It is customary to think of “Risk Parity Asset Allocation” and “Carry Trading Strategy” as two different things. We explain that the Risk Parity after the Global Financial Crisis is nothing else but a hugely successful Global Carry Trade funded in Japanese Yen, Dollar and Euro. The performance of this trade is fantastic, the allocation is huge (100s of blns of $) and the risk of crash that will precipitate the next financial crisis is growing day by day. But for now the music is still playing.

Conventionally “Carry” and “Risk Parity” are defined as follows

- Risk Parity is an approach to investment portfolio management which focuses on equal allocation of risk, usually defined as volatility, rather than allocation of capital;

- The Carry of an asset (or assets) is the return obtained from holding it assuming that market conditions, including its price, stays the same.

So “Risk Parity” is a kind of allocation and “Carry” is a kind of expected return. In fact Carry return is what you get by allocating according to Risk Parity.

The importance of Global Carry trade which was funded in Japanese Yen before the Global Financial Crisis is hard to underestimate and it was explained in great details by Independent Strategy[1] who also explained why and how of financial crisis before it started in 2007.

Question: So is there a Global Carry Trade after 2008?

Answer: Yes and it is as alive and as successful as it ever was, it mystically transmuted and “IPO-ed” itself (went public) under the glamorous name of Risk Parity and has hundreds of billions invested in it.

Question: How did it work since 2009?

The Global Carry is funded in Japanese Yen, Euro and Dollar and is invested in US bonds and equities in Risk Parity manner, meaning equal risk allocation to equities and bonds. Below is the futures basket exemplifying Global Carry:

The futures in the basket are as follows:

The performance of this basket since 2009 was fantastic. Note the period of abrupt volatility it hit last summer on Taper Tantrum.

This trade was easily proxied by a pair of spx and 10y treasury futures and could have been leveraged enormously given its volatility was so low.

Question: How did it work over the last year?

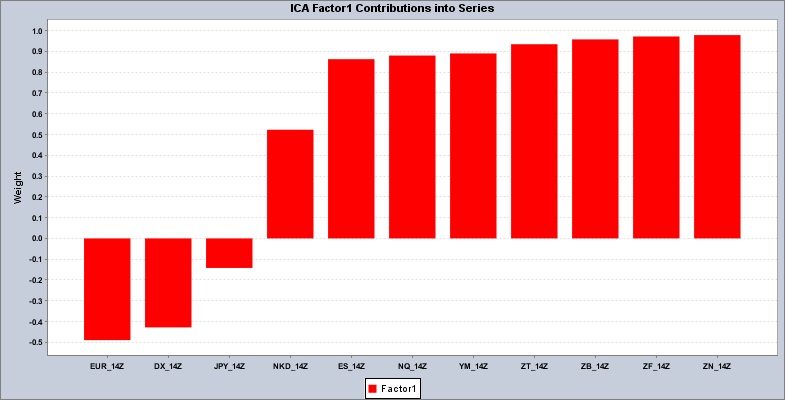

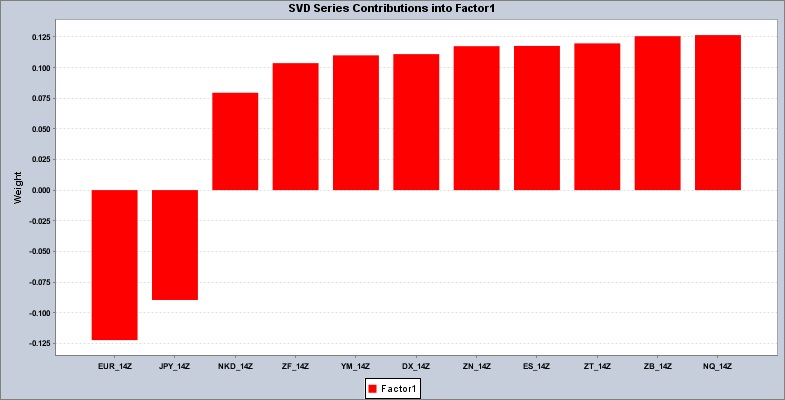

Over the last year as Japanization of Europe financial markets is getting complete the Euro got even more important as a funding currency for Risk Parity weighted Global Carry basket:

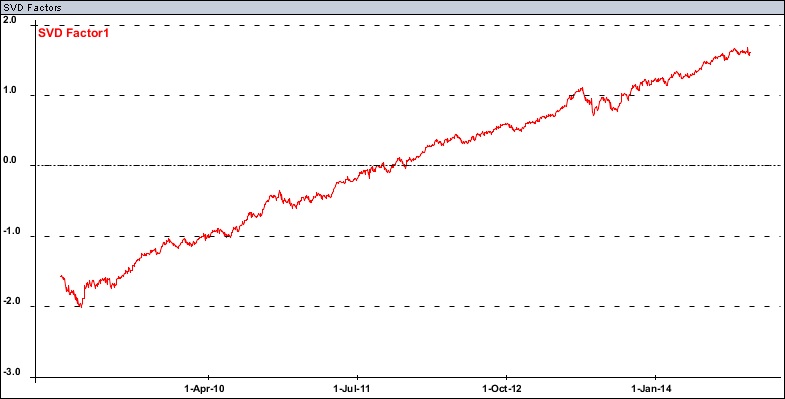

Below is the basket performance:

This trade is easily proxied by a basket of us dollar index, dow jones and a couple of 5y treasury futures.

Of course Global Carry Trade goes far beyond the US equities and bonds to global sovereigns bonds, currencies, credit and equities (we intentionally simplified our basket) in a not so complicated way. It is all driven by the same music though and risk of this music stopping is growing day by day. We have seen how it might look like during the Taper Tantrum which was just a slight volatility in Global Carry Trade. One can only imagine what happens if the music really stops. This is the most important metric to watch.