GMO is often accused of being a “glass half empty” investor, and I admit that in a year that has seen the S&P 500 rise 8.3%, MSCI All-Country World rise 3.7%, and the Barclays U.S. Aggregate rise 4.1% through the third quarter, the words “Purgatory” and “Hell” are unlikely to come to mind to most investors when opening their brokerage statements. It has been a dull year, perhaps, but certainly not a hellish one. So what is bringing Danteesque visions of damnation into our slightly warped minds? As is often the case, our moods are driven far less by a look in the rearview mirror and more by what we see through the windshield. A little over a year ago, my colleague James Montier wrote about the current opportunity set for investors and referred to it as the “Purgatory of Low Returns.” He called it Purgatory on the grounds that we assume it is a temporary state and higher returns will be available at some point in the future. But as we look out the windshield ahead of us today, it is becoming clearer that Purgatory is only one of the roads ahead of us. The other one offers less short-term pain, but no prospect of meaningful improvement as far as the eye can see. At the risk of stretching this metaphor further than I should, I need to point out that we are merely passengers in this car, with no more ability to affect the road taken than my toddler when he exclaims that today we should drive to Legoland instead of pre-school.1 All we can do is shout from the back seat to the financial markets taking us on this ride to “Take the Purgatory exit! Take the Purgatory exit!” and cross our fingers.

And which road we take will be of more than theological interest. The two paths not only differ in their implications for the long-term returns to financial assets, but also in the appropriate portfolio to hold today and into the future. To skip to the punchline, if we are in Hell, the traditional 65% stock/35% bond portfolio actually makes a good deal of sense today, although that portfolio should be expected to make several percentage points less than we have all been conditioned to expect. If we are in Purgatory, neither stocks nor bonds are attractive enough to justify those weights, and depending on the breadth of your opportunity set, now is a time to look for some more targeted and/or obscure ways to get paid for taking risk or, failing that, to reduce allocations to both stocks and bonds and raise cash.

Mean Reversion and Fair Value

In this April’s note “In Defense of Risk Aversion” I wrote about how a belief in mean reversion would lead an investor to move his asset weights around by much more than they would in the absence of that belief. Here I’m not going to be talking about the general question “Do asset class prices mean revert?” but rather “What are prices going to mean revert to starting today?” While we use the phrase reversion to the mean a lot in describing our beliefs about financial markets, in reality what we believe is that asset class prices should revert to fair value. Fair value may or may not be approximately equal to the average of historical valuations, but we find it instructive to start with an analysis of historical valuations in trying to understand what fair value might be.

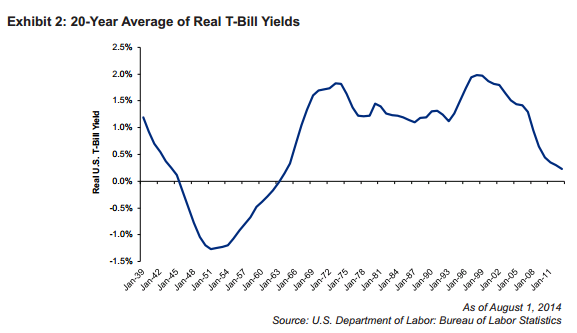

One of the toughest assets to get our brains around turns out to be cash. The real yield on U.S. T-Bills is shown in Exhibit 1.2

A real optimist could look at that chart and say that it’s pretty clear ex-ante real cash yields have been bounded somewhere between -2% and 4%. But -2% to 4% is an awfully big range, disappointingly big for anyone who is hoping to build fair values for other asset classes off of the returns available on the “risk-free asset.” There is a certain amount of cyclicality that one should expect for cash yields. The appropriate cash rate in a recession is significantly lower than what makes sense in an economic boom. And for figuring out fair value for long-lived assets such as equities, those cyclical shifts shouldn’t matter, only the long-term average. But no matter how much we smooth the yields to damp down the cyclicality, we are left with a problem, as you can see in Exhibit 2.

We’ve still seen rates bounce around from -1% to +2%, which is a very big deal for fair value estimates. To put it in perspective, if equities were to give a 4.5% risk premium above cash and expected long-term cash yields moved from -1% to 2% real, the fair normalized P/E on the stock market would move from 29 to 15. That is such a wide range as to be basically useless for anyone hoping to figure out when equities are worth owning. Implications for GMO Forecasts When we started building our asset class forecasts in the mid 1990s, we felt sufficiently confident that we knew where cash rates were going that we didn’t worry much about it. Somewhere around 1.5% to 2% over inflation seemed right, and we blithely ignored the low rates of the 1930s to 1950s as a combination of the very long cycle of the Great Depression and the confusion of investors who didn’t realize the important inflationary implications of going permanently off of the gold standard. But the events of the last 12 years or so call into question the confidence we used to feel in the level of normal cash rates. At our internal investment conference in September, we had a lively debate over “Secular Stagnation” – the argument, popularized by Larry Summers, that the developed world is suffering from a lack of aggregate demand that has driven the equilibrium cash rate far lower than it had been in the past 40 years. I wouldn’t say that the stagnation proponents decisively carried the day, but it was striking how little consensus there seems to be across the firm. The two basic camps were our current base case – real cash rates in the developed world will move to around 1.25% on average in the long run – and secular stagnation – cash rates in the long run would average around 0% real. The average response in the post-conference survey was 0.75% real with fairly close to half of the GMO investment professionals believing that rates were going to be close to zero real into the indefinite future.

