Eurozone 2015 Economic & Capital Market Outlook

Five years after the financial crisis, the Eurozone is facing major challenges in restoring economic growth. The Eurozone is faced with numerous structural problems, high unemployment, excess capacity, stagnant wages, slow banking reform, declining manufacturing, low level of capital investment and the uncertainty of Russian foreign policy. The result is that member countries are struggling to comply with the original terms of the European Union and running budget deficits in order to stimulate growth within their countries. Even the stronger economies including France and Germany are beginning to show signs of weakness.

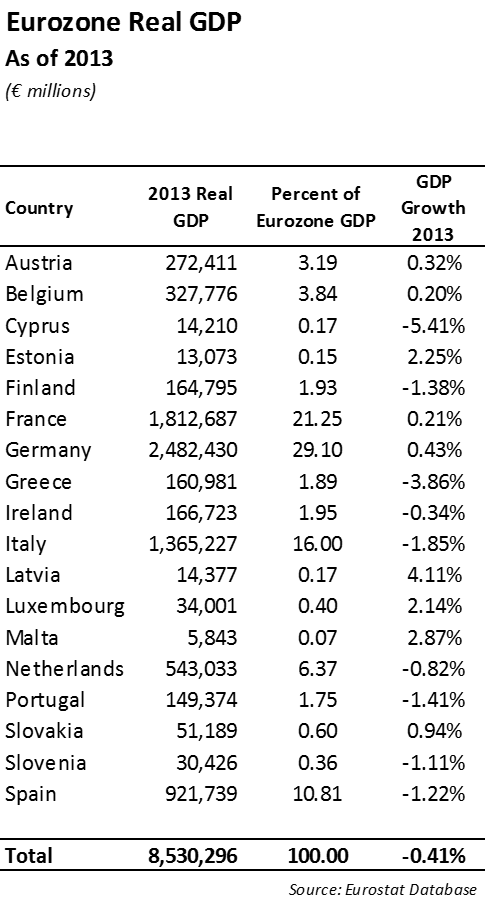

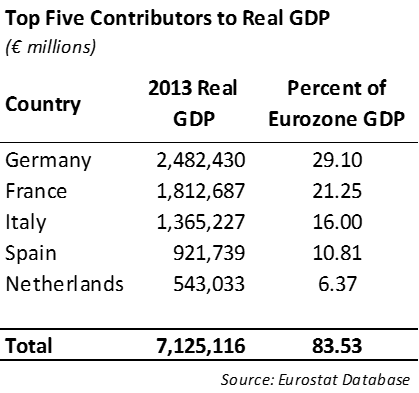

Germany and France represent 50% of the Eurozone GDP and the five largest economies represent 83.5% of the total GDP for the Eurozone. Thus, France and Germany have a large impact on the economic growth of Europe. Unfortunately, France posted zero percent growth over the second quarter of 2014. In the second quarter of this year, real domestic demand was 5% lower than in the first quarter of 2008. The Eurozone’s unemployment rate has risen by just under 5 percentage points since 2008 and deflation is a growing risk for the European Central Bank (ECB). We believe the Eurozone is in a severe recession. Without fiscal stimulus and structural economic reforms, we expect the Eurozone is four years away from a total meltdown which ultimately will put the euro currency at risk.

