Lately, I’ve been fielding questions about the possible “unknowns” that could bring about the end of the current economic expansion. While I understand investors’ trepidation about the unknown, I believe this concern is misplaced. Business cycles do not generally end because of unforeseen accidents. They normally end because central banks, in an effort to bring down inflation, raise interest rates, which creates an inverted yield curve and slows money and credit growth. We are clearly a long way from this scenario at present. That is why I have argued over the past two to three years that this business cycle expansion will be one of the longest on record.

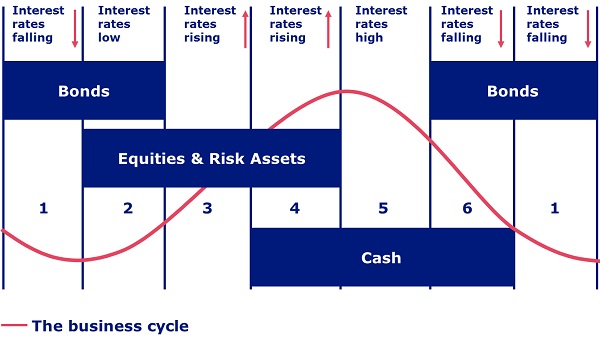

Below is a chart that I created that illustrates the typical business cycle from the bottom to the top and back down again. I also highlight the asset classes that have historically outperformed in each phase. I believe this is a good reminder of the true drivers of the global economy. For reference, I believe the US is transitioning from Stage 2 to Stage 3, and the UK is still in Stage 2.

Stage 1 (late recession). Typically in this stage, economic growth is still weakening, and as a result interest rates and inflation are typically low and falling. This leads the central bank to take stimulative monetary policy measures by cutting interest rates or conducting quantitative easing. In this environment of weak economic activity and low or falling interest rates, I believe bonds should generally benefit from both falling interest rates and declining inflation.

Stage 2 (early recovery). The central bank typically remains in stimulative mode with very low rates during Stage 2, and investors begin to anticipate better corporate earnings as economic growth starts to recover. Interest rates and inflation remain low, helping bonds to continue to perform. However, in this environment equities and other risk assets (such as commodities), anticipating the recovery in activity, should start to benefit and would be expected to outperform cash and bonds. Note that initially, most of the gains in equities should be attributable to rising price-to-earnings (P/E) ratios rather than higher earnings because the recovery is still expected rather than actual. Given the risks at this stage of recovery, I believe a mix of bonds and equities is favorable.

Stage 3 (full-scale expansion). The economic recovery becomes well-established in Stage 3, and the central bank starts to normalize its policy, raising rates back to levels consistent with continued growth, but with no intention of constricting future economic growth. Inflation remains subdued as it typically falls during the first two years of a recovery. Bond yields and market interest rates should rise along with the central bank’s rate hikes as investors start to anticipate inflation ahead, undermining bond market performance. As this happens, equities should generally benefit from continued earnings expansion and the upturn in economic growth. In this phase, most of the gain in equities should derive from growth of earnings and less from increases in the P/E ratio.

Stage 4 (late expansion). Business activity starts to show signs of overheating and inflation starts to rise in Stage 4. In response, the central bank typically raises rates even further, this time with the deliberate aim of slowing business activity in order to prevent inflation becoming too serious. As market interest rates and bond yields continue to rise, economic growth starts to slow. This causes corporate earnings expectations to be cut back, and profit growth to slow. I believe the cautious approach is reducing exposure to equities but taking advantage of the high yields available on cash-like instruments.

Stage 5 (start of the downturn). The economy has passed its cyclical peak in Stage 5, but inflationary pressures are still strong and interest rates remain high. As the economy begins to slow, equities are likely to fall in anticipation of lower profits. With central bank interest rates and inflation still high, bonds should not yet be attractive. High interest rates and inflation plus a weakening economy mean cash should generally be more attractive than bonds or equities.

Stage 6 (recession). Real GDP declines, and in response, the central bank lowers interest rates in Stage 6. Money and bond market yields should either anticipate or follow. The decline in business activity implies further declines in corporate profits. Equities would generally not be attractive in this environment. The returns to cash and deposits should decline, but still outperform equities. Bonds, benefitting from lower interest rates and inflation, should start to show improved returns.

The business cycle then repeats itself.

Digging deeper into the model

Models such as this can be developed further to take into account sub-classes of assets within the equity and bond markets. For example, early in the cyclical recovery (Stages 2 and 3), those sectors of the equity market most sensitive to an upturn in economic activity – such as transportation, basic materials and energy – could benefit. Later, as the economy reaches a peak in activity (Stage 4) consumer staples and utilities, which have more “defensive” characteristics, would not be expected to be as adversely affected by an economic slowdown.

Similarly, during Stages 6, 1 and 2 — as the economic risks diminish and the business cycle recovery becomes more established — the attractiveness of different types of bonds varies. Initially, I believe it is typically best to hold lower-risk government bonds, and gradually shift to high-quality investment grade corporate bonds and finally to more risky high yield corporate bonds.

There are other issues with using such stylized models that need to be kept in mind.

- First, economic and policy cycles (tightening and easing) are of varying length, so the length of the different stages varies. In the US, for example, postwar economic cycles – defined as from one peak to the next peak in activity have varied from 8 to 108 months.1 The progression through the choice of assets described would, on that basis, range from very rapid to slow and leisurely. This means that a thorough understanding of the business cycle must underlie shifts between asset classes.

- Second, markets’ assessment of the stage of the policy and interest rate cycle, and hence the choice between equities other risk assets and bonds, and between different sectors of those markets, can change very quickly indeed. The events of the summer of 2011 reminded us that we live in a world in which “risk on” can become “risk off” in days, indeed hours.

- Third, in such an environment, trying to time the market can be a very perilous activity.

- Finally, the notion of what is a “safe” asset has been challenged by concerns over sovereign debt.

Despite these issues, I believe this general approach can be useful as a guide to thinking about the choice of different assets through the economic and policy cycle.

1 Source: National Bureau of Economic Research

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2014 Invesco Ltd. All rights reserved.