Three Reasons Why Commodity-Related Debt May Hold Value Under Pressure

SUMMARY

- Commodity prices have come under pressure due to slower-than-expected growth outside the U.S., divergent monetary policies resulting in a stronger U.S. dollar and lower-than-anticipated inflation.

- The sell-off in commodities and commodity-related debt, as well as related currencies, may be a short-term dislocation that offers value opportunities to bond investors.

- A flexible, opportunistic multisector bond strategy is one solution to take advantage of these value opportunities.

Investors have historically turned to commodity-related assets as a hedge against rising inflation. But despite expectations that inflation will rise in the near future, weak economic growth in the eurozone, Japan and China, as well as a stronger U.S. dollar, has had a negative effect on commodity prices. The volatility in the commodity space may create buying opportunities in commodity-related debt. However, the challenge will be in finding good long-term value.

A multisector bond strategy may be one solution. In this Insight, we explain how our strategy can be applied to find value in commodity-related credits after recent volatility in the sector. We begin our discussion with a focus on how and why we utilize price as a signal for finding value opportunities.

What does price mean to you?

As opportunistic bond investors, we embrace uncertainty in order to find opportunities. A hallmark of our multisector bond approach is taking a longer-term view in order to take advantage of short-term dislocations. In our view, opportunistic means conducting thorough, rigorous research in order to recognize market inefficiencies. We then seek to capitalize on these opportunities.

For us, price can be a powerful indicator of value. Securities prices fall sharply when investors extrapolate bad news into a worst-case scenario. In some instances, the price of a security portends a situation that, in a probability sense, is less likely. In these times of short-term dislocations, we use price as a signal that value opportunities may exist. We assess the probability of an outcome and compare it to what the price of a security is suggests is the likely outcome.

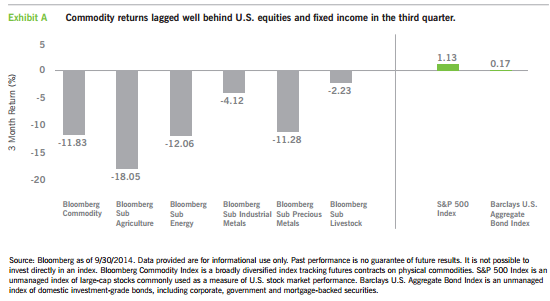

Let’s apply this simple concept to the commodity market. During the third quarter of 2014, commodity-related assets fell sharply, as Exhibit A shows. The consensus view of commodities, we think, has been set with a worst-case scenario in mind. While commodity prices dropped sharply during the quarter, there has been no change in the underlying fundamentals of some commodity-related companies. As bottom-up bond pickers, this is a scenario that piques our interest.

Why have commodities declined so sharply?

We see three reasons why commodity prices have dropped sharply, which also double as reasons why we’re attracted to the sector:

- Expectations for global growth have fallen.

- The U.S. dollar has rallied over the past year.

- Central banks around the world are pushing for higher inflation, but inflation simply hasn’t arrived.

We like to think of commodity prices as the world’s speedometer; when global growth is rapid, commodity prices have historically climbed as well, and vice versa. For example, industrial metals like nickel fell sharply in price after the International Monetary Fund (IMF) said it expects China’s economy to grow 7.1% in 2015, a slowdown from its own prediction of 7.4% in 2014. We also think that the concept of demand destruction comes into play, particularly with greater supply of several commodities made available. With lower world growth predicted for 2015, expected demand for commodities has been reduced. With greater supply of commodities and lower global demand, many commodities, like crude oil, have dropped sharply in price.

Commodity prices have also been influenced by inflation, or a lack thereof. Historically, commodities have served as an inflation hedge. There are plenty of reasons for concern over rising inflation; central bank activity around the globe has been aimed at spurring higher inflation. The U.S. Federal Reserve (Fed) has used large-scale asset purchases (known as quantitative easing, or QE) to keep interest rates low and to stimulate inflation. More recently, central banks in Europe and Japan have been utilizing ultra-accommodative policies to increase inflation.

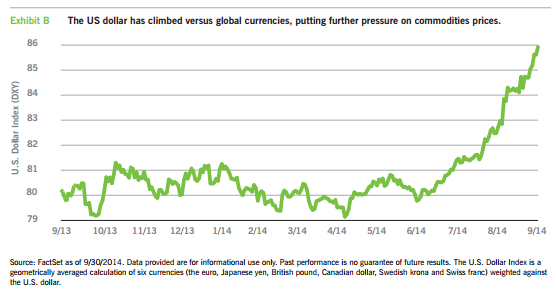

The problem: Higher inflation simply hasn’t arrived. U.S. inflation readings have instead come in below the Fed’s 2% target. Compounding the issue is the inverse relationship commodities have historically had with the value of the U.S. dollar. The divergence in policies between the Fed and other central banks may result in the U.S. dollar strengthening further. The dollar’s rally, highlighted in Exhibit B, has led to pressure on commodities prices.

It’s worth noting that the U.S. dollar has historically rallied in response to higher interest rates, so investors should have expected commodity-related assets to come under some pressure. This is all part of the market adjusting expectations for when the Fed raises short-term interest rates. However, the strength of the U.S. dollar had us wondering if the sell-off in commodities is due to expectations of a worst-case scenario.

