Risk Parity: Comparing the Objections With Reality Part 1

Over the last several years, risk parity has gained prominence as a general asset allocation approach as well as a specific strategy. Rising adoption rates of the approach have invited scrutiny from both practitioners and academics. We agree with some of the challenges identified by critics and have addressed them over time through our research agenda. Others, however, either do not apply to our version of risk parity or, at least to our knowledge, the approach in general.

In this blog series, we will look at two objections we’ve heard about risk parity, and explain why we believe they do not apply to our risk-parity approach — the Invesco Balanced-Risk Allocation strategy.

What is risk parity?

Before we begin addressing objections, we’d like to offer a quick definition of risk parity. In general, risk parity is an asset allocation strategy that seeks to build portfolios in which each asset class — such as stocks, bonds and commodities — contributes an equal amount of risk to the overall portfolio. This is in contrast to traditional strategies, which weight assets according to their dollar amount in the portfolio (60% stocks and 40% bonds, for example.)

Proxy portfolios don’t tell the whole story

Many of the critiques of risk parity include a proxy representation of the strategy — a sample asset allocation that’s used as a shorthand definition for risk parity as a whole —which they then proceed to criticize. However, these proxy portfolios almost always seem to miss important characteristics of risk parity.

A number of academic papers construct model risk parity portfolios using US equities, US Treasury bonds, credit (either investment grade bonds, high yield, or both), and Treasury Inflation-Protected Securities (TIPS). Given the historical performance of these assets, this type of portfolio would experience significant interest rate risk and lack sufficient defense against inflation. (TIPS would offer some defense against inflation, but they were not introduced until 1997 and therefore would not have been a factor in earlier inflationary periods.) Unsurprisingly to us, critiques of this type of proxy focus on the overuse of bonds and how that would have negatively impacted such a portfolio in the late 1970s and 1980s.

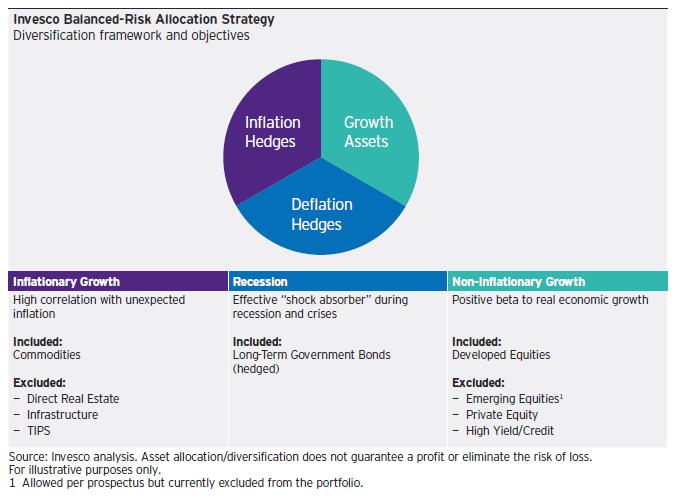

In contrast, when we build our balanced-risk portfolios, we think first about economic outcomes — including inflation — and which assets could best defend or take advantage of each (see exhibit). We next consider the liquidity, diversification benefit, and evidence of a risk premium1 for each asset. This results in a portfolio that has the opportunity to prove resilient in challenging environments, ample liquidity, and diversification.

Commodities: A critical component of our strategy

When we examine the proxy portfolio example described earlier in the context of economic outcomes, we can see there is little parity among the economic environments. Stocks fall into the non-inflationary growth category as does the spread portion2 of high yield or investment grade bonds. Treasuries and the related portion of credit products cover recession, and inflationary growth is only covered by TIPS since 1997.

In contrast, our balanced-risk approach includes commodities, which have historically outperformed in inflationary environments.3 Therefore, reviews of how the proxy portfolio might have performed in the late 1970s and 1980s are misleading when thinking about our strategy.

Important Information

1 A risk premium is the amount of return an asset generates above cash.

2 The spread portion of bond returns are those returns that are in excess of Treasury returns.

3 During the inflationary period of 1973 to 1981, stocks (represented by the S&P 500 Index) returned 5.16%, and commodities (represented by the S&P GSCI Index) returned 12.81%. Sources: Morningstar, Bloomberg L.P., Invesco.

The S&P 500 Index is an unmanaged index considered representative of the US stock market. The S&P GSCI Index is an unmanaged world production-weighted index composed of the principal physical commodities that are the subject of active, liquid futures markets.

Under normal conditions, the strategy invests in derivatives and other financially linked instruments whose performance is expected to correspond to U.S. and international fixed income, equity and commodity markets. However, the performance of the asset classes cannot be guaranteed.

Diversification does not guarantee a profit nor eliminate the risk of loss.

Commodities and futures are volatile a may not be suitable for all investors.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

Before investing, investors should carefully read the prospectus and consider the investment objectives, risks, charges and expenses.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2014 Invesco Ltd. All rights reserved.