The Beginning of the End of the Fossil Fuel Revolution (From Golden Goose to Cooked Goose)

General Thesis

The quality of modern life owes almost everything to the existence of fossil fuels, a massive store of dense energy that for 200 years had become steadily cheaper as a fraction of income. Under that stimulus, the global economy grew ever larger, more complex, more inter-related and, I believe, more fragile. Then around the year 2000 the costs of finding oil start to rise at over 10% a year, and with the global economy growing at only 4% oil starts to fall behind in affordability. Oil has a leading role in the cost structure of agriculture and extractive industries, including coal, and dominates transportation. Because of that its affordability seems to determine economic progress far more than coal or natural gas. As its cost of extraction rises, other parts of the complex economic system have to be sacrificed to retain the ability to acquire sufficient oil. In those conditions, economic growth rates have to fall, and if oil costs continue to rise the trade-offs become more and more painful. Our complex system has been trained by experience to deal with steady growth. Now it must deal with slowing growth and one day it may face contraction. In this changed world we can only guess how robust the stressed system will be. We may hope it will be tough but quite possibly it will be brittle. At the extreme it might even threaten the viability of our current economic system.

It is vital therefore, if we want to reduce these stresses, to emphasize fuel efficiency, reduce wastage of all kind, and encourage the rapid development of sustainable “alternative” forms of energy, particularly those that displace oil. These alternatives are competitive today with only very high-cost fossil fuels but in 20 to 30 years, if encouraged, may replace $40 or $50 barrels of oil, at which price the global economic system may muddle through. Unfortunately, this target is hindered by the fossil fuel industries, which actively oppose incentives for alternatives.

As a sign of the immediacy of this problem, we have never spent more money developing new oil supplies than we did last year (nearly $700 billion) nor, despite U.S. fracking, found less – replacing in the last 12 months only 4½ months’ worth of current production! Clearly, the writing is on the wall. It is now up to our leadership and to us as individuals to read it and act accordingly.

Discussion

The Historical Importance of Coal and Oil

The epic spurt of growth that began for Europe and the U.S. around 1800 (before which global growth had been negligible for thousands of years1), was fueled by coal and then oil. The driver of this growth was the massive gap between what the energy was worth in terms of horsepower and human power equivalents and the much lower cost of digging or drilling the fuels out of the ground. Just imagine, for example, that you had to cut your winter wood supply in a hurry and you had to choose between paying your local labor a respectable minimum wage of, say, $15 an hour or filling your empty chainsaw with a gallon of gas. One of my sons, a forester, tells me he could cut all day, 8 to 12 hours, with a single gallon of gasoline and be at least 20 times faster than strong men with axes and saws, or a total of 160 to 240 man hours of labor. For one gallon! So for this task an estimate of value of $2,400 to $3,600 a gallon would be about right. But with gasoline at $3 a gallon we trade way down to trivial tasks with little labor equivalent value because we can, squandering the great potential value that oil has for really important jobs. That’s how we do it. We assume the oil or coal, our finite and amazing inheritance, is free and price it just at its extraction cost plus a profit margin. So at the important end of the spectrum gasoline or oil is worth, say, $3,000 a gallon and at the wasteful, trivial end is worth $3. This example used gasoline, an expensively processed part of a barrel of crude oil, but the same principle of a large gap between value and cost of course also applies to crude. Let’s work with that assumption for a moment. In 1998 the price of oil hit a 20-year low of below $14 a barrel and I assume the average cost was about $10 given there was still quite a bit of very cheap Middle Eastern oil in the mix. But the value might well have been as high as $2502 in which case a “massive surplus” – or beneficial gap between cost and value – of $240 would have existed, or 24 times the cost of extraction.