And make no mistake about it, a world in which cash rates average 0% from here on out is a fairly hellish one. It is our belief that investors get paid for taking unpleasant risks. That compensation is in the form of a risk premium over the “risk-free” rate, and while there are no truly risk-free assets out there, T-Bills are a good enough approximation for many purposes. If that rate is going to be zero real, stocks, bonds, real estate, and everything else investors have in their toolkit should have their expected returns fall as well. In that world there are likely to be no assets priced to deliver as much as 5% real, and the expected return to a 65% stock/35% bond portfolio would drop from 4.7% real to about 3.4% real. Starting from 4.7% real, it’s easy to believe you can do enough smart things to get your portfolio to a return of 5% real or above. For the system as a whole, that belief is a delusion, as the average investor cannot hope to have above-average returns. But 0.3% of alpha is not so much to hope for as to seem irresponsible for an investment committee to expect. When you raise that 0.3% to 1.6%, it does start to seem implausible, particularly when you are thinking of it as not the “hoped for alpha” but the “budgeted for alpha.” This is where the difference between the market value of a portfolio and the ongoing spending it can support becomes a big issue. If we imagine for a moment that one could become convinced that the expected return to the standard portfolio has fallen from 4.7% to 3.4%, the ongoing spending that can be supported by that corpus has fallen 28%. This is, by an odd coincidence, the same effect as removing all of the gains from a 65/35 portfolio since September 2010. That is to say, the last four years of gains across the stock and bond markets look nice on paper, but have not increased the spending supportable from the portfolio.3 And while that may seem inconvenient enough for an entity that bases spending off of current wealth, the problem is much bigger for any entity who will be doing a chunk of their wealth accumulation in the future. If you are a 35-year-old worker who has another 30 years to go saving for retirement, the prepayment of future returns has been a real disaster, as all of your future savings will be accreting at a much lower rate. Such a worker will wind up with about 21% less in his retirement account than if prices had never risen in a way consistent with a 0% real risk-free rate forever. Compounding the problem (no pun intended) is the fact that a given pool of retirement savings can support less spending in a lower rate environment, making the effective shortfall more like 33%.

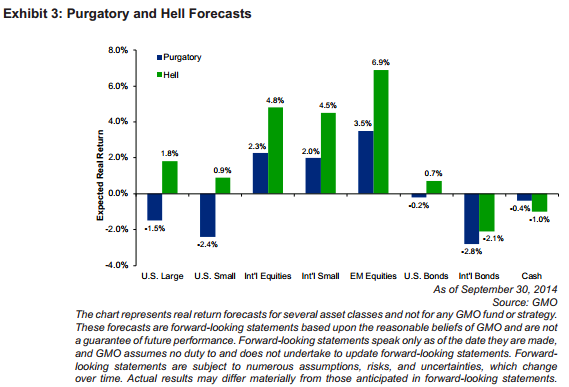

Pretty inconvenient for anyone saving for retirement. So we can all hope we aren’t on the road to Hell. But the other option, you’ll remember, wasn’t an immediate trip to Heaven, but a stay in Purgatory. So what is Purgatory, and is it really any better? The answer to that really depends on your time horizon. Purgatory would mean that cash rates will eventually go back up to more “normal” levels of around 1.25%, which means that the rest of the financial asset pyramid will go back to more normal expected returns as well. The bad news is that valuations will have to fall in order to get there, so if you are thinking about returns over, say, the next seven years, Purgatory is actually worse than Hell. Exhibit 3 shows our current seven-year asset class forecasts, which assume a Purgatory path, compared to the forecasts under the Hell scenario.

All of the forecasts (except for the cash forecast) are higher under the Hell scenario, because Purgatory requires a repricing of assets downward as cash yields rise.4 So for the next seven years, we’d be better off in Hell than Purgatory. But in the longer run, the calculus shifts. Our hypothetical 35-year-old worker will wind up with 15% more in his retirement account if we take the Purgatory road than if we head to Hell. That still leaves our worker 5% short of where he would have been had we never had the boom in the first place, but a 5% shortfall is a lot less of a disaster than a 33% shortfall is.

