Year-End Roller Coaster

- Q4 volatility likely to persist through year-end

- Portfolio positioning for the end of 0% short-term interest rates

- Mutual Funds versus Separately Managed Accounts in a rising interest rate environment

- Mid-term election implications for municipal governments and taxes

It’s hard to believe that only seven weeks remain before 2014 is finished. For the investment markets, the reality is that only four weeks of active trading remain due to the forthcoming holidays. Individual investors, traders, and institutional money managers should be positioning themselves for year-end. While the last half of the last quarter of the year has traditionally been a relatively active time in the financial markets, banking constraints imposed following the Great Recession, resulting in new regulations such as Dodd-Frank, have exposed investors to possibly greater late-year price volatility.

We anticipate increased profit-taking, tax-swapping and asset repositioning in response to the impressive gains achieved in both the equity and fixed income markets.

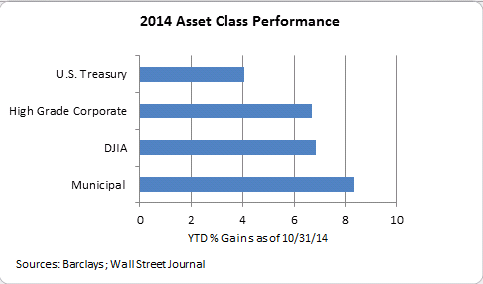

Among the most surprising and impressive asset class performance reported has been that of long-term municipal bonds. Most pundits were calling for negative market performance again this year following the sharp 2013 sell-off; no one we know of (ourselves included) foresaw the stellar returns achieved through the year’s first ten months. The tenth consecutive month of gains in 2014 is an unprecedented string dating back to 1989, according to Bloomberg analytics. Falling yields have enabled many issuers to refund their higher yielding outstanding debt at lower costs, as well as encouraged additional new tax-exempt debt issuance in order to take advantage of lower rates. State and local governments issued over $36 billion of long-term, fixed rate bonds last month, the highest monthly total since March 2013. As long as borrowing costs remain close to current levels, net new issuance should increase next year.

Both individual and institutional investors have proven to be steady customers throughout 2014, mostly undeterred by record low municipal yields. Competition has been intense, and many buyers have elected to become spectators by adding to their cash positions while awaiting better buying opportunities at higher yields. The best proxy for municipal tax-exempt security demand is the flow of money into mutual funds. Aggregate fund inflows total over $15 billion year-to-date, a very significant reversal from the net outflows experienced last year. However, there has been a significant deceleration in the pace of buying since the beginning of the fourth quarter. We anticipate the flow of new purchases will continue to dwindle into year-end, and anticipate the possibility of a trend reversal to more sellers, which should be anticipated after a sustained period of performance that is well-above historical norms. The better than 8% return garnered by the Barclays long-term bond index through October 31 is unlikely to be repeated.

Volatility has been largely absent this year; however, the gyration in yields since the beginning of October has been significant enough to give investors pause. The pace of selling has picked up recently compared to the first nine months of the year, and it is expected to accelerate into year-end.

Bond Market Volatility: Q4 2014

|

10-Year UST Yield Change |

10-Year Municipal Yield Change |

30-Year UST Yield Change |

30-Year Municipal Yield Change |

|

|

Sept. 30 |

2.48% |

2.17% |

3.20% |

3.09% |

|

Oct. 15 |

2.14% - 0.34 |

1.81% -0.36 |

2.90% -0.30 |

2.75% -0.34 |

|

Oct. 31 |

2.33% +0.19 |

2.07% +0.26 |

3.07% +0.17 |

3.00% +0.25 |

|

Nov. 10 |

2.35% +0.02 |

2.18% +0.09 |

3.09% +0.02 |

3.07% +0.07 |

|

Net Change |

-0.13 |

+0.01 |

-0.11 |

-0.02 |

Sources: Thomson Financial (MMD “AAA” Municipal, 5% coupon); Bloomberg

Mounting geopolitical tensions, escalating economic weakness in the Eurozone, and further stimulus measures from the Japanese and European Central Banks, contributed to renewed strength in the dollar and demand for U.S. Treasury debt in early October. The response in domestic fixed income markets was swift and furious, as shown in the table above. Treasury and municipal yields plunged to their low of the year during the first two trading weeks of the month; however, the yield reversal and accompanying sell-off was equally swift. Investors have finally gotten a taste of what had been largely missing through the first three-quarters of 2014 – volatility. We do not view this as an aberration, but more likely a foreboding.

Anticipating a more challenging trading environment in 2015, if not an outright reversal of the 2014 trend, SMC FIM has implemented a more conservative investment strategy by harvesting some of the gains earned this year and moving to a slightly more defensive posture. Countdown to “the end of 0% short-term interest rates” continues and it will likely happen later next year according to the consensus forecast. This factor alone should significantly add to skittishness and create more volatility. While municipal bonds might still register a second consecutive year of positive performance, the prospect for a repeat of this year is unlikely.

Besides instituting the more obvious portfolio management strategies such as duration and maturity reduction and raising cash reserves, there are other tactics a portfolio manager can utilize such as shifting assets into more defensive (higher coupon) bond structures or repositioning along the maturity spectrum. Another strategy is to hold “kicker” (cushion) bonds. A kicker bond is a callable, premium bond that is priced assuming it will be redeemed at an upcoming call date, in advance of its final maturity. These bonds are best utilized in a stable or rising rate environment. Should the call feature not be exercised by the issuer at the call date, the yield the investor will receive increases, or “kicks up,” based on holding the high coupon bond to the later maturity date. Buyers receive higher yields at purchase because they must be compensated for the uncertainty of the call. Generally, they offer more attractive market yields relative to non-callable bonds of similar maturity and are a great source of extra income and principal protection in an uncertain environment.

