This year sector rotations were quite dramatic with late/early, recession and growth/value baskets swinging back and forth all along. By and large these rotations explain essentially all US equities market prices action at the level of sectors. We are taking a closer look at this year rotations, at this week action and where it can end up next as well as how to take advantage of it.

At the level of sectors US equity market is essentially driven by four factors:

- Market itself (SPX)

- Recession sector rotation (staples+utilities vs technology+industrials)

- Late/early cycle sector rotation (energy vs discretionary)

- Growth/value sector rotation (growth vs value)

Let us quickly go through all of these.

- Market factor (Factor1) and SPX are portrayed below. Here one can see the recent correction taking place with nothing looking too aggressive so far. Time to buy the dip?

- Recession sector rotation factor (Factor2) and staples+utilities vs technology+industrials basket with market component hedged out by SPX are portrayed below. We also show full reconstruction of the basket which includes some minor contributions from other factors. One can see recessionary rotation picking up from the beginning of the year till the end of April and subside afterwards though being volatile. Interestingly there was also a recent pickup in recession sector rotation late this week.

- Late/early cycle sector rotation factor (Factor3) and energy vs discretionary basket are portrayed below. We also show full reconstruction of the basket which includes some minor contributions from other factors. Where was aggressive late cycle rotation starting mid-March this year (post March FOMC) and peaking at the end of June (post June FOMC) and still aggressively ongoing rotation back (early cycle rotation) since the end of June. There is still some room to go.

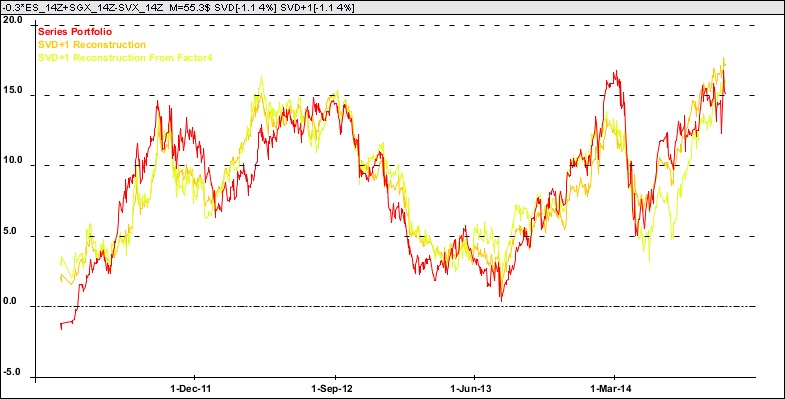

- Growth/value sector rotation factor (Factor4) and growth vs value basket with market component hedge out by SPX are portrayed below. We also show full reconstruction of the basket which includes some minor contributions from other factors. We use Citigroup Growth and Value indices as proxies for growth and value. No luck of action here as well. Overreacting growth momentum peaked at the end of February, crashed, bottomed mid-April and has been picking up since in very volatile way. In particular there was recent drop on Friday 25th (PIMCO) which was pure dislocation and recovered since. All in all this factor seems to be quite stretched and rotation back to value might follow unless we see some growth materializing in Q3-Q4.