Dear Reader:

CARDS AGAINST HUMANITY

There’s no way I can adequately describe this game. The game’s website (http://cardsagainsthumanity.com/) says, “Cards Against Humanity is a party game for horrible people. Unlike most of the party games you've played before, Cards Against Humanity is as despicable and awkward as you and your friends.” It’s all true and one of the most fun games I’ve played in a long time . It was introduced to me by my friends Karla and Bob. Deena and I have become addicted, as has everyone we’ve introduced it to. If you’re not familiar with Cards Against Humanity, take a look.

I DON’T UNDERSTAND

I recently read an article headlined, “Morgan Stanley paying $275 million to settle SEC charges.” Seems the firm settled with the SEC for failure to disclose adequately the delinquency status of home mortgages backing the security deals that it financed and sold. According to the article, the mortgages underlying the securities had a total value of about $2.5 billion. As is all too common in these cases, Morgan Stanley neither admitted to nor denied the charges and, no surprise, the firm spokesman said, “We’re pleased to have resolved this matter.” Even better, the bank said the payment would be charged against its 2013 results and wouldn’t affect its earnings in 2014.

I really don’t want to single out Morgan Stanley; it just happens to be the most recent article I read. As the story noted, the SEC settlement was latest in a series of federal actions against the Wall Street banks.

I may be naïve, but I don’t think so. There is something seriously wrong when major financial institutions can make billions misleading customers and then get away with “neither admitting nor deny allegations,” simply paying millions in penalties and proceeding about their business. If a small firm like ours engaged in such practices, we wouldn’t be in jail, we would be under the jail. I don’t understand.

MORE INTERESTING TIDBITS

From the same BA article

- In New York City, women are legally allowed to be topless in public.

- However, it is illegal to have sex on a motorcycle in London.

- And, in Mumbai, Personal Displays of Affection (PDA) are a punishable offence.

- New Yorkers speak more than 800 languages (and I struggle with one).

SOMETHING FOR NOTHING

This is for real! Sign up at https://www.bookbub.com/home/ and you’ll receive a daily list of ebooks available for free (or in some cases $0.99). We’re not talking about books no one wants or has never heard of, but ones you might really like to have. In my first week, I downloaded a half-dozen. CAVEAT: it’s like eating popcorn. Once you “buy” the free book, you’re likely to want to have a bunch of the author’s other publications – and they’re not free. As a result I think I bought 15 more. Obviously, whoever thought up this marketing ploy is a fan of behavioral finance. Still, the first one is FREE!

WHO WINS?

An interesting story in British Air’s Highlife magazine compared a variety of venues in London and New York; here are some of the results:

Winner

Museums London – 173 vs 131 for New York

Art Galleries London – 857 vs. 721 for New York

Public Libraries London – 383 vs. 229 for New York

Bookstores London – 802 vs. 777 for New York

Population London – 8,336,697 vs. 8,173,194 for New York

Green space (sq km) London – 1,572 vs. 1,214 for New York

Major live music venues London – 349 vs. 277 for New York

Restaurants London – 37,450 vs. 24,149 for New York

Restaurants (Michelin starred) London – 64 vs. 62 for New York

Cinema screens London – 349 vs. 277 for New York

Film Festivals London – 566 vs. 501 for New York

Bars New York – 7,224 vs. 2,143 for London

Did I mention I read this in a British Air publication?

GURUs

If you’ve been reading my NewsLetter, you’ll know one of my favorite subjects is “gurus.” Here’s another example of the folly of following the advice of self-appointed gurus from my friend Bob Veres’ most excellent Newsletter.

From Guru Marc Faber’s website:

“[He] is considered one of the world's premier economists and stock market investors. Known for his ‘contrarian’ investment approach, Dr. Faber is renowned for his timely market predictions.”

From Bob’s Newsletter:

“If you want an extreme example, consider Marc Faber, a Swiss investment guru who predicted the crash of 1987, and who recently predicted an imminent market crash in 2014. Ritholtz spent some time researching Faber’s track record in between these calls, and found that Faber announced that ‘stocks have likely peaked’ in September 2009. In 2010, he predicted imminent hyperinflation, saying that it was not a matter of if, but when. In 2011, he announced that the bear market had begun. Later in the same year, he predicted that the dollar’s value would fall to zero. In 2012, he predicted a 1987-style crash sometime during the year, and he repeated the prediction in 2013, and now again in 2014.”