By maintaining direct ownership of municipal bonds through a separately managed account (SMA), investors gain the advantage of additional yield provided by kicker bonds. On the other hand, a mutual fund manager might be dissuaded from purchasing due to the specialized yield (30-day SEC) reporting requirement, which is the basis for quoting yield. Also, it should be kept in mind that if interest rates increase, the purchaser of an individual bond will immediately benefit from buying the higher yielding security currently available in the market. The mutual fund advertised yield will likely lag that of similar profile individual bonds if the majority of bonds held in the fund were bought during the lower rate environment. Conversely, when rates decline, the mutual fund will often offer the better yield until rates normalize.

The November mid-term elections provided some more “food for thought” for investors. Republicans have seized control of the Senate for at least two more years and widened their majority in the House by 14 additional seats. Additionally, three more GOP governors were elected, bringing their ranks to a total of 31. With a more conservative leaning at the national and state levels, we anticipate more calls for action regarding fiscal discipline. For state and local governments, the focus will be on deficit reduction, especially in regards to retiree pensions and health care. Look to financially strapped Illinois to see if the newly elected GOP governor will allow the temporary tax increase, imposed by the departing Democrat incumbent, to expire as scheduled in January.

In 2014, $44 billion of state and local spending measures were passed across the country compared to only $13 billion last year. Many of the proposals were for infrastructure and school projects. While the election results indicate most citizens probably agree that our country is in need of more infrastructure spending, it remains to be seen if the voter-approved projects will advance, especially given the more conservative tone of the 2014 elections.

Finally, no election analysis would be complete without a comment about tax reform and the possible impact on the tax-exemption bestowed on the interest received from municipal debt obligations. While we anticipate a great deal of clamoring for a cut in the corporate tax rate, which might be possible, the chance for a much needed change at the individual level is remote, particularly before the 2016 election.

Those of us willing to admit that we were managing municipal investment portfolios back in 1986 remember how the tax-exempt market essentially shut down for most of that year due to the uncertainty about the possible elimination of the federal tax exemption on municipal interest income. While the exemption was not repealed, the “Reagan Tax Act,” signed into law late in the year, did reduce the top federal tax bracket from 50% to 28%. Needless to say, the market is still thriving today despite a much lower top marginal rate of 39.6%.

We do not anticipate a repeat of 1986. For that matter, we doubt there will be any change to the status quo until at least after the 2016 Presidential election. The climate in Washington is still too acrimonious in our view to get a tax deal done, and issues such as healthcare and immigration reform will likely be the focus. The most recent tax reform proposal (Tax Reform Act of 2014) was drafted by outgoing House Ways and Means Chairman, David Camp (R-Michigan). One of the most important features of the proposal is the creation of only three tax brackets: 10%, 25% and 35%, and a 10% surtax on wealthy individuals. While we anticipate some challenging headline risk for municipals, it is unclear how the Republican-controlled Congress will respond. Experience suggests that there will be considerable debate but little action.

Disclosures

The information provided in this commentary is not intended to be a complete summary of all available data. Certain information contained herein has been obtained from published sources and/or prepared by sources outside SMC Fixed Income Management (“SMC FIM”), a division of Spring Mountain Capital, LP, and certain information contained herein may not be updated through the date hereof. While such sources are believed to be reliable, no representations are made as to the accuracy or completeness thereof by SMC FIM or any of its affiliates, directors, officers, employees, partners, members or shareholders, and none of the former assumes any responsibility for the accuracy or completeness of such information. Nothing contained herein shall be relied upon as a promise or representation as to past or future performance.

This commentary does not constitute an offer to sell or a solicitation of an offer to purchase securities, or any other product sponsored or advised by SMC FIM or its affiliates, nor does it constitute an offer or a solicitation to otherwise provide investment advisory services. It should not be assumed that any of the security transactions listed were or will prove to be profitable, or that the investment recommendations we make in the future will be profitable.

Statements contained in this commentary that are not historic facts are based on current expectations, estimates, projections, opinions and beliefs of SMC FIM. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Unless specified, any views reflected herein are those of SMC FIM and are subject to change without notice. SMC FIM is not under any obligation to update or keep current the information contained herein.

This commentary does not take into account any particular investor’s investment objectives or tolerance for risk. The information contained in this commentary is presented solely with respect to the date of its preparation, or as of such earlier date specified in it, and may be changed or updated at any time without notice to any of the recipients of it (whether or not some other recipients receive changes or updates to the information in it).

No assurances can be made that any aims, assumptions, expectations, and/or objectives described in this commentary will be realized. None of SMC FIM or any of its affiliates, directors, officers, employees, partners, members or shareholders shall be liable for any errors in the information, beliefs, and/or opinions included in this commentary or for the consequences of relying on such information, beliefs, or opinions.

Neither this commentary, nor any of the contents hereof, may be reproduced or used for any other purpose, or transmitted or disclosed in whole or in part to any third parties, in each case without the prior written consent of SMC FIM.

Copyright © 2014 Spring Mountain Capital, LP. All rights reserved.