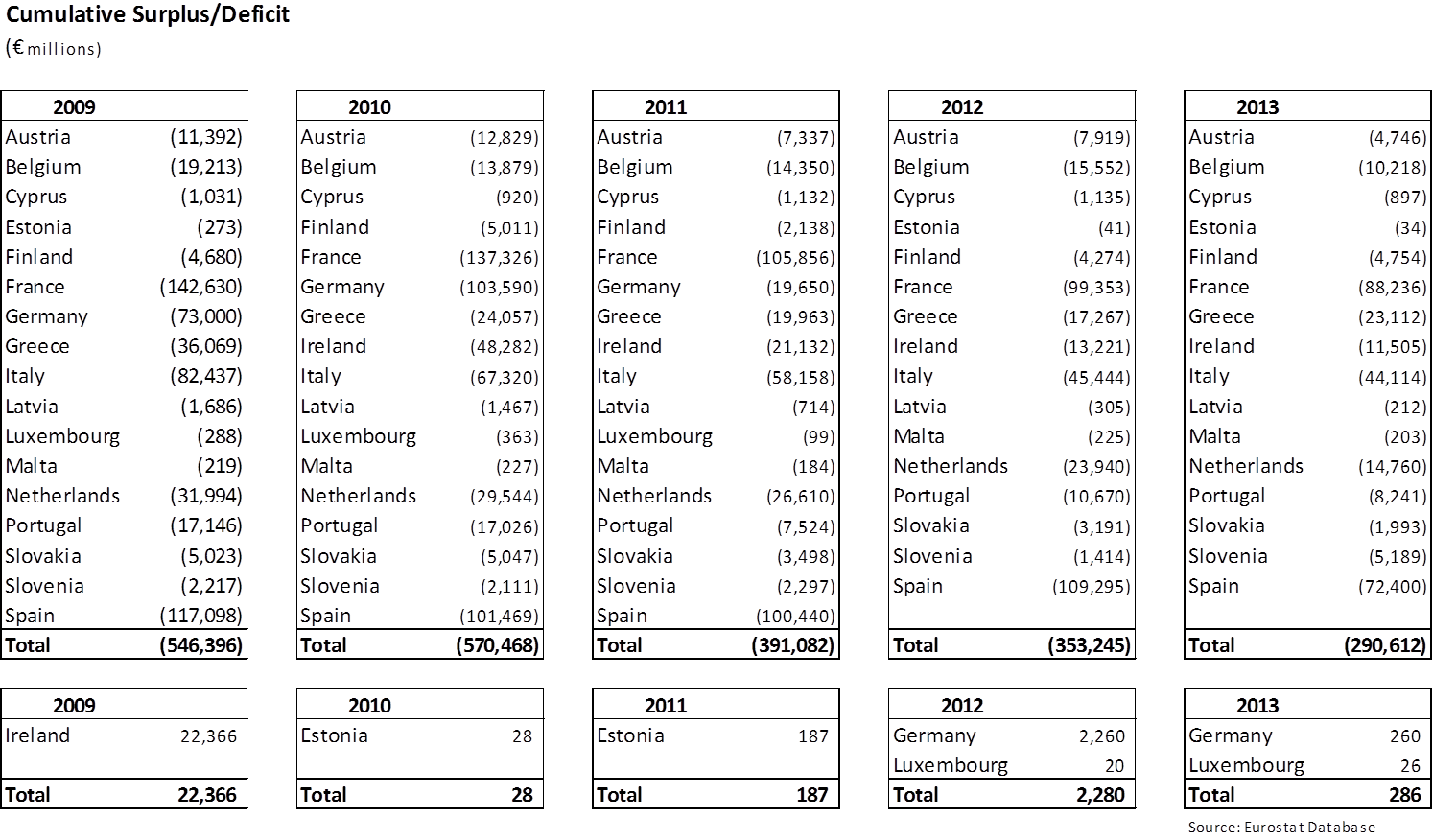

While the annual cumulative deficits of the Eurozone members have declined over the past five years, they are still substantial enough to be a barrier to meaningful economic reform. After reaching a cumulative annual deficit of €570.5 billion in 2010, the cumulative net deficit declined to €290.3 billion in 2013 according to Eurostat data. From 2009 to 2013, the cumulative deficit is over €2.15 trillion. This means that €2.15 trillion of expenses has been funded through additional debt.

Europe is challenged in that each country has its own culture, sovereign debt, taxing authority and economy. Yet, the euro is the common currency across the Eurozone. As a result, a country like Italy can’t alter its exchange rate to stimulate trade since the euro currency is common across the Eurozone.

Europe is living beyond its financial means. Cultures rooted in socialism and fascism emphasize government support for citizens. Strong labor unions which supported jobs and wages have had the effect of stifling business formation, entrepreneurship and risk taking.

Europe’s Growing Debt Problem

We consider the fiscal position of the Eurozone to be very weak. Of the eighteen countries using the euro, only two have managed to produce a budget surplus in the past three years. For each year that passes with a deficit, the respective country incurs debt to pay its bills. From 2009 to 2013, the countries in the Eurozone added €2.15 trillion in debt. An analysis of each country’s budget position over the past five years reveals that most countries generated a budget deficit, with the largest deficits being consistently generated by France, Spain and Italy. We do not expect that to change in the 2014-2015 budget years.

The cultural differences between the countries creates difficulties in implementing timely policies to effectively implement change within the European Union. Strong unions in France, Spain and Italy have made labor reforms difficult to implement. At the same time, the banks have been forced to strengthen their capital position to comply with Basel III standards and new Federal Reserve guidelines resulting in weak private credit expansion. As a result, job creation, fixed investment and business formation has been slow.