POPULATION CONTROL?

According to the U.S. Department of Agriculture via USA Today, the cost of raising a child born in 2013 is $245,340 (http://usat.ly/VzQ16a). Housing is the single-biggest expense, averaging about $73,600 or 30% of the total cost of raising a child, followed by child care/education at 18%. Sure am glad mine are grown.

AND ONE MORE

This is a compilation of scenes from National Geographic videos. It doesn’t get much better. https://www.youtube.com/embed/Hodomt6bBOw

COOL GADGET

A 64GB USB 3.0 ScanDisk Flash Drive from Amazon for $20.55! I have no idea what I’m going to do with them, but I bought two.

NATURALLY

NOT LIKE I REMEMBER LIFE WHEN I GREW UP

There’s lots of discussion about Baby Boomers, Generation X and Millennials, but a recent article in AARP’s Magazine made me think that rather than age differences, I might be missing the really big demographic issues. Here are some statistics that led me to that conclusion:

| 1970 | 2013 | |

| Households consisting of a married couple and their children | 40% | 19% |

| 1960 | 2012 | |

| Adults who are married | 72% | 51% |

| Births to ummarried women | 5% | 41% |

SPEAKING OF AARP: GUESS WHO SHOWED UP IN A RECENT ISSUE.

http://www.aarp.org/money/investing/info-2014/what-financial-advisers-credentials-mean.1.html

THIS IS WHO I REMEMBER

In 1970, John Wayne hosted a variety show celebrating America's history. Included in the cast were: Ann Margret, Lucille Ball, Jack Benny, Dan Blocker, Roscoe Lee Browne, George Burns, Owen Bush, James Caldwell, Glen Campbell, Johnny Cash, Roy Clark, Bing Crosby, Phyllis Diller, Edward Faulkner, Lorne Greene, Harry Hickox, Celeste Holm, Bob Hope, Kay E. Kuter, Michael Landon, Forrest Lewis, Dean Martin, Dick Martin, Ross Martin, Greg Morris, Ricky & David Nelson, Hugh O'Brian, Dan Rowan, William Shatner, Orville Sherman, Red Skelton, Tom Smothers, Leslie Uggams, Jesse Vint, John Wayne, Patrick Wayne, Dennis Weaver, Dan White, Hal Williams, and The Doodletown Pipers. Watch it at: https://www.facebook.com/photo.php?v=10203900770857211.

AND THIS IS WHAT I REMEMBER

The Bates List Finder

It was my Outlook.

CHECK OUT YOUR STATE

WORTH WATCHING

By now you may have seen one or both of these; however, if not, they’re worth your time.

10 Life Lessons From A Navy Seal

Naval Admiral William McRaven’s University of Texas Commencement Address

http://www.youtube.com/watch?v=pxBQLFLei70

Jim Carrey’s (a Jim Carey you won’t recognize) commencement address at Maharishi University

http://www.youtube.com/watch?v=V80-gPkpH6M

KICKSTARTER BEFORE KICKSTARTER

From the KickStarter Blog – “In 1713, Alexander Pope set out to translate 15,693 lines of ancient Greek poetry into English. It took five long years to get the six volumes right, but the result was worth the wait: a translation of Homer’s Iliad that endures to this day. How did Pope go about getting this project off the ground? Turns out he kind of Kickstarted it. A year later, Pope crafted his pitch: ‘This Work shall be printed in six Volumes in Quarto, on the finest Paper, and on a letter new Cast on purpose; with Ornaments and initial Letters engraved on Copper,’ he wrote.

In exchange for a shout-out in the acknowledgements, an early edition of the book, and the delight of helping to bring a new creative work into the world, 750 subscribers pledged two gold guineas to support Pope’s effort before he put pen to paper. They were listed in an early edition of the book…

In 1783, Mozart took a similar path. He wanted to perform three recently composed piano concertos in a Viennese concert hall, and he published an invitation to prospective backers offering manuscripts to those who pledged:

‘These three concertos, which can be performed with full orchestra including wind instruments, or only a quattro, that is with 2 violins, 1 viola and violoncello, will be available at the beginning of April to those who have subscribed for them (beautifully copied, and supervised by the composer himself).’

