts (REITS). This increased QE, in our view, is not only necessary to boost inflation and stimulate growth, but also to finance the Japanese government’s massive stock of debt and ongoing fiscal deficits—Japan’s debt-to-GDP ratio stood at over 200% at end-2013, according to International Monetary Fund estimates.1

| Change in Size of BOJ’s Balance Sheet (in Japanese yen trillion; tr) | |||

| 2013 | 2014 (forecast) | Planned annual increase* | |

| Monetary base | 202.0 | 275.0 | + 80 tr |

| Long-term JGBs | 142.0 | 200 | + 80 tr |

| Commercial paper | 2.2 | 2.2 | - |

| Corporate bonds | 3.2 | 3.2 | - |

| Exchange-traded funds (ETFs) | 2.5 | 3.8 | + 3 tr |

| Japanese real estate investment trusts (JREITS) | 0.14 | 0.18 | + 90 bn |

| Total assets | 224.0 | 297.0 | |

| *Based on the planned expansion of the monetary base announced by the Bank of Japan on October 31, 2014.Source: Bank of Japan, October 2014. | |||

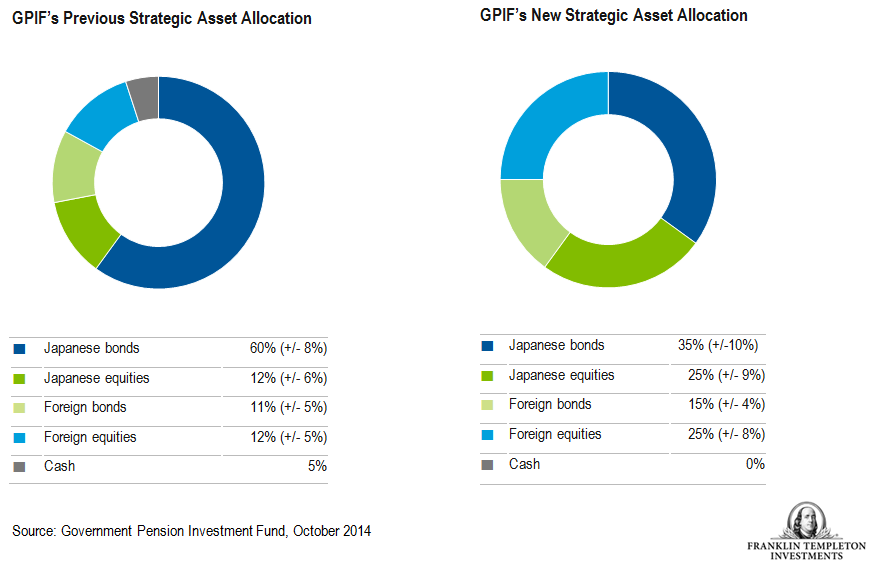

The second announcement came from the Government Pension Investment Fund (GPIF), the world’s largest pension fund with assets of $1.16 trillion, on October 31. The GPIF announced its decision to implement a more international investment strategy, intended to help Japanese retirees earn higher returns compared to those from JGBs. Specifically, the GPIF stated that it would reduce its domestic bond allocation from 60% to 35% of total assets while increasing its overall allocation in global bonds, as well as domestic and global equities. Given Japan’s persistent deflation, the marginal nominal yields of JGBs probably did not worry pensioners. However, as the BOJ aggressively targets a boost in inflation to 2%, we believe the GPIF’s decision to invest in a wider variety of non-JGB assets could not have come at a more pertinent time. Other Japanese pension funds are likely to follow the GPIF’s lead by internationalizing their investment parameters, which would likely further boost asset prices outside Japan.

The aggressive moves unveiled on October 31 increase the BOJ’s influence on Japanese financial markets, with its annual purchases of assets set to equal about 15% of Japan’s GDP—its balance sheet relative to its economy will dwarf that of other central banks, like the Bank of England and the Fed, that have also implemented QE. Overall, the BOJ’s continued quantitative easing supports our long-held views regarding the likelihood of downward pressure on the yen and that fears of a global liquidity crisis have been overstated. Recall that quantitative easing is one of three core components, or “arrows,” in Japan’s policy known as “Abenomics.” The other two arrows are fiscal consolidation and structural reform to enhance growth. In our view, only the first arrow, quantitative easing, is being fully utilized and effectively implemented. Implementing the other two arrows has proved both politically and socially challenging, so more emphasis is likely to be placed on quantitative easing for Abenomics to be effective. The combined pressure from Japan’s debt financing and the reliance of Abenomics on quantitative easing should motivate the BOJ to continue to provide global liquidity, given the end of the Fed’s asset purchase program. And such liquidity is not likely to remain in Japan—we believe it will spread globally, with emerging markets as the likely recipients.