Portfolio Implications

So, for investors with a long time horizon, we can certainly hope that we go down the Purgatory path. But hope is not an investment strategy, and the trouble is that the right portfolio to hold today is pretty different if we go down the Purgatory path or Hell path. If Hell is our destiny, then both equities and bonds are a pretty decent hold today. The expected return to global equities goes from 0.5% real to 3.5% real – perhaps coincidentally, that 3.5% return is precisely a 4.5% return premium over cash. Meanwhile, U.S. bonds go from -0.2% to +0.7%, with the +0.7% a slightly greater than “fair” 1.7% premium to cash. In other words, if we are in Hell and we felt that 65/35 was the appropriate portfolio to hold if risk premia were normal, then we should hold almost exactly that 65/35 portfolio. If we are in Purgatory, the equity risk premium is +0.9% for global equities and +0.2% for bonds, a small fraction of the normal payment for taking stock and bond risks. How much less of equities and bonds to hold under that circumstance is a bit of a matter of taste, but it’s almost certainly a good deal less of both. For an investor operating with a constant aversion to risk, the 65%/35% stock/bond portfolio turns into a 20% stock/58% bond/22% cash portfolio, with an expected return of -0.1% real. No, that is not a typo. Running the same risk aversion that would get you to 65%/35% under “normal” circumstances says that the right portfolio to run today actually has an expected return less than inflation. Putting that in perspective, though, the 65/35 portfolio only has an expected return of +0.25% real, so you aren’t exactly giving up a stirring expected return for the sake of risk reduction. If we are actually in for Hell instead of Purgatory, the comparison is +0.9% real for the low risk portfolio and +2.5% real for the 65/35 version, which is a much more material give-up of 1.6% in expected return for the lower risk portfolio.

A Path to Redemption?

So, is there anything we can do other than hope we’re in Hell if we have a short time horizon and Purgatory if we are taking the long view? Maybe. One of the interesting implications of Hell is that the rise we’ve seen in asset prices over the last few years would have been a repricing of those cash flows to a lower discount rate. Investors are used to thinking only about the duration of bonds, but all sorts of assets have a definable duration with regard to the discount rate applied to their cash flows, and equities, as not only a perpetuity but a growing perpetuity, have a ton of duration to them. Table 1 shows the approximate duration with regard to the discount rate on their cash flows of a variety of assets, along with the expected gain in their price if the discount rate were to have fallen by 1.25%.

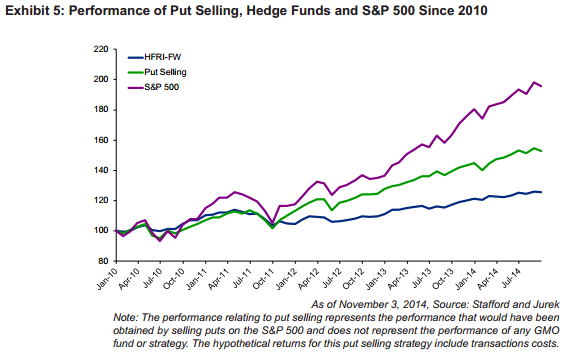

There is a certain amount of guesswork to these figures as, apart from bonds, none of them have fixed cash flows that can give a precise measure of duration, and partially for that reason I didn’t bother to try to calculate the associated convexity effect of the change in discount rate. But taking the figures at face value, let’s say that you can justify a 44% rise in equity valuations if the required return on equities has fallen from 5.7% real to 4.5% real. Investors have found themselves doubly disappointed by hedge funds since the onset of the Global Financial Crisis. First, investors were shocked by the extent to which hedge funds fell in sympathy with the stock market in 2008. And ever since, they have been disappointed by the fact that hedge fund strategies have failed to come close to the performance of equities – or in many cases even keep up with the performance of bonds – in the rally since 2009. One way to reconcile this disappointing performance is to recognize that many hedge fund strategies are underwriting the same basic risk as the equity market, but doing so in a fashion that has much less duration. Stafford and Jurek showed a few years ago that most hedge fund strategies can be reasonably modeled as variants on equity put selling. Exhibit 4 shows the performance of a put-selling strategy versus the HFRI fund weighted index of hedge funds.