This surplus goes in part to governments as taxes, in some oil-producing countries virtually carrying the budget on its back. It goes as pay to oil workers and their support infrastructure. It goes as profits to oil companies and from them out to dividends. But above all, its greatest benefit is in those uses that have a far higher value than the cost of the fuel, as is the case with my son’s chainsaw. The great size of this surplus, first for coal and then oil and gas, drove the industrial revolution. The giant leap in wealth facilitated a massive increase in the science and engineering worlds. If you doubt the driving force of this surplus, revisit for a moment my earlier effort at imagining a world without fossil fuels (“Time to Wake Up,” April 2011 Quarterly Letter, page three). Somewhere around 1850 we would have rapidly run out of wood, the predecessor fuel to coal. Wood was used for ships, homes, tables, and wagons but above all it had two irreplaceable and vital uses: charcoal for making steel and power for steam engines and heating. By 1900 wars would have been fought over forests, and the population – without oil-intensive agriculture, both for growing and transportation – would have peaked out probably well under two billion and our species would indeed have had its nose pushed up against the limits of food. (Those who assume the key factor in our growth was the steam engine miss the point: without coal, the steam engine would have just hurtled us toward the depletion of wood far faster than was already happening. The Industrial Revolution was based on coal as the source of energy and the steam engine as the original way to exploit that energy as the efficiency level rose from 1% to 35% over the steam engine’s first 100 years.)

Thus we owe almost everything we have had in the way of scientific and economic progress and the growth of the world’s food supplies and population to fossil fuels. And not simply to the availability of these fuels, but more precisely to the availability of those fossil resources that could be captured extremely cheaply. From 1870 to 1970 technological improvements in finding oil offset the naturally rising marginal cost effect that you drill the best and cheapest prospects first. The price was always volatile but stayed around a trend of $16 a barrel in today’s currency. During this time, though, Americans became six times richer so that they could afford very substantial increases in energy, which drove the size and complexity of the economic system.

Rising Oil Costs Begin To Squeeze the Economy

Starting around the year 2000 a remarkable change in the relationship between oil and the economy began: the growing demand for oil started to outrun the supplies of cheap reserves and the economy had to adjust by bringing in the higher and higher cost reserve so that marginal costs compounded at over 10% a year. Why the price of oil inflected around the year 2000 so sharply, from stable to rising, is not clear but certainly owes a lot to a growing world population and perhaps a lot more to rapid Chinese growth. Marginal costs, which usually determine price, rose from $15/bbl or so in 1998 to around $70 to $90/bbl today. (And average costs rose from about $10 to $60/bbl.) This has subtracted about $50 from our invaluable surplus. On my numbers – and it is the principle here that is more important than the accuracy of the numbers, which in any case can only be guessed at – the surplus dropped from $240/bbl to $190/bbl. This 21% drop in surplus has no effect at all on high value uses like my son’s, but it drives out of business a $50/bbl band of less valuable uses of oil, which acts as an important drag on economic activity. (On a less abstract basis, a $50/bbl loss amounts very roughly to $1,000 per person per year in the U.S.) The price of oil is such an important input into the cost of all other resources that as oil more than quintupled between 1999 and today, the price of almost all other resources doubled and, for a while up to 2011, tripled (all adjusted for inflation). If it’s true that oil’s economic surplus has accounted for so much of our growth, then what we should have seen since about 2004 as the price of oil began to break out way over its long-term trend was some grinding of the economy’s gears: a persistent seeming reluctance on the part of the economy to live up to expectations. And this, in my opinion, is precisely what we have seen: a broad and increasing tendency for all countries to disappoint compared to their earlier growth rates. This should be no surprise, for every previous example of surges in oil price had the same effect. What is different this time, though, is that the damaging effects of the rapid price rises in oil and other resources up to 2008 in the U.S. have been misascribed as solely the result of the financial collapse. Being a believer in real things – people, education, training, motivation, and machines and buildings – and considering oil and its energy to be very real indeed, I believe that the financial paper losses are much less consequential than others do and that the resource squeeze on the economy is much more important. The apparent value of paper can disappear into thin air easily enough, as we have seen, but people do not, nor do machines. But the same worker, with only half a gallon of gasoline in his chainsaw because of increased cost will simply have a lower output. The efficiency of energy usage increases at about 1.5% a year, but if the price of finding and delivering oil continues to rise at a faster rate than that, then the squeeze on global growth rates will continue to tighten.

Consequently, I think that the old growth rates in productivity will not come back, at least until we have had a transition away from fossil fuels. Even that transition is not in itself enough. The latest solar and wind are indeed competitive already in ideal locations, but with what are they competitive? They are not replacing our old oil that cost $10/bbl on average 15 years ago. They are at the moment only outcompeting the highest cost fossil fuels so that the new energy sources are absolutely not remedying the painful loss to our energy surplus. What is needed is a continuing steady drop in the cost of alternatives for another 20 or more years before the surplus they offer has any chance of equaling our old, 1950-2000 fossil fuel surplus. Fortunately, a continued steady decline in the cost of wind power is likely, and a rapid decline in solar and energy storage costs is almost a certainty.

