Risk Parity: Comparing the Objections With Reality - Part 2

As the use of risk parity has grown, so have criticisms against the approach. In this blog series, I look at objections I’ve heard about risk parity, and explain why we believe they do not apply to our risk-parity approach — the Invesco Balanced-Risk Allocation strategy.

Our first post discussed why we first consider economic outcomes when building our strategic allocation. Below, we examine some important details of our allocation process.

Risk is more than just volatility

In general, risk parity is an asset allocation strategy that seeks to build portfolios in which each asset class — such as stocks, bonds and commodities — contributes an equal amount of risk to the overall portfolio. Several commentators have made the point that risk parity ignores returns and valuations. While this can be true in certain circumstances, it is not in ours.

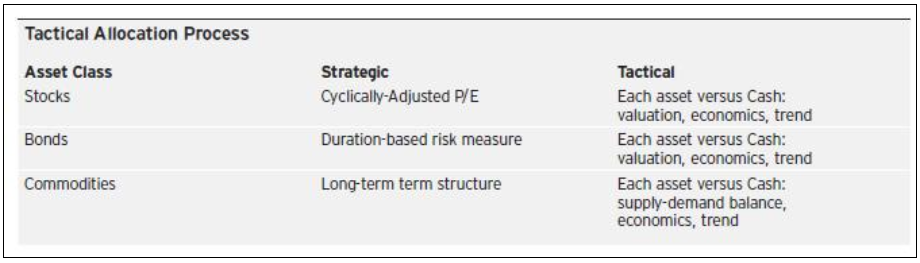

In our strategy, we consider a variety of factors to help determine the attractiveness of each asset relative to cash over time, rather than simply using historical volatility as the sole measure for assessing and allocating risk across assets (which is the approach that’s criticized in many risk parity critiques.)

- Bonds: Modified duration1 has supplanted volatility as the means to determine our overall weight to bonds. Duration is also used to determine the relative weighting across bond markets. We also employ a credit risk assessment to sovereign debt markets.

- Commodities: The shape or term structure of commodity futures curves is used to determine the exposures and weighting to those exposures we desire before volatility is considered.

- Equities: We use historical volatility2 to determine our weight to equities; however, we also apply a valuation metric to determine the relative weighting across equity markets. This reduces the dependency on historical volatility as an assessment of future risk.

Our expanded set of risk factors can be viewed as a reflection of return expectations. For example, our use of duration as a measurement of bond risk means that higher yields lead to a higher bond weight, all other things equal. Similarly, when evaluating equities and commodities by our enhanced risk measures, the worst-ranked have historically had poor future returns.

Also in our strategy, we have the flexibility to make tactical adjustments to the risk-balanced portfolio in an attempt to take advantage of market cycles in the near term.

In conclusion, we encourage investors to consider the specifics of their investment strategies, as they can deviate meaningfully from their common, broad-brushed descriptions. Whether it’s the asset selection process or estimates of volatility, differing approaches can have material impacts on investors’ risks and rewards. Despite the increasing scrutiny given to risk parity strategies of late, we believe our approach provides a research-driven robustness that may provide investors with consistent, risk-adjusted returns over time.

Important Information

1 Modified duration measures the rate of change of price with respect to yield.

2 Historical volatility is measured by standard deviation of the equity markets in which we invest, represented by the S&P 500 Index, Russell 2000 Index, FTSE 100 Index, Eurostoxx 50 Index and Hang Seng Index.

P/E (price-to-earnings ratio) measures a company’s share price versus its earnings per share.

Under normal conditions, the strategy invests in derivatives and other financially linked instruments whose performance is expected to correspond to U.S. and international fixed income, equity and commodity markets. However, the performance of the asset classes cannot be guaranteed.

Diversification does not guarantee a profit or eliminate the risk of loss.

Commodities and futures are volatile a may not be suitable for all investors.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

Before investing, investors should carefully read the prospectus and consider the investment objectives, risks, charges and expenses.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2014 Invesco Ltd. All rights reserved.