Alas, not all projects reach their funding goals, and Mozart fell short. A year later he tried again, and 176 backers pledged enough to bring his concertos to life. He thanked them in the concertos' manuscript.”

AND WHO OWNS WHAT?

I know this is a bit hard to read. If you go to http://sploid.gizmodo.com/fascinating-graphic-shows-who-owns-all-the-major-brands-1599537576/+caseychan, you can see the chart enlarged.

AND ONE MORE

This is a compilation of scenes from National Geographic videos. It doesn’t get much better. https://www.youtube.com/embed/Hodomt6bBOw

DAVID vs GOLIATH

And who’s surprised? In the battle to hold anyone providing financial advice to consumers to a fiduciary standard, I fear $$$ will win. According to TD Ameritrade Institutional’s analysis of lobbying spending so far in the 2014 campaigns, [industry lobbyist] SIFMA has spent $3.96 million, followed by the National Association of Insurance and Financial Advisors, which has spent $1.4 million. On the fiduciary side, barely registering on that scale are the Investment Advisor Association, which has spent $80,000, and the Financial Planning Association, at $40,000. Caveat Emptor!

FOR EXAMPLE

The Republican-controlled House passed a budget that bars the Securities and Exchange Commission from imposing a fiduciary standard on broker-dealers during the federal fiscal year beginning October 1. The language, which also bans spending to write and adopt broker-dealer fiduciary rules, was approved in an amendment by voice vote. I’m still scratching my head about this. FOR SHAME!!

DOUBLE TAKE

Speaking of National Geographic naturally makes me think of photography and that makes me think of my client Maggie Silverstein. Maggie, a well-known South Florida portrait photographer just published her book Double Take: Portraits Over Time. With 50 photo sets the images chronicle the essence of childhood through the years and mark the delicate transition into adulthood. Dave Barry, Pulitzer Prize winning author who wrote the Afterword described Double Take best in his inimitable style. “If you’re a parent, you know where I’m going with this. Five minutes have passed, maybe six, and now Rob is a married man in his thirties.”

You can preorder Double Take from Books and Books

http://www.booksandbooks.com/search/apachesolr_search/maggie%20silverstein

DID YOU KNOW

- At least according to Reddit via BuzzFeedNEWS:

- The computer used to guide the Apollo 11 moon mission was less powerful than a modern calculator.

- We built an atomic bomb twenty years before we had color television.

- Lead rhymes with read. Lead also rhymes with read.

- The blue whale’s heart is the size of a Volkswagen Beetle.

- We figured out how to put a man on the moon before we figured out putting wheels on luggage.

CAVEAT INVESTOR

A tongue in cheek video about a client interviewing a potential advisor at a large brokerage firm. Created by my friend Bob Veres.

https://www.youtube.com/watch?v=0UZkv8HWsnc

NICE STORY

I think you’ll enjoy this, especially if you’re a frequent flyer like me. “Getting stranded on the runway when your flight gets hit with last-minute delays is enough to fray the temper of even the most

sanguine flier. But passengers on one severely delayed flight this week found themselves having an altogether more uplifting experience, when the pilot ordered pizza for the entire plane.”

GOOD STUFF

If you do any international traveling, one of the issues you’ll face is “tipping.” Like, who knows? Well, here’s a great link that spells out the politically correct amount in most countries around the world.

http://matadornetwork.com/abroad/ultimate-global-tipping-cheat-sheet-infographic/

SOAP BOX

In keeping with Caveat Investor and to continue my regular soap box rants on “suitability vs. fiduciary,” I thought I’d share an excerpt from Scott Simon’s most excellent Morningstar Advisor column. It’s kind of long, but well worth reading (and heeding). Scott is a member of our ad hoc Committee for the Fiduciary Standard and the trip he references is the one I wrote about in my last NewsLetter.

You can find Scott’s complete article at http://www.morningstar.com/advisor/t/93869173/the-conundrum-of-mary-jo-white.htm.

