Crude oil prices have dropped sharply over the last few months thanks to abundant global production and signs of slowing global economic growth. Lower oil prices could inject spending power into the economy as consumers eventually pay less for gasoline and open their wallets in other areas. This would provide a positive shock and potentially bolster the performance of consumer discretionary shares.

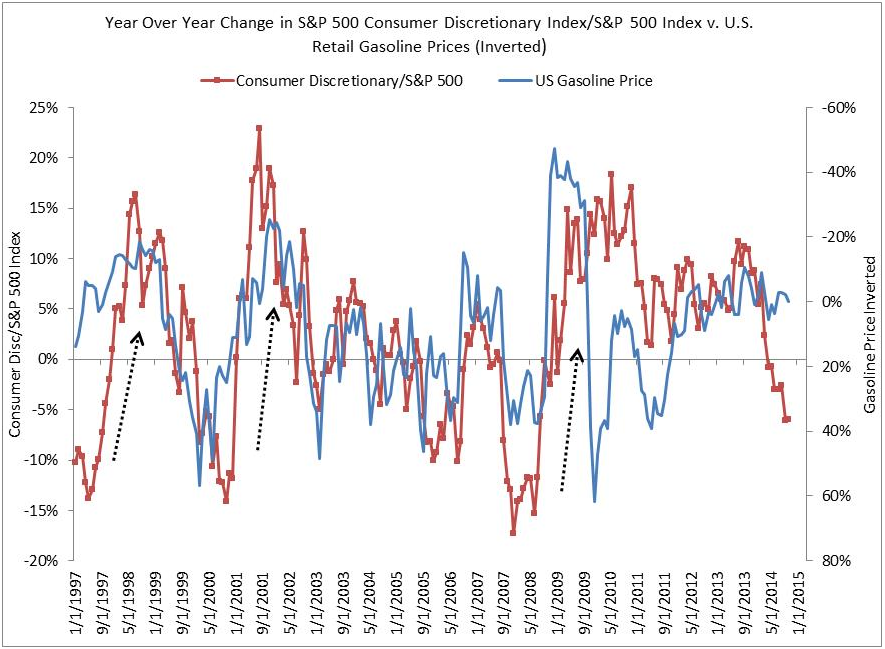

Historically, there has been a robust relationship between the performance of consumer discretionary shares and changes in gasoline prices. The graphic below displays the relationship between the year-over-year change in the price of the S&P 500 Consumer Discretionary Sector Index relative to the price of the S&P 500 Index against the year-over-year change of US retail gasoline prices. The price change of gasoline is inverted in the graphic to correspond visually to the outperformance or underperformance in consumer discretionary stocks when crude oil prices rise and fall. The graphic suggests that a meaningful decline in the year-over-year gasoline prices may lead the consumer discretionary sector to outperform the S&P 500 Index. This happened in the late 1990s, early 2000s, and 2009 — illustrated by the arrows on the graphic.

The graphic also indicates that consumer discretionary stocks have been underperforming the S&P 500 in recent months despite the outlook for healthy holiday sales and continued growth in job creation. The National Retail Federation recently projected holiday sales would rise 4.1% in 2014 — the most since 2011. The current weakness may present an opportunity.

Source: Bloomberg, Oct. 10, 2014. Past performance cannot guarantee comparable future results.

Even though oil prices have dropped sharply, the impact has not been dramatic at the pump, yet. The most recent data from the Department of Energy suggests that the national average price of retail gasoline is just below $3.30/gallon and little changed from a year ago. Using monthly data and providing some context, the retail price averaged $3.31/gallon in the fourth quarter of 2013 and $3.49/gallon in the first quarter of 2014. Gasoline prices peaked at $3.71/gallon in April 2014, creating a recent high water mark and easy year-ago comparisons into the spring of 2015.1

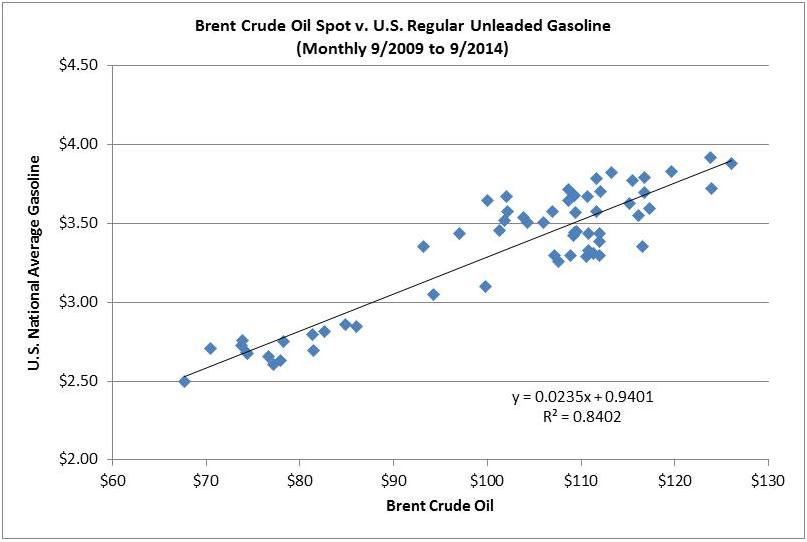

US gasoline prices are priced off of Brent crude oil, which is the global benchmark instead of West Texas Intermediate (WTI) due to transportation bottlenecks and the inability to export US crude oil. Examining the relationship between the US retail price of gasoline and Brent over the past five years indicates that $90 Brent projects US gasoline at $3.06/gallon. A Brent price of $80 implies a national average gasoline price of $2.82/gallon. Loosely speaking, a move in gasoline to $3.05/gallon in January 2015 would cause gasoline prices to be down about 7.1% year over year, while a move to $2.82 would cause gasoline prices to be down 14.4% year over year. At writing, Brent was priced at $88.60/barrel.2

Source: Bloomberg, Oct. 10, 2014

Consumer discretionary shares do face the headwind of slower refinance activity and a very weak rise in wage growth, but those who think that oil prices will stay low or fall even further should consider holding stocks in the consumer discretionary or retail sector. Lower oil prices could inject spending power into the economy – providing a positive shock and bolstering the performance of consumer discretionary shares. One risk to the favorable impact of lower energy prices would be a widespread outbreak of Ebola that freezes travel and restrains economic activity.

1 Source: Bloomberg LP as of Oct. 10, 2014

2 Sources: Bloomberg LP and Invesco PowerShares as of Oct. 10, 2014

Important Information

*Within the past 12 months, changes to the Funds’ name and investment objective have occurred. For more information about these changes, please see the Fund’s prospectus.

The S&P 500® Index is an unmanaged index considered representative of the US stock market.

The S&P 500® Consumer Discretionary Index is an unmanaged index considered representative of the consumer discretionary market.

West Texas Intermediate (WTI) is light, sweet crude oil commonly referred to as “oil” in the Western world. WTI is the underlying commodity of the New York Merchantile Exchange’s oil futures contracts.

There are risks involved with investing in ETFs, including possible loss of money. Shares are not actively managed and are subject to risks similar to those of stocks, including those regarding short selling and margin maintenance requirements. Ordinary brokerage commissions apply. The Fund’s return may not match the return of the Underlying Index.

Investments focused in a particular industry or sector, such as the consumer discretionary sector are subject to greater risk, and are more greatly impacted by market volatility, than more diversified investments.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.All data provided by Invesco unless otherwise noted.

©2014 Invesco Ltd. All rights reserved.