The challenge for our economy is to speed up this energy transition and to try and minimize, in the interim, the damage to our global economy and, possibly more importantly, to the actual viability of several poor countries, which suffer under the combined impact of rising fuel costs and their associated rising food costs. In some critical cases like Syria and Sudan, these cost increases are exacerbated by rapidly worsening climate extremes. Even if we can make the transition to renewable electric power smoothly, other challenges to reducing carbon emissions remain, especially in transportation, which is where the great majority of the rest of oil goes.

Because of oil’s dominant role in the cost structure of agriculture, mining, and, particularly, transportation, cheaper coal and gas have historically not materially blunted the pain from increases in the affordability of oil in developed countries. Only in some emerging countries with large coal reserves is there some reprieve, and even there as their economies mature and transportation takes on a larger share, as in China today, their sensitivity to oil increases.

U.S. Fracking: the Largest Red Herring in the History of Oil

First, let us quickly admit that U.S. fracking is a very large herring. Its development has been remarkable. It will surely be seen in the future as a real testimonial to the sheer energy of American engineering at its best, employing rapid trials and errors – with all of the risk-taking that approach involves – that the rest of the world finds so hard to emulate. Similarly, it will always stand out as remarkable proof that, so late in the realization of the risks of climate change and environmental damage, the U.S. could expressly deregulate such a rapidly growing and potentially dangerous activity. There are few if any constraints, for example, on what chemicals and in what amounts, can be pumped into a fracking well. Nor is the leakage of methane (natural gas) from the drilling and pipeline operations seriously monitored despite the fact that methane is over 86 times as potent a greenhouse gas, at a 20-year horizon, as CO2 is. This has given the U.S. industry a second spectacular advantage over more regulated fracking efforts elsewhere and demonstrated once again the remarkable influence of the energy industry over the U.S. governmental process, if “process” is not too dignified a word. Be that as it may, U.S. fracking produced – in addition to a lot of natural gas – almost four million barrels of incremental oil per day, not a barrel of which was in the official oil estimates eight years ago! This is very close to 100% of all the increase in global oil production in this time period and without it oil prices would obviously have been substantially higher than the recent Brent peak of around $115/bbl. Equally remarkable, U.S. oil production from fracking continues to rise and it seems likely to rise another two to three million barrels a day before topping out. Already today, partly because of continued very disappointing global economic growth, U.S. production is temporarily glutting the world market – storage is up and prices are falling. It is one of the ironies of this complex oil system that despite this unexpected gush of U.S. oil and the ensuing impressive current drop in oil prices, nothing that really matters in the long term is changed by U.S. fracking. Yes, it has produced most of the short-term kick to the U.S. economy that makes the U.S. look superior to others (although despite this help the U.S. economy, too, has been persistently below earlier estimates, including this year). It has also created a temporary oil glut and pushed down world oil prices. Yet what it has not done is more important, and that is what makes it a red herring. It has not prevented the underlying costs of traditional oil from continuing to rise rapidly or the cash flow available to oil-producing countries like Saudi Arabia, Iran, and especially Venezuela from getting squeezed from both ends (rising costs and falling prices) with potential political consequences that I will leave to others to speculate about. The same pressures will of course also expose those oil operators that have been borrowing amounts close to the total of their cash flows for, strangely indeed, the fracking sub industry in total does not clearly show much positive cash flow despite considerably higher prices over the last two years than exist today. Yes, they have been drilling more wells that chew up money, but not that many more, and good operations have lowered the costs per well by over a third. On the other hand, they have drilled, as always the best parts of the best fields first, and because the first two years of flow are basically all we get in fracking, we should have expected considerably better financial results by now. The aggregate financial results allow for the possibility that fracking costs have been underestimated by corporations and understated in the press.