Last week, I set out from California on a journey to the center of the (political) earth in Washington, D.C., to join up with a small band--we happy few--of colleagues to meet with Mary Jo White, Chair of the SEC….

Fitting a Square Peg into a Round Hole

The fundamental, underlying problem faced by Chair White, of course, is reconciling the fiduciary standard of conduct that requires RIAs to put the "best interests" of their investor clients first with the fiduciary duty owed by stockbrokers as agents to the interests of their B/D principals. I've written about this conundrum before, but it wouldn't hurt to review the issues at hand here once again. In a nutshell, stockbrokers have a fiduciary duty to do what's in the best interests of their employer, but they don't have a fiduciary duty to do what's in the best interests of their investor clients. That's an inherent conflict of interest that no serious-minded person well-versed in these issues can "harmonize" in any way.

It's impossible to serve two masters at the same time, which is why it's impossible for a stockbroker to give investor clients objective advice based on a fiduciary standard. Because stockbrokers don't have to follow a fiduciary duty, the only way they can provide investment advice is if it's mere happenstance and not to be relied on in making serious decisions.

The problem begins when a B/D entity advising its investor clients from a strategic perspective is also the manufacturer of the products being offered as the solution. In order to be a good employee of the B/D, a stockbroker must do the best job that it can to sell products manufactured by the B/D. When a stockbroker sells a product, the advice that it provides to an investor client must be incidental in nature as a matter of law. This, in effect, means that the investor cannot depend on the stockbroker's advice when it tells the investor that the product is suitable for it.

Legally, then, a client making investment decisions is to ignore the stockbroker's advice and not rely on it because often it's inherently biased against the best interests of the client. That's because the B/D is the manufacturer of the products. If a stockbroker seeking to sell a product isn't able to do so, it might miss out on its quarterly bonus check or a trip to Hawaii with the spouse and kids, or even lose his job.

The regulations are straightforward. A B/D is in the business of manufacturing products and selling them to anyone who wants to buy them. There's nothing wrong with that. In fact, it's the same as if a B/D were a car dealer employing salespeople attempting to sell, say, a Ford to anyone who steps on the lot. But there's a big difference: the car buyer already knows what the dealer wants to do--sell him a Ford--even before setting foot on the lot.

But few investors have any awareness of the motivations of Wall Street. Indeed, Wall Street has done an excellent job blurring the distinction between what stockbrokers really are—Ford salespersons with a single-minded motivation to sell the products manufactured by their Ford-dealer employer—and the fairy tale of what's portrayed: a friendly client-centric experience with the best interests of their clients at heart. The investing public simply doesn't understand the difference between the advertising they see and the contracts they sign. Reading the provisions found in some of these contracts is akin to a seminar on how to pluck a goose without the goose knowing that it's been plucked.

Although Wall Street's business model, as noted, is the same as that of the Ford dealer--to sell products to anyone who comes along--there is one difference: Wall Street won't even match the transparent but honest motivations of a Ford dealer. Truth in advertising and Wall Street just don't seem to go well together in the same sentence.

If Wall Street were really interested in having a total commitment to the long-term interests of its clients, it would embrace a fiduciary standard. But it does just the opposite: It lobbies in Washington, spends big bucks on politicians, and does everything it can as an industry to avoid what a fiduciary standard requires. In 2007, former SEC chair Christopher Cox described the Wall Street business model as a "witch's brew of hidden fees, conflicts of interest" which is "at odds with investors' best interests." (Note in this regard that the Department of Labor's proposed rule is titled, "Conflict of Interest Rule-Investment Advice.") As I've said before, it's just as easy--actually, easier--to follow a fiduciary standard, to do what's in the best interests of investors within a truly client-centric business model.

FOR EXAMPLE

The Republican-controlled House passed a budget that bars the Securities and Exchange Commission from imposing a fiduciary standard on broker-dealers during the federal fiscal year beginning October 1. The language, which also bans spending to write and adopt broker-dealer fiduciary rules, was approved in an amendment by voice vote. I’m still scratching my head about this. FOR SHAME!!

WARNING

This is a repeat from a few years ago but with all of the news about hackers I thought it was worth repeating.

