After an extended period of extremely muted volatility in virtually every major asset class, volatility is finally starting to pick up, as it was always likely to do. A number of our volatility measures such as our equity, FX, bond and commodity volatility have turned a corner recently and have moved up off of in some cases generational lows.

In this post, instead referring back to our asset class volatility indicators we'll touch on a few other measures of vol that have also picked up. The main theme is that volatility has picked up recently, but still remains fairly depressed by historical standards. Those measures are as follows:

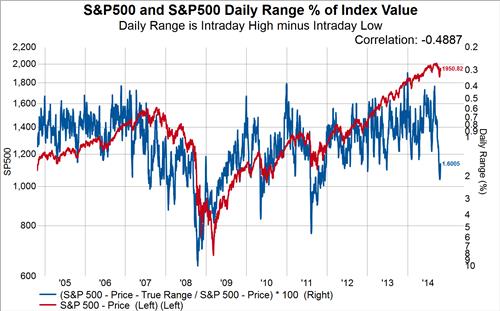

The S&P 500 daily range (the high value minus the low value) as a percent of the index level has spiked from low never before seen outside of an end of year period to a more normal level.

The 65-day cumulative number of stocks that gap lower at the open of trading has moved from an all-time low of about 800 back to a still low level of about 1750.

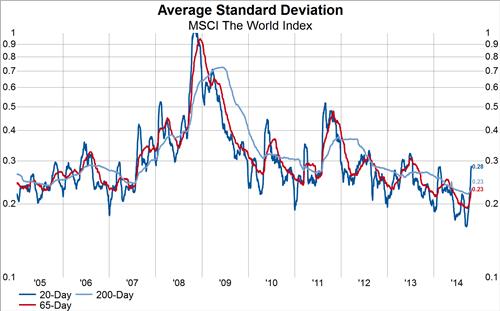

The average realized standard deviation for developed markets stocks as moved from an all-time low back to levels that are usually at the low end of the typical range.

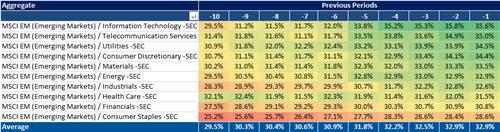

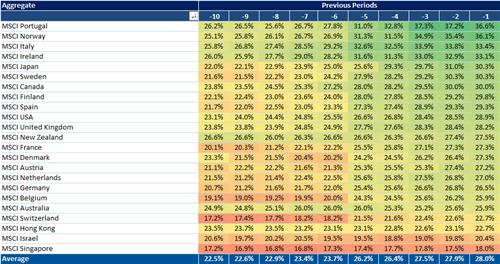

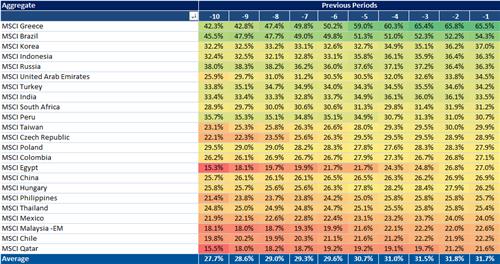

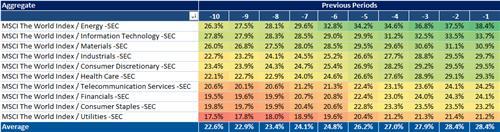

In the four tables below we can see that the average volatility by both country and sector is moving from yellow (low) to green (high). In the below tables we are looking at the progression of 20-day average volatility over the last 10 days.

Developed Markets Realized 20-day Volatility by Country

Emerging Markets Realized 20-day Volatility by Country

Developed Markets Realized 20-day Volatility by Sector

Emerging Markets Realized 20-day Volatility by Sector