Because fracking reserves basically run off in two years and can be exploited very quickly indeed by the enterprising U.S. industry, such reserves could be viewed as much closer to oil storage reserves than a good, traditional field that flows for 30 to 60 years. Fracking oil reserves could consequently be treated as our emergency reserve. In real life we are using it up as fast as we can. Let us hope that there will not come a time in 10 to 20 years when we will regret the absence of reserves that could be developed in a hurry. Meanwhile, cheap traditional oil, in contrast, becomes increasingly difficult to find both in the U.S. and globally. Last year for example, despite spending nearly $700 billion globally – up from $250 billion in 2005 – the oil industry found just 4½ months’ worth of current oil production levels, a 50-year low! Despite currently falling prices from a temporary glut that has exceeded storage capabilities, rising costs of finding and pumping traditional oil continues to put pressure longer term on resource prices. Because of this the global growth trend will be lucky to be over 3.5% with the developed world closer to 1.5% and both may well be less. The continued run of disappointing economic growth seems likely therefore to continue. Indeed, it is quite likely, although hard to prove, that any oil price over $40 or so has been putting sustained underlying pressure on global growth and that it did not take the spikes to $150 in 2008 and $115 recently to throw some sand in the works: the sand has been there since 2006 and is likely to stay there indefinitely or at least until alternatives provide very cheap energy under a $50 per barrel or so equivalent.

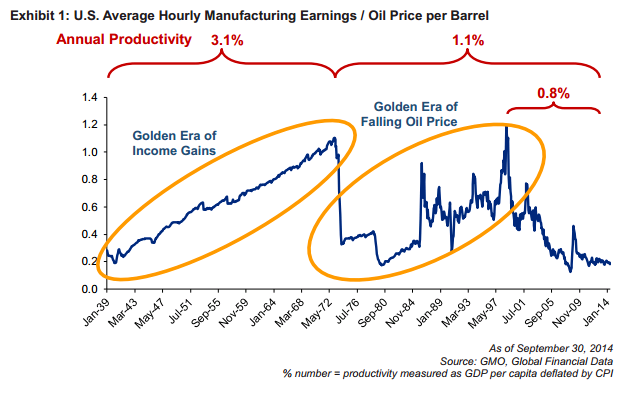

This is a good time to take a look at my solitary exhibit which is like a summary of the story so far. In 1940 as the Great Depression was ending, one hour’s work for an American engaged in manufacturing could buy 20% of a barrel of oil, or approximately eight gallons. Bearing in mind that a single gallon has the equivalent energy of 200 to 300 man hours of labor, this already seems like a small fortune, but in what I am calling “The Golden Age of Income” the affordability of oil increased so steadily that by the end of 1972, just before OPEC and the troubles in the Middle East began, one hour’s work controlled 1.1 barrels, over a five-fold increase, the greatest surge of real wealth in U.S. history. By the second oil shock of 1979, however, oil affordability was back at a new low. Next began a quite different leg up, far less smooth and this time driven by declining oil prices and despite increasingly modest increases in income per hour. A new high in affordability was reached at 1.2 barrels per hour worked at the astonishingly low price of $16 a barrel in 1999 at today’s dollar equivalent. The final leg that I have been obsessing about now for six years was the great decline in affordability from 1999 until today that took affordability of oil back precisely to where we began in 1940! This has been a remarkable round trip and what a lot it says about the preeminence of oil in our economy. When oil was becoming more affordable up to 1972 and oil intensity per person was still increasing, productivity per man hour grew at an unprecedented rate of 3.1% a year. From then until now as affordability fell and oil usage per person fell, productivity per man hour fell with it to 1.1%. This is not a small shift! 3.1% will take $1 to $21 in 100 years, where 1.1% will make it to barely $3. But to rub this point in, the productivity from 2000 to now has fallen to 0.8% a year at which rate $1 just about doubles in 100 years. (All calculations were done using GDP in nominal dollars deflated by the CPI, a number calculated by a government that always has a strong incentive to shave inflation down a bit here and there.) This data surely raises a strong likelihood that falling affordability of oil dominates our energy equation and poses a serious threat to income and wealth generation. At the very least the data is compatible with the thesis.

