- Fed becoming wary (again) on global growth

- Slumping commodities signaling a deflation warning

- Municipal bond investors continue to benefit from falling yields and maturity “roll-down”

- Strong municipal market presents year-end 2014 tax-swapping opportunities

The never-ending debate over when the U.S. central bank will reverse course on its near-zero short-term interest rate policy continues to rage. Continued improvement in the U.S. economy, a drop in the unemployment rate to 5.9% last month, and generally good business performance through the first three quarters of the year, have lent strong support to the “sooner rather than later” camp that has been calling for the normalization of rates to commence. What seemed possible this past summer appears much less so as the fourth quarter unfolds.

Further weakness is evident in European and emerging market economies. Rapidly deteriorating commodity prices underscore the softness in global demand. Nowhere is this fact more evident than in the energy sector. Crude oil prices have plunged more than 20% since mid-year. Global deflation is once again a serious threat. Further geopolitical unrest and the spreading Ebola virus present additional threats to world economies. The U.S. dollar has strengthened, making American goods, including the commodity complex (priced in U.S. dollars), more expensive abroad. Wall Street stock analysts are rightfully concerned about the possible future earnings consequences for domestic companies that compete in foreign markets. Based on the pressure currently being exerted on global equities, investors are reacting by reducing stock exposure. For now, the “later rather than sooner” consensus clearly has the upper hand. An increasing number of bond market participants are predicting new lows for benchmark sovereign debt yields.

The widely anticipated back-up in bond yields, including municipal bonds, has yet to materialize to a significant degree. While tax-exempt yields did follow Treasuries higher during September, the snap-back has been fast and significant; yields have recently established new twelve-month lows. Portfolio managers have reportedly been holding larger than normal cash reserves for many months in anticipation of a surge in new tax-exempt issuance. To the contrary, supply has not meaningfully increased. Meanwhile, investors appear to be repositioning from equity and other asset classes into fixed income. The move to bonds includes municipal securities, as evidenced by strong flows into tax-exempt funds, which is forcing cash-laden portfolio managers to buy at the highest prices of the year.

Interestingly, the recent market advance has not been equally proportional along the tax-exempt yield curve. Both intermediate-term and long-term bond yields have slid significantly more than those bearing short maturities or that are nearing their optional call redemption dates. The result of the disproportionate price rally has led to further flattening of the yield term structure that encompasses securities maturing from 1-30 years. Rate compression has led to a very significant flatting of the rate differential between the shortest and longest maturing tax-exempt bonds. The more significant decline in yields in the 10-year and longer maturities, multiplied by their longer durations (i.e., greater price change for the same yield change) has translated into generally better performance for this sector of the market. As illustrated in the table below, the modest peak in yields attained in September has reversed significantly lower in just the first seven trading days of October.

“AAA” Municipal Yields - 5% Coupon

|

Maturity (Years) |

10/9/2014 |

9/30/2014 |

8/29/2014 |

Change 7 Days 9/30-10/9 |

Change 21 Days 8/29-9/30 |

|

2015 (1) |

0.13% |

0.13% |

0.12% |

0.00% |

+0.01% |

|

2019 (5) |

1.10% |

1.17% |

1.08% |

-0.07% |

+0.09% |

|

2024 (10) |

2.01% |

2.17% |

2.07% |

-0.16% |

+0.10% |

|

2029 (15) |

2.35% |

2.55% |

2.51% |

-0.20% |

+0.04% |

|

2034 (20) |

2.65% |

2.83% |

2.79% |

-0.17% |

+0.04% |

|

2044 (30) |

2.92% |

3.09% |

3.03% |

-0.17% |

+0.06% |

|

Spread 1-30 yrs |

2.79% |

2.86% |

2.92% |

-0.07% |

+0.06% |

Source: Thomson Reuters MMD

Past performance doesn’t guarantee future results.

