Much press attention has posed the question of whether China has become more confrontational toward U.S. businesses and other foreign firms. The Middle Kingdom stands accused of protectionist policies that restrict access to many markets in order to protect its domestic firms. But in today’s world, what exactly is protectionism, and who are these protections meant to benefit? The standard definition is: government actions and policies that restrict or restrain international trade, often with the intent of protecting local businesses and jobs from foreign competition.

First, let’s consider the usual protectionist policies used to benefit industries. These include import tariffs, restrictive maximum import quotas and other government regulations designed to reduce competitiveness among imported goods and services versus those offered domestically. As a result, the cost and availability of certain protected goods are not determined by underlying economics. Thus, this tends to hurt consumers. Is China still protecting Chinese companies or has it actually shifted its focus to protecting consumers? Amid a revival of concerns over U.S.–China trade protectionism, it’s important for us to peek beneath the covers to try to understand motives behind some recent actions that may impact our investible universe.

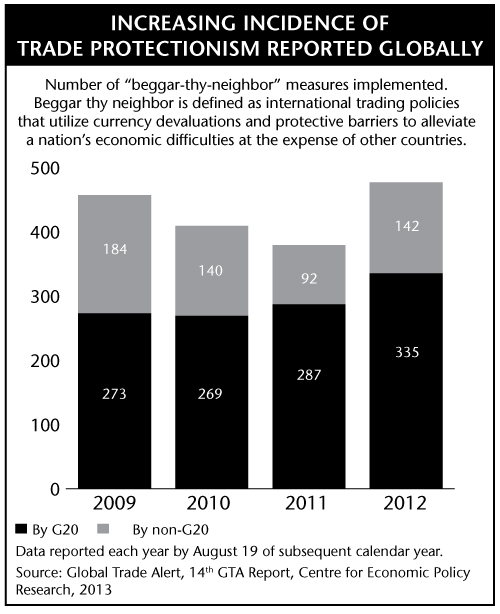

Since the onset of the Global Financial Crisis in 2008 and the subsequent “Great Trade Collapse,” many countries—particularly the U.S.—have actively pursued trade policy instruments as part of their response to boost domestic economic activity and curb unemployment. The following figure from the Global Trade Alert’s latest report on protectionism shows two–perhaps surprising–things: 1) protectionism is not slowing down and 2) G–20 nations are relatively heavy offenders.

Even though empirical evidence demonstrates that protectionism, over the long run, tends to do more harm than good to a country’s economy, many countries still resort to such practices during economic downturns, with GDP deceleration and currency appreciation being key triggers. For example, since 2008, a one percentage point drop in real domestic GDP growth typically led to a 4.4% increase in newly implemented trade-restrictive measures. If negative long-term consequences of trade protectionism are well-documented, then why do countries continue to ignore such evidence? Different countries have different motivations and urgencies over time. Understanding these motivations could lead to fruitful investments and help in avoiding unsustainable hype.

A noted U.S. protectionist program, introduced in 2009 in the wake of the financial crisis, was the American Recovery and Reinvestment Act in which the government proposed to inject US$831 billion domestically to stimulate U.S. growth and employment. The controversial protectionism feature of this act was a “Buy American” provision, which triggered international concern—including a stern warning from the European Union. The U.S., perhaps motivated by shorter-term objectives, ignored most threats from its trade partners and proceeded with the program, largely on the basis of saving jobs. Despite this, unemployment remained elevated through mid-2011. Overall, the U.S. methods of protectionism are in-line with average practices within the G–20, according to the Center for Economic and Policy Research.

A New Purpose in China

Across the Pacific, we find China now facing similar criticism following its recent anti-monopoly probes against international firms operating on its soil. By way of background, China is no stranger to implementing protectionist policies. From increasing import taxes on U.S. chicken in 2010 to subsidizing Chinese auto-parts makers in 2009, China’s past protectionism policies favored domestic companies at the expense of consumers. However, we sense a different motive for the recent, heightened wave of anti-monopoly investigations by the Chinese government. The protection has shifted from protecting domestic companies to protecting domestic consumers.

China’s anti-monopoly investigations have been ongoing since 2008. However, the frequency of investigations, breadth of industries covered and escalation of penalties have heightened concerns. Though it is near impossible to forecast any government’s policy, we wanted to try to understand the possible motivations to see what investment conclusions could be drawn. While the vast majority of the firms targeted by such policies are non-Chinese, a small percentage of domestic firms are also affected. We analyzed several recent Chinese anti-monopoly cases carefully—including domestic spirits producers, LCDs panels, domestic banks, domestic telecoms and semiconductors. In each case, the government is mandating reduced prices or imposing heavy fines on these industry participants for anti-monopolistic pricing in efforts to lower the cost burden for end users. This is contrary to the traditional definition of protectionism in which prices are kept artificially high to foster domestic industry growth at the expense of consumers.