The Demise of Oil-burning Engines

Working in exactly the opposite direction to the rising costs of finding new oil is the accelerating progress in oil replacement technologies. Progress in electric vehicles (see January 2014 Quarterly Letter) seems to move faster by the month. Last November, a colleague and I personally witnessed a two-minute recharging of electric batteries (without any damage to the life of the battery). Interestingly, this was described to us a week later by a leading battery expert as being “against the laws of physics.” Considerably perplexed, we checked with the engineers who had achieved this two minute recharge to find that they themselves were not so sure of the physical principles involved. They had reached their goal by many thousands of intelligent trials and errors as engineers have probably done since the Stone Age, leaving it to future Nobel Prize winners to notice what had happened and then produce a theory. And more recently scientists have indeed theorized the possibility of rapidly charging electric batteries. (This is a field of research moving so fast that apparently even the laws of physics can’t keep up!) Then, in the spring of this year, a Japanese company, Power Japan Plus, announced similar rapid-charging capabilities, plus some attractive features that offer great potential cost reduction. There have also been several important breakthroughs announced in both the cost and efficiency of large-scale energy storage, notably in liquid metal batteries. If not unprecedented, this progress is definitely remarkable. We also heard from experts of automobile redesign from the ground up to produce ultra-lightweight “people movers,” and we followed the rapid progress of “autonomous” or self-driving vehicles. All in all it seems likely that in 10 to 15 years the gasoline engine will be in its death throes, and we can absolutely count on China riding the new technologies to the limit even while the vested interests in the U.S. fossil fuel and utility industries throw their usual wrenches into the machinery to try to buy themselves some time at society’s expense. But we will, I’m sure, eventually remove oil demand for surface transportation. As we do so, it will give our environment some breathing room – some more time for us to deal with the remaining important uses for oil and gas such as chemical feedstock, air and sea transportation, and road surfacing, which uses will take many decades to completely replace.

Oil Costs vs. Oil Prices (or Oil Profits get Crushed!)

In the long run, when the costs of producing oil rise, the prices will rise. But in the short run it is not always the case, and in such occurrences it is easy to confuse the effects of changes in costs with changes in prices. When global oil costs rise, as they are currently doing, global growth must suffer as we are forced to use more of our capital per unit of oil discovered and thus limit our capital investments in other growth opportunities. This is true even if prices simultaneously fall due to a temporary supply/demand imbalance. The current fall in price does nothing to offset the squeeze on the total economy from rising costs. It merely transfers massive amounts of income from one subgroup (oil producers) to another (oil consumers), in a largely zero-sum game. Oil consumers tend to spend more and save less than oil companies so short-term impacts are favorable. But we should not be carried away with enthusiasm because the declining investment from the oil industry will lower future growth. When, as now, oil costs are still rising even as prices fall there is of course a particularly savage effect on the profits of oil companies, squeezed from both ends. They must and will rapidly adapt by reducing expenditures and therefore oil production with the fairly obvious result that prices will rise again.

The only longer-term price relief and net benefit to the economy will come when either we reverse recent history and start to find more oil more cheaply, which will be like waiting for pigs to fly, or when cheaper sources of energy displace oil.

The Immovable Object and the Irresistible Force

What I’m trying to describe here is on one hand a remorseless and historically unprecedented rise in the costs of delivering oil to the marketplace, which is sapping economic strength globally, and on the other hand (and simultaneously) what will be the beginning of an accelerating transference of demand away from oil under the impact of surprising technological progress in alternative energy. When we add the further complexity of a temporary surge in oil from U.S. fracking, I am willing to concede that the outlook for oil and energy is the most complicated puzzle I have ever come across: it is wheels within wheels, but with each spinning in a different time frame. As Spock would say, “Fascinating!” How this ultra-complicated tug of war plays out in the next 10 years or so is anyone’s guess. My guess is that oil prices will bounce around for most or all of the next 10 to 15 years as first one side of this tug of war moves ahead and then the other, with perhaps another 2008-type spike (or two) in the price of oil, after which prices will plateau and decline as electric vehicles take over and, one by one, oil’s remaining uses are slowly replaced.