The leadership of the European Union has been fighting about whether to continue down the path of forcing austerity measures on those countries that rely on budget deficits to operate their economies. Over the long term, we do not believe the cultures of many of the European countries that rely on government sponsored social programs for citizens (including Italy, Spain and France) will change in a manner that allows for a more robust business and consumer sector. As each year passes and the deficits turn into debt, the financial burden on Europe grows. Ultimately, the growing debt burden will result in more credit deterioration and downgrades.

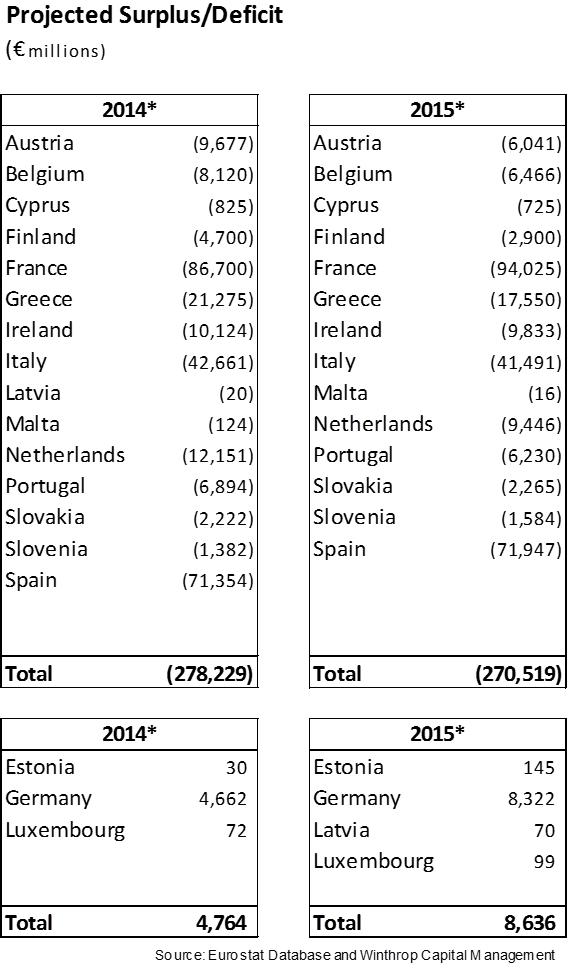

In the absence of any meaningful stimulus, we expect the Eurozone will incur over €650 million in additional debt over the next two years.

Access to Capital Markets

European countries are experiencing historically low interest rates similar to the United States. The ability for each country to access the credit markets and borrow at these low interest rates has helped to defer the growing debt problem into the future. Every year a country operates under a deficit, it must fund it by incurring more debt. As the debt grows, it will ultimately put pressure on the country’s credit rating. Theoretically, lower credit ratings result in higher borrowing costs; however, that has not necessarily been the case in Europe.

We believe countries are postponing the inevitable reconciliation between excessive spending and fiscal prudence into the future. Simply put, their economies cannot grow fast enough to rationalize the debt being incurred. As long as countries can access the capital markets and continue to borrow, the debt burden will continue to grow as the country incurs deficits. We do not believe that access to the capital market is a complete measure of success of the programs being implemented in Europe.