This isn’t exactly the strategy Stafford and Jurek used in their paper, which was levered and sold out-of-themoney puts. It is a simpler unlevered strategy selling at-the-money puts every month. The reason I’m using this version is that it is nice and straightforward to understand that an at-the-money unlevered put-selling strategy is underwriting the same risk as an unlevered equity position – you lose money one-for-one when the equity market falls – but the way you get paid is different, because rather than collecting the gains on equities, you get paid a premium for the option you have sold. This method of payment means that put selling has a much shorter duration than equities do, and would not be expected to keep up in an environment in which a falling discount rate has driven up the price of equities. The performance of the S&P 500, put selling, and the HFRI since 2010 is shown in Exhibit 5.5

The performance of put selling has been one half that of the S&P 500 since 2010, and for hedge funds, one quarter. It is far too facile to say that put selling has half the duration of the stock market and hedge funds one quarter the duration. In fact, I haven’t been able to figure out a sensible way to calculate a duration of either of them given the nature of their cash flows, but it is almost certainly the case that for both of them the duration answer is “a lot less duration than stocks.”6

But if we are in an environment today where we aren’t sure whether stocks are very overvalued or whether they have been repriced to give a lower, but still fair, return, taking equity risk in a fashion that has less duration looks like a pretty good idea. If we are in Purgatory, we’ll do a lot less badly than in stocks (depending on how long mean reversion takes, we might actually make decent money) and if we are in Hell, the tailwind for equities that has made such strategies look uninteresting is probably over and there is no particular reason why they don’t have a decent shot of keeping up with standard equities.

And if you look at what we are doing in our benchmark-free strategies, that’s exactly the direction we’ve been moving toward in recent months, adding to merger arbitrage where we structurally can and doing more put selling than we had been, while reducing our weighting in standard stocks. This has not been driven directly by the Purgatory/Hell debate but rather by the fact that the attractiveness of these shorter-duration strategies has been naturally rising to us relative to our slowly falling forecasts for equities.

Conclusion

It would be incredibly convenient right now to know if we are going down the Purgatory route or the Hell route. Our official forecasts are for the Purgatory path and our hopes are there as well because Hell is a very unpleasant long-run outcome for investors. But if we knew we were in Hell, the right solution today is a decently risked-up portfolio. That portfolio doesn’t make sense in a Purgatory scenario, as the extra risk gives almost no additional return. There is no solution that is right for both scenarios, but having assets whose expected returns are reasonably unaffected by which path we go down is a help. The strategies that most fit the bill are the very “hedge fund-y” strategies that have so disappointed investors in recent years. That benefit is well short of an argument for happily paying 2% and 20% for such strategies, but if you can find a way to do it more cheaply (or you can actually find some managers talented enough to pay for their fees), we believe now is a pretty good time to be on the look-out for shorter-duration ways to take standard risks.

1 My son’s obsession with Legoland is a bit of a mystery to the rest of us as he isn’t particularly enamored of Legos, has never been to a theme park of any kind, and has no idea whatsoever what he would do should he ever actually cajole us into taking him to Legoland. But the heart wants what the heart wants, and his heart seems to be currently shaped out of little rectangular plastic blocks.

2 The chart is showing approximate ex-ante real T-Bill yields – that is what buyers of T-Bills probably thought they were going to get after inflation. Ex-post real T-Bill yields are much easier to calculate, but they aren’t that relevant for his purpose because they may or may not bear much resemblance to what the buyers of the bills expected to achieve.

3 Strictly speaking, this is only true for infinite life entities like endowments and foundations. The shorter the time period that the money is to be spent over, the larger the incremental spending that is supportable. If the money was going to be spent tomorrow, for example, the fact that future returns are lower is irrelevant and the 38% larger portfolio actually does support 38% more spending.

4 Okay, I have to admit to a big caveat here. This set of Hell forecasts assumes that the return on capital on the current stock of economic capital for corporations is not affected by the fall in the discount rate. In these forecasts the lower discount rate only impacts the return on capital on future investments. As James Montier has pointed out to me, this assumes a significant disequilibrium will persist for quite a while, although the disequilibrium will eventually dissipate as today’s capital is depreciated away. If you assume that the return on current economic capital is fairly quickly eroded by the lower discount rate, the Hell forecasts for equities wind up actually a little worse than the Purgatory ones. I chose not to make that assumption because I couldn’t think of a plausible mechanism that would cause the quick erosion, but that could just be due to my lack of imagination. Bond forecasts are not affected by any of this because their cash flows are fixed.

5 I picked 2010 as a starting point because it was a time when asset pricing had generally recovered from crisis levels, but participants still seemed to be assuming cash rates would normalize. I’m not sure how to pick a “perfect” starting point for this analysis, but 2010 seemed as good as any.

6 I don’t mean to imply that I think hedge funds have less duration than put selling, or that their underperformance relative to that simple strategy is readily explainable or excusable. Hedge funds look to have done worse than one would have expected over the past five years. They should not have been expected to keep up with the stock market in this kind of environment, but it would have been nice if they had kept up with a simple put-selling strategy.

Disclaimer: The views expressed are the views of Ben Inker through the period ending November 2014, and are subject to change at any time based on market and other

conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for

illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2014 by GMO LLC. All rights reserved.

© GMO