European Outlook

Some very tentative signs that the eurozone economy might be stabilizing at a low ebb have started to emerge. A European Commission survey of economic sentiment in the eurozone rose in October, in part because of falling oil prices and the boost to exporters from the euro’s ongoing decline, while German industrial production bounced back in September, following a sharp drop the previous month, and French GDP growth, while feeble, was better than expected. But the eurozone is not out of the woods yet, and while the occasional positive data points have emerged, the mood appears to remain somber. October’s annual headline inflation rate of 0.4% remained far below the 2% target set by the European Central Bank (ECB), meaning that deflation is still a threat. Indeed, whileheadline inflation rose slightly in October, the core rate of inflation fell (from 0.8% to 0.7%), an indication that the weakness in prices that had been concentrated in energy and food has spread to other goods and services, while inflation expectations have fallen significantly. The ECB itself now expects that consumer prices will have increased by just 0.5% this year and will rise a feeble 0.8% in 2015, which would be well down from its September forecast of 1.1% inflation in 2015.

The low expectations for eurozone inflation are amply justified by the growth outlook. Quarter-over-quarter growth for some of the European high-fliers has begun to stutter. Spanish growth slowed to 0.5% in the three months through to end-September from 0.6% in the previous three months, while in the United Kingdom, growth slipped from 0.9% to 0.7%. The drop in activity in Germany has been even steeper: Quarter-over-quarter GDP growth of 0.1% in the third quarter meant that the country barely avoided recession (defined as two consecutive quarters of negative GDP growth). Taking cognizance of Germany’s reduced prospects, the European Commission cut its growth forecast for Germany in 2015 from 2% to 1.1%. But the Commission also cut its growth forecasts for the other eurozone heavyweights as well given German weakening and the failure of the Italian economy to pull out of long-term decline. (Astonishingly, Italy’s GDP in the third quarter had retreated to the level it was at in 2000). All in all, the Commission’s autumn forecast now sees eurozone growth of only 1.1% in 2015, down from the 1.7% growth it penciled in its spring forecast. A composite purchasing manager index (PMI) reading for October supported these downbeat predictions. It picked up less than market expectations, and the sluggish PMI number was generated in spite of much price-cutting, with a sub-index of output prices slumping to its lowest reading since February 2010.

| Year-over-Year GDP Growth Rates (in %) in Select EU Economies | ||

| 2nd Quarter 2014 | 3rd Quarter 2014 | |

| Eurozone (18 countries) | 0.8 | 0.8 |

| European Union (28 countries) | 1.3 | 1.3 |

| Germany | 1.4 | 1.2 |

| France | 0.0 | 0.4 |

| Italy | -0.3 | -0.4 |

| Spain | 1.3 | 1.6 |

| Greece | 0.4 | 1.4 |

| United Kingdom | 3.2 | 3.0 |

| Poland | 3.4 | 3.4 |

| Source: Eurostat, November 14, 2014. | ||

Yet one can find small silver linings to these latest developments. Even though the details remain frustratingly vague, economic sluggishness is lending some urgency to European Commission plans to launch a €300 billion investment drive, for example. Along with better-than-expected growth in France, activity in crisis-ridden Greece accelerated in the third quarter. And the slowdown in growth in Germany could lessen German policymakers’ resistance to straight purchases of government bonds by the ECB. Indeed, on November 6, ECB President Mario Draghi felt bold enough to say that the central bank was actively preparing to deploy further unconventional tools, including quantitative easing, should economic conditions deteriorate and that the bank was unanimously committed to expanding its balance sheet “towards the dimensions it used to have at the beginning of 2012,” which implies a balance sheet level up to €1 trillion higher than today. (Since July 2012, the ECB’s balance sheet has declined from a little less than €3.2 trillion to about €2.2 trillion.)

So far, the ECB has spurned QE, preferring instead to launch a series of technical measures that are precisely targeted at specific blockage points in financial markets and waiting to see the effect before attempting anything more radical. Thus, this year, it has launched a new program of cheap, medium-term loans for banks and has begun to purchase covered bond and asset-backed securities. Quantitative easing, as Draghi has hinted, is the logical next step. But would what is contemplated really be a game- changer? The possible effects on asset prices might spill out to the wider economy, but there is reason to doubt that government bond purchases in the eurozone would have a huge effect when interest rates are already so low. And a commitment to pumping up the ECB’s balance sheet to 2012 levels still seems pretty cautious when set beside the hugely expanded asset-buying program announced by the BOJ.

Perhaps it is more interesting to focus on the sometimes painful slog toward structural reform being undertaken around continental Europe. Spurred by economic stagnation, reforms are ongoing in competition policy, labor markets, pensions and the approach to regulation. The pace of reform varies from country to country, and we think patience will be needed before the results are seen in the form of falling unemployment and stronger growth (except in Spain, where labor-market reform has already helped achieve a marked turnaround in the country’s fortunes). Both of the eurozone’s big problem cases, France and Italy, are under the leadership of young, resolute prime ministers and would seem to be making some progress in overhauling their tired economies. However, while there are grounds to believe that Europe has the potential to make up lost ground, there are still plenty of reasons for Europe’s short-term prospects to be dim.

© Franklin Templeton

http://us.beyondbullsandbears.com

© Franklin Templeton Investments