US equities are deeply oversold by many measures, and are likely to bottom here. But what if we “crash”? While market crashes are impossible to predict, it’s wise to be prepared for the occasional plunge from deeply oversold territory.

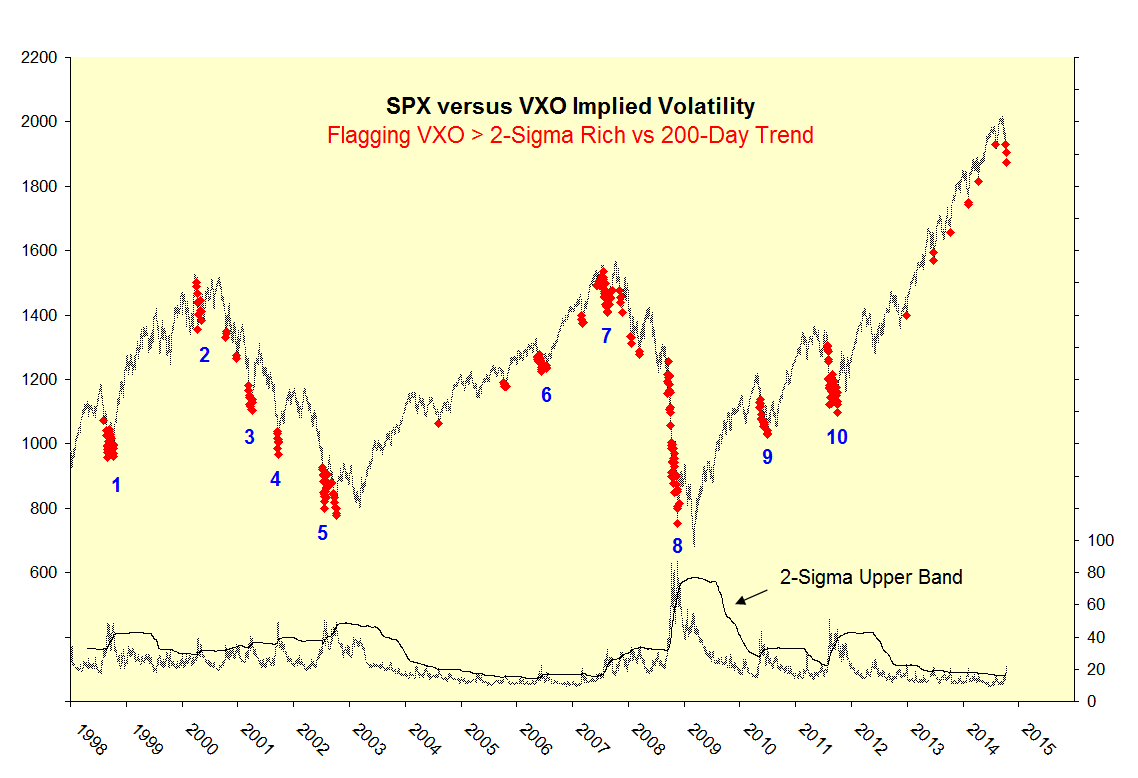

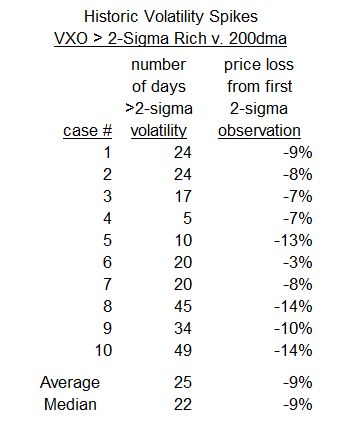

From the perspective of implied volatility, there were ten occasions over the past sixteen years when volatility spikes were more than temporary. These cases are illustrated in the chart below.

Here, a crash is defined as an event in which implied volatility (VXO) spikes above its 200-day moving average for five or more trading sessions. This hasn’t happened yet, but if it does, the table below might come in handy. The median crash generated greater-than-2-sigma volatility for 22 non-consecutive trading sessions. The median price loss was 9%, counting from the first 2-sigma observation.

If the median crash were to repeat here, SPX would drop to 1760 before bottoming in early November. Remember, this is not a prediction, but something to keep in mind if the unexpected should happen. A move to 1760 would constitute a 13% correction from the September 2014 top and a re-test of the February 2014 bottom. In other words, a fairly normal event by market standards.

Contemplating a hypothetical crash based on historic parameters is a useful exercise. While a crash is unlikely, it’s wise to remember the old scout saying: “Be prepared.”