Warning from the NY Times via Readers Digest. When you decide on a new password, don’t use any of the five most common: 123456, 12345, 123456789, password, iloveyou. Guess I have a lot of passwords to replace.

FEELIN’ OLD!

“I was feeling pretty creaky after hearing the TV reporter say ‘To connect to me, go to my Facebook page, follow me on Twitter, or try me the old-fashioned way: email.’”

LOOKING FOR A JOB?

LUCK vs SKILL

In 1934, Professors Graham and Dodd, the fathers of fundamental investing, published their seminal book, Security Analysis that, according to Wikipedia, “…chided Wall Street for its myopic focus on a company's reported earnings per share, and were particularly harsh on the favored ‘earnings trends.’ They encouraged investors to take an entirely different approach by gauging the rough value of the operating business that lay behind the security.” Basically, Graham and Dodd reminded the reader that buying stock is an investment in a business and the price of the stock should be related to the value of the business.

Well, it seems some investors are still chasing stories, not fundamentals. The “hot” opportunity of the Alibaba IPO is a case in point. A WSJ article quoted a number of investors on their plans regarding the IPO. One, a salon owner said, “”I want to buy Alibaba on Friday, whatever the price [my emphasis]…This is an amazing opportunity. It will help pay for my kids’ college.” I hope for his kids’ sake he’s right but, if so, it will be due to blind luck, not thoughtful investing. What might go wrong?

As a valuation expert and Dartmouth business school professor noted, “I’m not even sure what my cash flow rights are. That’s troublesome. Taken by itself, this wouldn’t ruin it for me. But the second issue is a history of disclosure disputes between Chinese [companies listed in the U.S.] and the SEC. And finally, the company’s based out of a country whose corporate-governance culture is still evolving, to put it gently. These are things I have no idea how to model. It goes back to the distinction between uncertainty and risk. I know how to price risk. But what do I do with uncertainty?”

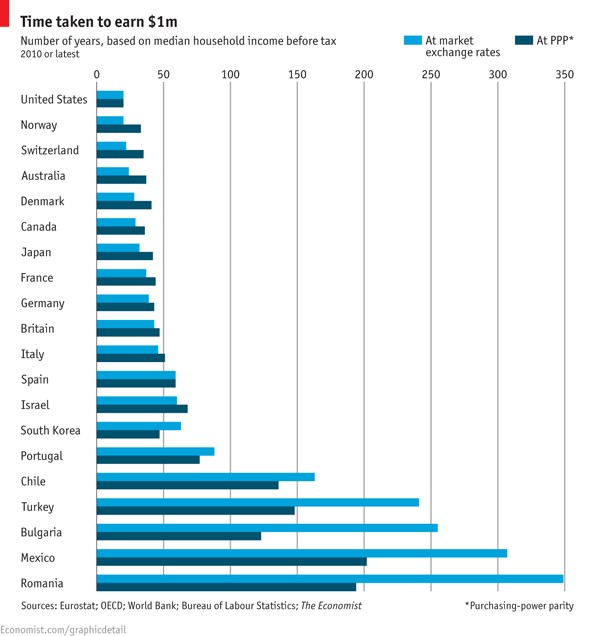

HOW LONG DOES IT TAKE TO EARN $1 MILLION?

It depends – turns out it makes a huge difference where you live (from Martina).

How long would it take for an average person to earn that special sum? To find out, The Economist looked at how much the main breadwinner in an average household makes each year (before tax). On this measure, America creates the swiftest millionaires. South of the border, Mexicans can expect to toil for three centuries to earn the same.

THE BEST OF THE BEST

I frequently write about the difference in the legal responsibilities of an investment advisor and a broker. Unfortunately, it’s difficult to convey accurately the significance of that difference, but I came across a Wall Street Journal article that provides a bit of an idea of the risk of conflicts of interest. Here’s the link to “J.P. Morgan Faces More Questions on Conflicts of Interest. SEC Looks at Whether Clients Were Steered to Banks' Own Funds; Inquiry Echoes Move by Bank Regulator.” http://online.wsj.com/articles/j-p-morgan-faces-more-questions-on-conflicts-of-interest-1407514915. Here are some excerpts from the article:

“Financial advisers can operate under different rules depending on whether they register as an investment adviser with the SEC. If they do, they must adhere to a so-called fiduciary standard requiring them to recommend only those investment products that are in the best interests of their clients. Others generally adhere to a different standard that allows them to recommend products that are merely suitable for the individual. Generally, investment specialists in J.P. Morgan's private bank who have discretion over client assets are bound by a fiduciary standard, whereas private bankers, who are relationship managers, are not.”