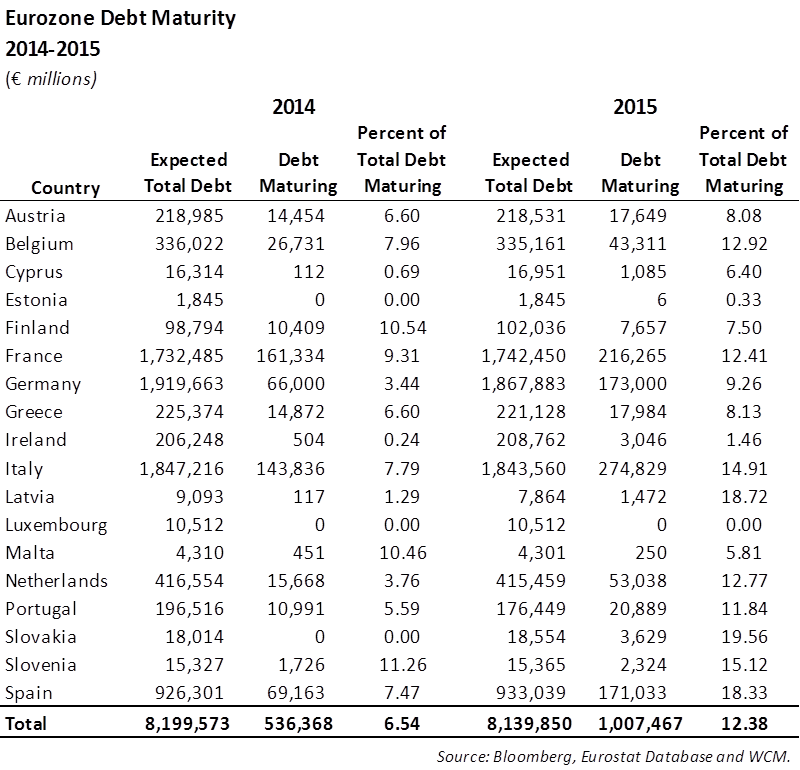

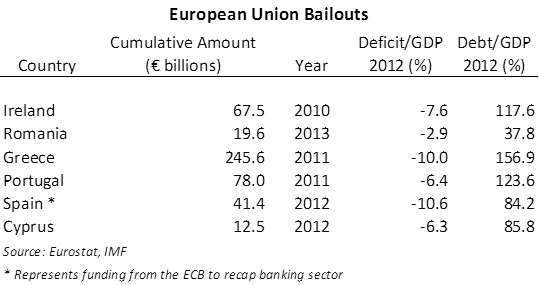

Italy is just one example the excessive borrowing by a member country. After accumulating deficits over the past decade, Italy now has the fourth largest bond market in the world today. Next year Italy will need to roll 14.9% of its total debt. At some point, the growing debt may culminate in a downgrade in the country’s sovereign rating which may, in turn, impair Italy’s ability to continue to borrow in the capital markets. Greece followed a similar path which culminated in 2009 with its down grade and inability to continue to pay its bills which lead to their bailout in 2011.

The European Central Bank

While inconsistent fiscal policies across the European Union, including forced austerity measures for many countries, have contributed to the economic malaise, monetary policy initiatives have proven ineffective in Europe. Unlike the Federal Reserve’s aggressive monetary policy over the past five years, the ECB’s monetary policies have not been able to provide the needed catalyst for growth. European Central Bank President Mario Draghi recently announced an asset purchase program by the ECB which is intended to mirror the Federal Reserve’s quantitative easing program. The program is designed to purchase asset-backed securities and covered bonds and add liquidity to the financial system while driving the yields on these assets lower. The question is will it work?

Because of the design of the ECB and the European Banking system, we believe that the ECB’s program will ultimately fall short of its intended stimulus impact. The problem in the Eurozone’s economy is not a lack of liquidity in its financial system; it is a lack of demand. While the details of the program have not been finalized, it appears that there is an intent to customize the asset purchases to the needs of the respective countries. In addition, the program may include purchasing riskier securities than the Federal Reserve allowed in its recent asset purchase program.

Europe’s banking system traditionally is more leveraged than the major banks in the United States and relies on wholesale funding for its deposit base. In addition, since the financial crisis Europe has struggled to put a common bank regulator in place and agree on policies. For example, the ECB recently raised concerns about the use of tax assets to boost capital levels, a practice that was meant to be phased out under the new EU rules. Following the bailouts of 2011 and 2012, the EU recognized the need for bank reforms and a common regulator over the EU banks. As a result of continuous bank negotiations in 2012, the ECB now has direct supervision of the top 300 largest banks in the Eurozone.

Summary

The Eurozone has struggled to achieve sustained economic growth following the financial crisis. In addition, by its very nature as a co-operative managed currency, the governance around the Eurozone is tedious and often indecisive. While progress has been made over the past two years to stabilize the economies and capital markets of the member countries following the string of bailouts, it was difficult for investors to live through. We are at a point where the European banking system is stronger and better capitalized but economic growth across the Eurozone is slowing.

The conflict around the use of austerity measures to better manage member countries’ budgets in line with original treaty intentions reveals the cultural differences between the various member countries. We expect that by the time these differences are addressed in a meaningful way, years will have passed and the cumulative debt of the Eurozone will have grown significantly. We do not believe that “growing their way out of the problem” by attempting to stimulate growth through fiscal initiatives will work over the long term. Further, we don’t believe there is a vision to achieve any meaningful reform necessary to achieve sustained economic growth throughout the Eurozone.

The next likely step will be a series of downgrades starting with Italy and France. Any escalating conflict with Russia will be expensive and distract further from the European Union’s fiscal problems. Immigration will continue to be a problem for the southern countries and put pressure on its social program costs. Ultimately, we expect dithering in Europe to continue.

Gregory J. Hahn, CFA

Chief Investment Officer

Marco Carvajal

Research Analyst