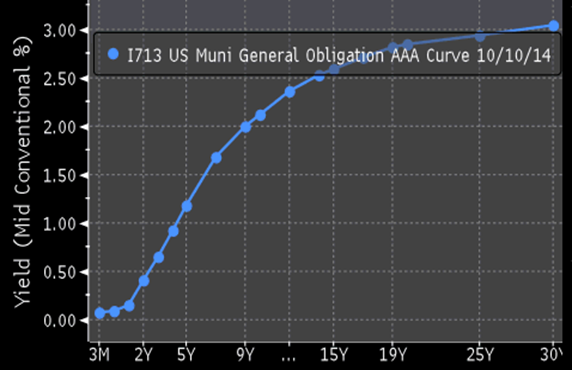

SMC FIM has been employing a strategy to selectively reduce exposure to short-maturity (1-5 years) bonds and securities that the issuer has the option to redeem within this time period. As exhibited since the start of the fourth quarter, this maturity spectrum will significantly underperform long-dated bonds if rates continue to fall. More importantly, investors should expect the short-end of the yield curve to also be most vulnerable to the Fed’s eventual rate rise that markets have been expecting. Purchasing intermediate maturity bonds with the sale proceeds should continue to prove beneficial regardless of any directional rate move. Even though the yield curve has flattened from a 4.01% yield spread (1-30 years), at the beginning of 2014, to 2.79% currently, there still exists a significant degree of steepness (yield differential) between successive maturities in intermediate (10-20 years) bond maturities. Investors are likely to benefit from the gravitational pull on these bonds as they become shorter in maturity.

“AAA” Municipal Bond Yield Curve

Source: Bloomberg

The potential performance advantage of purchasing intermediate-maturity bonds rather than higher yielding, long-term bonds makes sense in the current rate setting. For example, in today’s low interest rate environment, an investor can decide between two options: a 10-year maturity bond yielding 2.10% or a 30-year bond, callable in ten years, that yields 3.00% in order to pick-up an additional 90 basis points of return. Assuming no change to yields over a one-year time horizon, the 10-year bond will become a nine-year bond yielding 2.00% The yield curve “roll-down” generates an additional 0.75% of price gain in excess of the bond’s book value; adding the initial 2.10% yield nets the investor in the ten-year bond a 2.85% twelve-month return, compared to 3.00% for the 30-year bond that does not benefit from the yield “roll-down” due to the curve’s flatness. While only forgoing an extra 15 basis points of return, maturity extension is reduced from 30 to 10 years, leaving the investor better insulated from a portfolio loss due to rising rates.

As December 31 draws closer, we are advising clients to evaluate whether tax swapping is appropriate for year-end tax planning. The significant gains achieved might be useful in offsetting losses incurred in other asset classes. Harvesting portfolio gains after a period of unprecedented market strength should be considered. The current environment can be taken advantage of to increase portfolio yield with minimal maturity extension. We do not anticipate municipal market action in 2015 to be as one-way as experienced this year. Volatility should be on the increase regardless of what the Fed decides to do or not to do.

Disclosures

The information provided in this commentary is not intended to be a complete summary of all available data. Certain information contained herein has been obtained from published sources and/or prepared by sources outside SMC Fixed Income Management (“SMC FIM”), a division of Spring Mountain Capital, LP, and certain information contained herein may not be updated through the date hereof. While such sources are believed to be reliable, no representations are made as to the accuracy or completeness thereof by SMC FIM or any of its affiliates, directors, officers, employees, partners, members or shareholders, and none of the former assumes any responsibility for the accuracy or completeness of such information. Nothing contained herein shall be relied upon as a promise or representation as to past or future performance.

This commentary does not constitute an offer to sell or a solicitation of an offer to purchase securities, or any other product sponsored or advised by SMC FIM or its affiliates, nor does it constitute an offer or a solicitation to otherwise provide investment advisory services. It should not be assumed that any of the security transactions listed were or will prove to be profitable, or that the investment recommendations we make in the future will be profitable.

Statements contained in this commentary that are not historic facts are based on current expectations, estimates, projections, opinions and beliefs of SMC FIM. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Unless specified, any views reflected herein are those of SMC FIM and are subject to change without notice. SMC FIM is not under any obligation to update or keep current the information contained herein.

This commentary does not take into account any particular investor’s investment objectives or tolerance for risk. The information contained in this commentary is presented solely with respect to the date of its preparation, or as of such earlier date specified in it, and may be changed or updated at any time without notice to any of the recipients of it (whether or not some other recipients receive changes or updates to the information in it).

No assurances can be made that any aims, assumptions, expectations, and/or objectives described in this commentary will be realized. None of SMC FIM or any of its affiliates, directors, officers, employees, partners, members or shareholders shall be liable for any errors in the information, beliefs, and/or opinions included in this commentary or for the consequences of relying on such information, beliefs, or opinions.

Neither this commentary, nor any of the contents hereof, may be reproduced or used for any other purpose, or transmitted or disclosed in whole or in part to any third parties, in each case without the prior written consent of SMC FIM.

Copyright © 2014 Spring Mountain Capital, LP. All rights reserved.