The story for coal is much simpler. Coal for coking in the steel business may last for decades (although very recent announcements out of MIT suggest that the need for coal may one day be bypassed), but steam coal, used almost exclusively for electric power, is already in a rapid and certain absolute decline in the U.S. and in a steady decline in its growth rate elsewhere. In China, which astonishingly accounts for over half of all current global coal consumption, it is unlikely that any material number of new coal plants will be built after 20 years and, quite possibly, 10 years. China is moving faster than most realize in this area and should be, given the extensive health damage from air pollution there. If this problem continues or worsens, it is likely to threaten the social contract between the Chinese people and their government, which seems well aware of this possibility. Natural gas, a fuel that is potentially much cleaner and potentially less environmentally threatening if leakage can be controlled, will last longer than coal in utilities, but not much longer. That said, as with oil, some other uses for natural gas, fortunately much smaller, such as feedstock for nitrogen fertilizer, will continue for decades. How quickly and smoothly this tug of war is resolved will determine how prosperous and stable our global society will be. Possibly, it will determine whether our currently successful global economy will be viable at all in anything like its present form.

P.S.

As a parting shot let me emphasize once again how out-of-it mainstream economics has been for the last several decades. Not only did the mainstream absolutely not see the financial crisis approaching, but it marginalized the work of Hyman Minsky, who did. More to the point, the economic mainstream has totally missed the significance of the limits on growth posed by finite resources and again marginalized the work of Kenneth Boulding and Nicholas Georgescu-Roegen and the writers of the original The Limits to Growth,3 who did. As with inefficient and corrupt market players in finance, they simply assume such limits away, in disregard of at least one of the laws of physics4 (that entropy rules and everything runs downhill, becoming less useful). This neglect of resources, like their last failure in finance, is likely to end very badly. Meanwhile, they try to define all of our problems in monetary, debt, and interest rate language, ignoring the real world of people and things. The economic establishment is letting us down again. Their report card should read, “Could do better!” Which brings me to my main P.S.

P.S. Two: Hysterical Malthusians and Hubristic Cornucopians

On the principle that there is no such thing as bad publicity, I must thank The Economist for mentioning (October 3, 2014) that I had pointed out three and a half years ago that the previous world of cheap and available commodity prices had gone forever. Reading between the lines, though, the view of The Economist is that concern over long-term commodity prices and availability is more likely to reflect hysterical Malthusianism than real life as they point to the recent impressive fall in almost all commodity prices. I had suggested originally that temporary drops in commodity prices could be caused by China growing less than expected or by weather for farming improving after several monstrously bad years. Both of these events occurred this year. However it has always been oil that matters most, for oil is half the value of traded commodities and almost half the cost structure of the rest. Oil, as described in this quarter’s letter, is currently very complicated but the key for the long term is the remorseless rise in the cost of producing the marginal, or extra barrel, that continues to rise even as U.S. fracking oil gluts the global market for a minute or two. Oil was $14 a barrel in 1998 and has now dropped to $83 from $115 (Brent). With costs of production at $60 or $70 a barrel, oil prices are not going back to $14 or even $40 (at least until renewables displace it more or less completely in a few decades). The weather for growing grain is of course mean reverting, but it is now unfortunately doing so around a steadily deteriorating trend. Rising grain prices are one of the greatest threats to global stability and it would be wonderful if there were a magic cure for the declining growth rate in the productivity of grain, soil erosion, water availability, and deteriorating long-term weather patterns but it just ain’t so.

As discussed in earlier quarterlies, three important commodities are really quite common in the earth’s crust: iron ore, bauxite, and potash. All other industrial metals and the critical phosphorus added together do not equal the least of those three! They are simply scarce and are being depleted, as is cheap oil.

The Economist is not a flamboyant, cowboy member of the Cornucopians – those who have the hubris to believe that the infinite human brain will always conquer all problems by divine right and will make all resources available forever, despite logic and the laws of nature – but they are part-time Cornucopians if you will. And they can still misuse the hoary old Simon-Ehrlich bet5, which extended to today is at worst a draw for Ehrlich and the last time I checked all the details it was a clear victory for him. (See Appendix A, attached, from GMO’s July 2011 Quarterly Letter.) It comes down to understanding the impossibility of sustained compound growth in finite resources and a finite planet and reminds me of one of my favorite quotes from one of my favorite economists (a very small group), Kenneth Boulding, who said, “Anyone who believes exponential growth can go on forever in a finite world is either a madman or an economist.”

