We bought a business today. I don’t know what the stock market is going to do today, this month or next year. I do know how to pick out a reasonable business to own for 10 to 20 years, and a lot of other people do too, incidentally. --—Warren Buffett on CNBC Squawk Box, October 2nd, 2014

Dear Fellow Investors,

We’d like to ask a self serving and much nuanced question: is your active equity portfolio manager buying businesses for you or are they trying to guess what the stock market will do in the next month or few years? Much like Samuel L. Jackson asks, “What’s in your wallet?” in television commercials, we’d like to ask, “What’s in your portfolio”? To us at Smead Capital, this is the single most important question in the world of manager search and asset allocation. It is also at the center of the debate about passive versus active management in U.S. equity investing. Dr. Eugene Fama, the darling of the efficient market theorists, said recently that active management is a “fallacy”. In effect, Fama is trying to convince investors to give up on the idea that someone can select common stocks and add value over an extended time period.

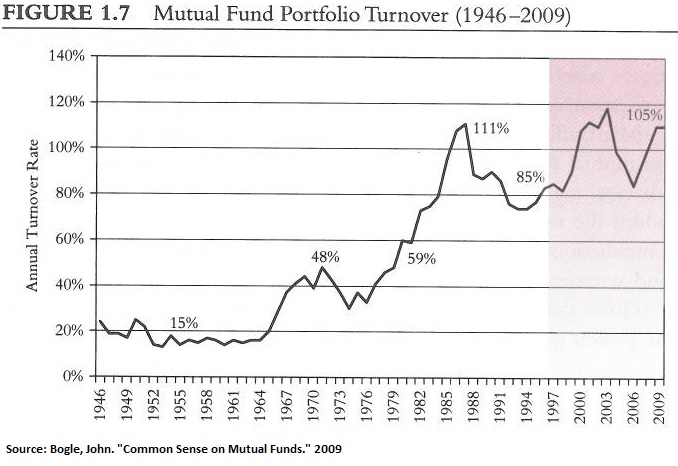

In his latest CNBC appearance, Buffett said loudly and clearly that he believes many people can pick out reasonable businesses to own for 10 to 20 years. The active management community has left itself wide open to attacks from the efficient market/passive investments folks in the process. As information and news have been provided more and more quickly, portfolio managers have accelerated the pace of portfolio turnover. Owning businesses for ten years has taken a back seat to quantitative analysis on 6 to 12-month price swings and inexpensive ETF participation in tactical allocation decisions. All of these forces breed activity and/or expense. See the chart below:

We don’t disagree with Fama that stock picking organizations which “rent” rather than “own” businesses in the stock market are at a massive disadvantage to low-cost indexes. In the large-cap space alone, the latest research in the Financial Analysts Journal in February of 2013 shows that the average large-cap fund spends 0.81% annually in trading costs associated with average portfolio turnover of 62%. How does a 1.6 year holding period compare with owning most of your portfolio for 10 years? To us, the possibility of adding high trading expenses to the annual fee of a separate account or annual mutual fund expense is a hurdle that most active managers can’t overcome in long durations. Investors have been voting with their feet, especially in the large-cap space. Here is how Morningstar explains this in their October/November 2014 edition of Morningstar Magazine through an article by Jeffrey Ptak called “Death of Active?”

One of the biggest stories of recent years is the rise of passive investing. In June 2009, active funds accounted for 79% of fund assets (active U.S. stock funds had a 31.7% market share). Fast forward five years, and that figure had shrunk to 71.5 (28.7% for U.S. stock funds), the incursion by passive funds accounting for the 7.5% erosion. That’s a big number.

Buffett likes to remind investors that “excitement and expense are the enemy of your portfolio.” On top of costing an average of 0.81% annually on trading cost alone, the high turnover mathematically cuts into the performance of what turn out to be some of the best long-term performers in the portfolio. We think the math of common stock investing is fairly simple: a multiple decade winner growing too many times your original investment covers a multitude of small losses. Mr. Buffett reminds almost every audience he speaks to that his sins of omission (winners sold to soon) dwarf the impact of his sins of commission (poor performing stocks he bought).