“The Securities and Exchange Commission is investigating whether J.P. Morgan Chase & Co. inappropriately steered private-banking clients to its own investment products and away from those offered by outside firms, according to people close to the probe.”

The article also notes that “J.P. Morgan in recent months has beefed up its disclosures to clients. In a May disclosure to clients, J.P. Morgan said it prefers its own funds, ‘unless we think third-party managers offer substantially differentiated portfolio construction benefits,’ according to a document reviewed by The Wall Street Journal. ‘Consequently, we expect the proportion of JPMC managed strategies will be high (in fact, up to 100 percent)’ in strategies such as cash and fixed income.”

That last observation reminded me of a comment I heard a few years ago at a meeting I attended in New York with the heads of the Wealth Management divisions of many of the major brokerage firms and trust companies. The discussion was around firms moving to “open architecture,” i.e., not restricting investment offerings to the firm’s proprietary product but offering the best available investments from different companies. After many participants bragged about how they were embracing the idea, one brave and honest soul said, “Wait, we all know what ‘open architecture’ really means. We scoured the world and discovered we offer the best of everything.” I guess Morgan agrees.

FROM AN OLD FRIEND

I met Dick Davis a LONG time ago when he was writing an investment column for the Miami Herald and publishing the Dick Davis Digest, an extraordinary newsletter that reflected Dick’s review of hundreds of financial newsletters and institutional research publications. Dick has retired and now writes his own unique blog. Below is the introduction to his first issue (he’s now on #3). I enjoy his eclectic musings, so I thought I’d introduce you Dick’s blog. You can find him at http://www.dickdavisblog.com/.

Dick Davis, here…….. CAN I COME IN?…………………………………..

Thanks. It’ll just be a short visit. I’m not selling anything; I have no agenda. Just wanted to say “hello” and leave you with something that may be helpful. You are receiving this because you are family, friend or acquaintance, perhaps from long ago. I’ll be 86. How does an old man blessed with the precious gift of life use that gift wisely? For me, one way is to share with you what I think is worth sharing, mostly excerpts from the articles, blogs, essays and quotations that I’ve accumulated in my “Wisdom” file over the years. My hope is that what I find wise, you will too. If some of these offerings can help you make wise choices in your pursuit of happiness, I’ll be a happy camper.

The subject is not finance; it is the business of living. As a broadcaster and writer, part of my job was sharing the wisdom of others. So this is just an extension of what I have always done–along with some personal observations.

And here’s a recent entry:

Airline Humor

One of the biggest irritants of modern day flying is having to wait forever on the ground, sealed inside the motionless plane, waiting for take-off. Pulitzer-prize humorist, Dave Barry, in an online column for the Miami Herald, puts it this way: “A century ago, it took a week to get from New York to California; today you can board a plane at La Guardia and six hours later–think about that: six hours later!–you will, as if by magic, still be sitting on the plane at La Guardia because “La Guardia” is Italian for “You will never actually take off.” Perhaps the funniest satire on airline travel is a classic skit from the “Carol Burnett Show” on “no-frills” airlines. Carol plays the stewardess, while comedian Harvey Korman plays the first class passenger and Tim Conway, the coach passenger. This skit appeared some 40 years ago (9/20/1975). Click here and decide if it has stood the test of time. WHERE DO THEY FIND THE TIME? I find it hard to believe, but according to the Journal of Financial Planning, high net worth individuals (they define that as individuals with earnings between $100,000 and a million) spend over 48 hours/week on social media.

BAD NEWS FOR ACTIVE MANAGERS

From S&P Dow Jones Indices

- Very few funds can consistently stay at the top. Out of the 687 funds that were in the top quartile as of March 2012, only 3.8% had managed to stay there at the end of March 2014. Further, 1.9% of the large-cap funds, 3.2% of the mid-cap funds and 4.11% of the small-cap funds remain in the top quartile.