Stop Press! The End of Normal by James Galbraith

Having labored over the eighth draft of this quarter’s letter on oil and energy in which I insult economists for their lack of interest in resource limitations, a new book appears that amazes me by doing the opposite, and by an increasingly well-known economist no less (although clearly not mainstream, thank heavens). It is entirely sensible from start to finish. Which is code for I agree with almost everything he writes. Galbraith claims, for example, that the resource price rise to 2008, especially for oil, played an important role in the economic setback and deplores the fact that nobody mentions this. Sadly, he is not a reader of my quarterly letters but, hey, nobody is perfect. Let me leave you with the advice to buy and read this book, along with this quote from page 104 (underlining added):

“There is no reason to believe that the democratic decision made by the living in the face of their present needs and desires will be the decision that would maximize the chance of long-term system survival. The unpleasant conclusion is that it is possible for a society to choose economic collapse.”

1 The Maddison Project estimates that U.K. growth from year 1 to 1800 was just .07% a year, with most of the world significantly lower.

2 This estimate is made by guessing what percentages of oil use are very high-value, low-value, and so on. From my rough work I believe the range is unlikely to be outside $200 to $400 a barrel.

3 Donella H. Meadows, Dennis L. Meadows, Jorgen Randers and William W. Behrens III, The Limits to Growth, 1972.

4 The Second Law of Thermodynamics.

5 The classic wager between Ehrlich (the Malthusian) who believed shortages would push up finite resource prices and Simon (the Cato Institute Cornucopian) who believed Technology would push their prices down forever.

Appendix A: Malthusians and Cornucopians: the Ehrlich-Simon Bet

While still on the topic of resources, there are a few points I’d like to make on the subject of the famous bet made between Paul Ehrlich and Julian Simon in 1980, which is so often mentioned by opponents of any ideas regarding resource limits. They have been called Cornucopians, which I think is a great term for them. Ehrlich believed that we were beginning to run out of resources; we might call him a Malthusian. He reflected the Club of Rome’s thinking and the famous book entitled The Limits to Growth.1 Simon on the other hand, who worked at the Cato Institute for many years, was a classic super-Cornucopian: everything will always be fine because of our species’ boundless resourcefulness; population increases are to be welcomed because they cause growth, which in turn stimulates invention so that there will always be plenty. The Cato Institute generally supports any theory that will result in less government and fewer restraints on corporations. (They were grubstaked by the Koch family, they of the hydrocarbon empire, who, not surprisingly, profoundly agree with those beliefs.) The argument that mankind might seriously endanger the long-term productivity of the planet by wasteful overconsumption or by unnecessarily large emissions of carbon dioxide is a dangerous “idea” for libertarians and Cornucopians (we might, I think, reasonably call such things “facts”) that might open the door to regulation. Ergo, the facts must be disputed. And every argument along the way, large or small, must be grimly defended, especially the ideal of limitless growth.

And defend it Mr. Simon did, and very effectively. He engaged Ehrlich in a bet on this topic, which he famously won, and the Cornucopians have never let anyone in this field forget it. The essence of the bet was that Ehrlich believed that compound growth could not be sustained in a world of finite resources, and therefore the real price of raw materials would rise. Simon argued that, regardless of the rate of growth, real prices would fall. Of course,the spirit of this bet has no time limit – 40 years is better than 10, and 100 is better than 40. But a bet like this between humans of middle age is one that both would like to collect on. So, the bet was set at 10 years and five commodities2 were chosen by mutual agreement. Here again, all commodities would have represented the spirit of the bet better than five, but five was easier to monitor. Simon won all five separate bets fair and square at the 10-year horizon. But let’s admit that this is a very unsatisfactory time period for the rest of us who are really interested in this contest of ideas. So, let’s take an equally arbitrary but much more satisfactory bet: from then, 1980, until now, and include all of the most important commodities. Simon would have lost posthumously, and by a lot! (Even of the original five, he is only one for five, having won the least significant of the five: tin.) So, please “Cornucopians,” let’s not hear any more of the Ehrlich-Simon bet, which proves, in fact, both that man is mortal and must make short-term bets, and, more importantly, that Ehrlich’s argument was right (so far).

1 Donella H. Meadows, Dennis L. Meadows, Jørgen Randers, and William W. Behrens, III, The Limits to Growth, Universe Books, New York, 1972.

2 Copper, chromium, nickel, tin, and tungsten.

Disclaimer: The views expressed are the views of Jeremy Grantham through the period ending November 2014, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2014 by GMO LLC. All rights reserved.

© GMO