We think there is a business reason why active managers practice what we consider to be injuriously high turnover and implement market timing techniques. They think investors want their returns smoothed and will leave the current portfolio manager if they don’t. It is our opinion that these U.S. equity fund managers believe this because they have seen how funds which outperformed in 2008 have received a large part of the active large-cap fund flows from 2009 to 2013. They also seem to get very high research ratings from vetting organizations for that same reason. When Warren Buffett hired Todd Combs and Ted Weschler, he was asked by Becky Quick on CNBC if he hired them because of how well they defended their capital in 2008. Buffett quipped, “I wouldn’t have hired anyone who didn’t get slaughtered in 2008.”

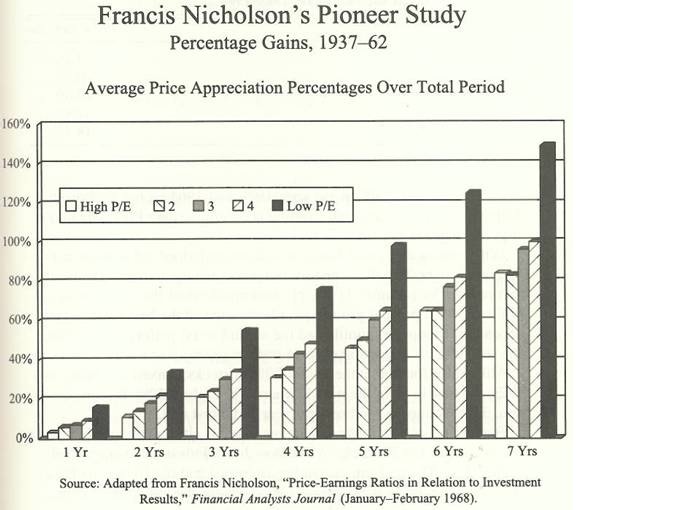

Our investment philosophy rests on three main tenants. First, valuation matters dearly. We agree with Fama/French, David Dreman, Bauman/Conover/Miller and Francis Nicholson, who proved academically that cheap stocks outperform average or expensive ones. Buffett probably likes Francis Nicholson’s study because it didn’t rebalance annually and saw the outperformance grow as the holding period lengthened. It’s possible we wouldn’t know who Warren Buffett is if his bargain purchases of attractive long-term businesses in the stock market hadn’t been held for 20 years or more.

Second, we want to own part of a business on behalf of our clients for a long period of time. We think it is the companies which create wealth, whereas most investors in hedge funds and in actively-managed strategies put their faith in the frictional changes which are made fairly often by what they think are brilliant money changers. We think this is the “fallacy” to which Fama speaks.

Lastly, we believe that in order to hold businesses for 10 to 20 years you need them to be high quality businesses. Everyone has their ups and downs, even companies. Strong balance sheets, wide moats and consistent free cash flow are among a series of qualitative aspects which can get a company through life’s ups and downs. Johnson and Johnson (JNJ) survived the Tylenol poisonings of 1984, Exxon (XOM) survived the grounding of the Valdez in 1989 and Merck (MRK) survived the Vioxx trials and recall of 2003-2007. They had qualitative strengths which got them through very difficult circumstances.

It is encouraging and refreshing to hear Mr. Buffett reiterate his belief in the selection of reasonable businesses for 10 to 20 years. How much market share must be taken away from the actively-managed equity community before they recognize the error in their ways? Capital gravitates to where it gets treated the best. We would expect to see those who screen equity portfolio managers gravitate toward stock-pickers who practice the discipline of “owning” companies rather than “renting” even as passive gains in popularity.

Warmest Regards,

William Smead

The information contained in this missive represents SCM's opinions, and should not be construed as personalized or individualized investment advice. Past performance is no guarantee of future results. Bill Smead, CIO and CEO, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. A list of all recommendations made by Smead Capital Management within the past twelve month period is available upon request.