- For the three years ending in March 2014, 14.1% of large-cap funds, 16.3% of mid-cap funds and 25% of small-cap funds maintained a top-half ranking over three consecutive 12-month periods. Random expectations would suggest a rate of 25%.

- An inverse relationship exists between the measurement time horizon and the ability of top-performing funds to maintain their status. It is worth noting that no large-cap or mid-cap funds

- managed to remain in the top quartile at the end of the five-year measurement period. These figures paint a poor picture of the lack of long-term persistence in mutual fund returns.

- Similarly, only 3.1% of large-cap funds, 3.6% of mid-cap funds and 5.5% of small-cap funds maintained top-half performance over five consecutive 12-month periods. Random expectations would suggest a repeat rate of 6.3%.

- The transition matrices track the performance of top and bottom quintile performers over subsequent time periods. The data shows the likelihood for the best-performing funds to become the worst-performing funds and vice versa. Of 426 funds that were in the bottom quartile, 28.64% moved to the top quartile over the five-year horizon, while 28.57% of those top-quartile funds moved into the bottom quartile during the same period.

The moral? Beware of chasing attractive returns from active managers. It’s likely to be yesterday’s story.

BAD (GOOD) NEWS FOR GOLFERS

According to Bloomberg Business Week, golf is suffering. From its peak in 2002, the number of golfers in the U.S. dropped 24% by 2013. In fact, the number of golfers today is lower than it was in 1990. Building new courses is not for the faint hearted at an average cost of $4.25 million. In 2013, only 14 new courses were built in the U.S. while almost 160 shut down. The good news, at least for those still playing, the cost of equipment has dropped significantly due to shriveling demand. For example, some drivers priced at $299 less than two years ago are now selling for $99.

GO FIGURE

Headline on Yahoo Finance for August 1st

S&P500 INDEX POSTS WORST FALL SINCE APRIL; INDEXES DOWN FOR JULY

How many investors do you figure bailed out of the market with this news?

Here’s the WSJ Headline for August 26th

S&P 500 PUSHES TO ANOTHER RECORD

Short-term market timing can be hazardous to your wealth!

GLOBILIZATION CONTINUED

According to Bloomberg Business Week, in Silicon Valley:

- One-third of the startups are founded by Indian Americans.

- In 2010, Asian Americans became the majority of the tech workforce in the Valley making up 50.1%.

- In 2011, 64% of the Valley’s foreign born talent had a B.A. or higher in science and engineering.

- In 2012, 51% of the Valley’s population spoke a language other than English exclusively at home.

- The largest annual influx of residents was from Mexico (followed in order by Texas, Arizona, Washington and Illinois).

ENGINEERING MADE SIMPLE

As I have two masters degrees in engineering, I can vouch for this process:

GREAT BIRTHDAY!

Deena and I attended Jean Sinclair and Bob Veres’ Insider’s and Leadership Forums on my birthday where 400 attendees (the best-of-the-best-of-the-best of the country’s financial planners) sang Happy Birthday and we received the following very cool awards.

Harold Evensky, chairman of Evensky & Katz/Foldes financial in Coral Gables, FL and Professor of Practice at Texas Tech University in Lubbock, TX, received the Insider's Forum Leadership Award. The award recognizes more than 40 years of outstanding service to the profession in a leadership role.

At the annual Leadership Forum dinner event, Deena Katz, Associate Professor in the Department of Financial Planning at Texas Tech University and co-chair of Evensky & Katz/Foldes financial in Coral Gables, FL, was presented with the Leadership Forum Iconoclast Award, recognizing in her career an ability and willingness to consistently think outside the box and move the profession forward in creative new directions.

FINALLY!

DO YOU TWEET? Then please follow us at https://twitter.com/EvenskyKatz

Hope everyone is having a great Fall, and hope you’ve enjoyed this issue of my NewsLetter. See you again in a few months.

Cordially Yours,

Harold Evensky, CFP®, AIF®

Chairman, Evensky & Katz / Foldes Financial Wealth Management

© Evensky & Katz / Foldes Financial Wealth Management