If these so-called anti-monopoly cases in China don’t fit the typical definition of protectionism, why has the foreign press been so harsh on the Chinese government for looking out for its 1.3 billion people? This may be because a significant proportion of the high-profile cases appear to involve big foreign firms with lack of due process and transparency. The prevailing concern is that China may be using its six-year-old anti-monopoly law to advance its “industrial policy goals.” This was suggested in April, when the U.S. Chamber of Commerce sent a private letter to Secretary of State John Kerry and Treasury Secretary Jacob Lew, demanding that Washington get tough with Beijing.

However, under further analysis, motives for China’s anti-monopoly movement may be interpreted simply as an aim to gain popularity and improve economics. Along with the anti-corruption movement, the anti-monopoly movement is welcomed by Chinese citizens and has boosted the approval ratings of China’s new leadership. On the economic front, as the return on fixed asset investments continues to decline in the Chinese economy, GDP growth has relied on more loans and borrowings. This is obviously not a sustainable growth path, and a shift toward sectors that carry over more sustainably to household income and consumption are critical for the Chinese economy’s structural reform. To increase the effectiveness of consumer spending toward boosting GDP, the government most likely examined the large-ticket items in its consumer’s daily lives. Property, autos, child care, education, electronics and health care unsurprisingly take up significant wallet share. In order to speed up—or in more technical terms, increase the multiplier effect of—the consumption economy, China needs to find ways to reduce “unfair” pricing practices of consumer goods companies. Excluding the impact from taxes and levies, we find that prices of many imported goods such as milk powder, auto parts, phones and drugs are indeed much higher in China compared to developed nations in Asia and beyond. This obviously stands in the way of the government’s push for a more efficient use of consumer savings. Because of this, the government is likely to scrutinize pricing policies if it finds that sufficient explanation for why a certain product is priced higher in China compared to neighboring countries is lacking. Thus, it is understandable that these investigations could actually be part of a bigger plan to transition the structure of the Chinese economy.

Other policies in this drive toward a consumption-led economy include control of property prices—another big ticket item that has been crowding out consumer spending. We expect protectionism of the consumer to continue in the future, given our view of potential motives. This may create some near-term pressure on domestic industries as they now have less price protection versus imported goods. However, in the long run, this could be a positive move. A more competitive market dynamic generally accelerates operating efficiencies and may quicken the pace of innovation among domestic players. Operating efficiency and innovation are often important drivers of sustainable earnings growth for companies, and we are excited to search for compelling investments in these industries. For the targeted multinational companies operating in China, we believe the vast market opportunity in China still make it a compelling place to do business despite near-term headwinds.

:

:

Besides protectionism of physical goods and services, another often-discussed area of protectionism revolves around digital data security and national security. The National Security Agency (NSA) scandal involving NSA contractor Edward Snowden and concerns around how digital data will be traded among Trans-Pacific Partnership members renewed the debate about digital trade. The Software Alliance, also known as BSA, that is the leading global advocate for the global software industry argues that, “Current global trade rules provide few protections to limit countries from imposing restrictions on cross-border data flows… Technical regulations, especially specific technology mandates, can significantly impede innovation and create unnecessary barriers to trade, investment and economic efficiency.” To argue the value of national security against the added benefit of economic efficiency from a boundless flow of digital information is difficult. However, just pragmatically looking at the numbers, starting in 2013, China imported more in semiconductors (integrated circuits) than it did oil. This naturally draws protectionism to the semiconductor and technology sectors, given the data security risk embedded in nanometers of silicon.

As a result, we also believe continued localization of China’s IT sector could drive interesting investment opportunities. China is also trying to bypass protectionist policies abroad that are imposed by others. The more successful cases have been through international mergers and acquisitions (M&As), for example in the information technology and solar industries where Chinese companies have expanded their manufacturing, research and development overseas to avoid protectionist import taxes or restrictive import quotas for importing goods to the U.S. As a result, we are encouraged by the continued efforts in financial reform toward liberalizing Chinese capital accounts for cross-border investments. It is also exciting that more companies may benefit from cross-border M&As.

“The future of trade policy is at the intersection of law, economics, politics and domestic policy,” said Chad Bown, lead economist of the World Bank research department. Indeed, as complexity increases ahead, we continue to focus on finding new and compelling investment trends.

Tiffany Hsiao, CFA

Senior Research Analyst

Matthews Asia

© Matthews Asia