By John Del Vecchio, CFA, portfolio manager of Ranger Alternative Management and AdvisorShares Ranger Equity Bear ETF (HDGE)

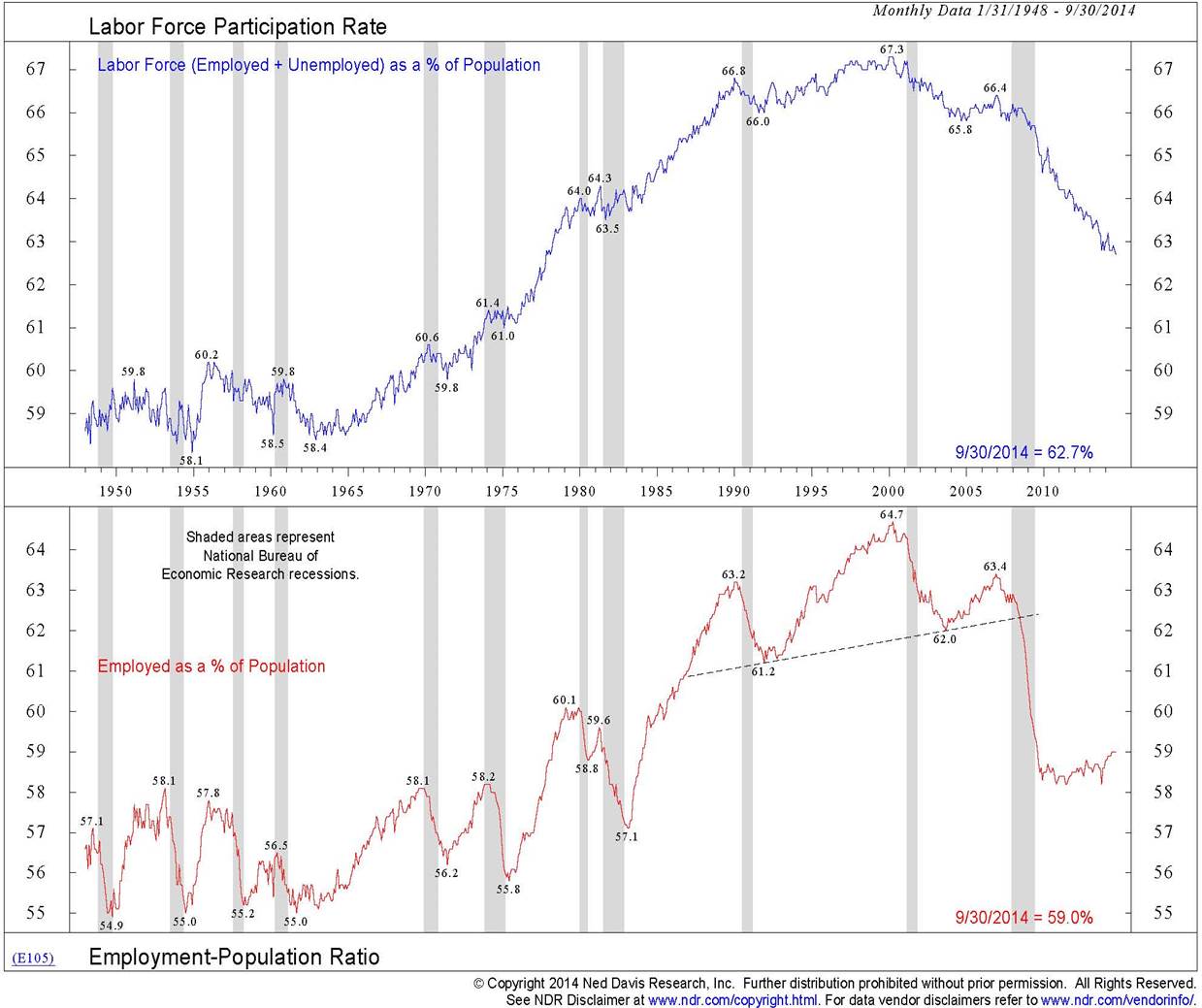

While many market observers debate whether quantitative easing (QE) “worked” the general consensus appears to be that the lower unemployment rate is a positive result of the Federal Reserve’s policies. Recently the unemployment rate hit 5.9%, the lowest since 2008. However, in our view, that is highly misleading with respect to the effectiveness of QE. The chart below shows the labor force participation rate as well as the percentage of people employed relative to the population.

As one can see, the results since the inception of QE are dubious at best. Currently, the labor force participation rate is 62.7%. This is a generational low and below the levels of the 1980’s recessions. Meanwhile, the percentage employed relative to the population broke its trend-line as QE was implemented and stands at just 59%. Other statistics paint and even more troublesome picture. For example, according to the Census Bureau, real median household incomes continue to plunge. In 2013 they hit $51,939 per household compared with nearly $57,000 in 1999 and $56,436 near the market peak in 2007 before the last crisis.

Why is this important? The economy is driven by consumption (approximately 70%) and fewer people are actually in the labor force regardless of what the misleading unemployment rate might state. Further compounding the problem is that wages are not growing.

The impact on stocks is simple. Companies have cut costs to the bone. In the work that we do, we see numerous companies buying back stock at inflated prices to prop up their earnings per share. Revenues are starting to wane at a time when the market is priced and multi-decade highs on a price / revenue basis. Profit margins are at all-time highs. Given that financial engineering can only be stretched so far – and it is near the max – demand is what could propel growth and ultimately equity returns higher. However, when that source of demand faces shrinking incomes and leaves the workforce all together, the demand side of the equation looks ominous. Investors need to approach with caution.