We also want to emphasize that we are not “theme” investors from a top-down perspective, unlike other multisector strategies. We aren’t making a call on whether the dollar will go higher or lower, nor are we saying the dollar’s movement is correct or incorrect. We are simply questioning whether commodity prices at these low levels reflect a worst-case scenario compared to the probability of those events actually playing out as currently priced in.

Finding value in commodity-related debt and currencies

Commodity-related credit is a category that includes a broad array of issuers, both corporate and sovereign, whose balance sheets are effectively backed by real assets such as gold and timber. Much like the actual commodity, such debt may serve as an inflation hedge once the global economy regains steam.

It’s true that inflation is not rising as fast as the Fed would like, but the U.S. is far from experiencing a deflationary environment. With inflation slowly increasing, we think it may be time to consider companies that are backed by real assets. As detailed, these assets should hold up better in an environment of higher inflation, in our view, and that value should rise over time.

Because we are fundamental, bottom-up bond pickers, we analyze individual credits and make investment decisions based on that research. Not every commodity-related credit may be worthwhile; we look for issuers that have strong growth prospects. If an entity is growing, we think the balance sheet will be in a better position.

In addition, we are interested in currencies that have weakened substantially against the U.S. dollar, such as the New Zealand dollar. Investments in foreign currencies avoid direct U.S. interest-rate risk and have exhibited historical volatility closer to that of bonds rather than stocks. Some foreign currencies have historically exhibited low correlation to many traditional asset classes and also provided a hedge against the decreasing purchasing power of the U.S. dollar (i.e., inflation).

Use a professional bond manager

Finding value opportunities in short-term market dislocations, like the one we currently see in commodity-related debt, requires experience and proper expertise. One potential advantage of utilizing a professional manager is gaining access to the manager’s ability as a tactician.

Demand or supply in the commodities market could change swiftly, requiring investors to move deftly so as not to miss a reversal in commodity prices. For example, demand for commodities could rapidly increase if stimulus measures around the globe result in accelerating global growth. On the supply side, producers could cut production, which could lead to an increase in prices.

A flexible manager may be able to add value by being closer to the pulse of the markets, working with traders to recognize opportunities and to nimbly move to where opportunities may be.

About Asset Class Comparisons

Elements of this report include comparisons of different asset classes, each of which has distinct risk and return characteristics. Every investment carries risk, and principal values and performance will fluctuate with all asset classes shown, sometimes substantially. Asset classes shown are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. All asset classes shown are subject to risks, including possible loss of principal invested. The principal risks involved with investing in the asset classes shown are interest-rate risk, credit risk and liquidity risk, with each asset class shown offering a distinct combination of these risks. Generally, considered along a spectrum of risks and return potential, U.S. Treasury securities (which are guaranteed as to the payment of principal and interest by the U.S. government) offer lower credit risk, higher levels of liquidity, higher interest-rate risk and lower return potential, whereas asset classes such as high-yield corporate bonds and emerging-market bonds offer higher credit risk, lower levels of liquidity, lower interest-rate risk and higher return potential. Other asset classes shown carry different levels of each of these risk and return characteristics, and as a result generally fall varying degrees along the risk/return spectrum. Costs and expenses associated with investing in asset classes shown will vary, sometimes substantially, depending upon specific investment vehicles chosen. No investment in the asset classes shown is insured or guaranteed, unless explicitly stated for a specific investment vehicle. Interest income earned on asset classes shown is subject to ordinary federal, state and local income taxes, except U.S. Treasury securities (exempt from state and local income taxes) and municipal securities (exempt from federal income taxes, with certain securities exempt from federal, state and local income taxes). In addition, federal and/or state capital gains taxes may apply to investments that are sold at a profit. Eaton Vance does not provide tax or legal advice. Prospective investors should consult with a tax or legal advisor before making any investment decision.

The views expressed in this Insight are those of Kathleen Gaffney and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and Eaton Vance disclaims any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Eaton Vance are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund.

This Insight may contain statements that are not historical facts, referred to as forward-looking statements. Future results may differ significantly from those stated in forward-looking statements, depending on factors such as changes in securities or financial markets or general economic conditions.

About Risk

An imbalance in supply and demand in the income market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. Investments in foreign instruments or currencies can involve greater risk and volatility than U.S. investments because of adverse market, economic, political, regulatory, geopolitical or other conditions. In emerging countries, these risks may be more significant. As interest rates rise, the value of certain income investments is likely to decline. Investments in income securities may be affected by changes in the creditworthiness of the issuer and are subject to the risk of nonpayment of principal and interest. The value of income securities also may decline because of real or perceived concerns about the issuer’s ability to make principal and interest payments. No Fund is a complete investment program and you may lose money investing in a Fund. The Fund may engage in other investment practices that may involve additional risks and you should review the Fund prospectus for a complete description.

Before investing, investors should consider carefully the investment objectives, risks, charges and expenses of a mutual fund. This and other important information is contained in the prospectus and summary prospectus, which can be obtained from a financial advisor. Prospective investors should read the prospectus carefully before investing.

About Eaton Vance

Eaton Vance Corp. is one of the oldest investment management firms in the United States, with a history dating to 1924. Eaton Vance and its affiliates offer individuals and institutions a broad array of investment strategies and wealth management solutions. The Company’s long record of exemplary service, timely innovation and attractive returns through a variety of market conditions has made Eaton Vance the investment manager of choice for many of today’s most discerning investors.

©2014 Eaton Vance Distributors, Inc. | Member FINRA/SIPC | Two International Place, Boston, MA 02110 | 800.836.2414