Uncertainty in markets, economy puts focus on stock picking

Tracking the Fed

The U.S. Federal Reserve (Fed) has indicated it will stop buying U.S. Treasury bonds and mortgage-backed securities – the “taper” of its QE3 program – by the end of October. The Fed also has said it will keep interest rates at a very low level for a “considerable time.”

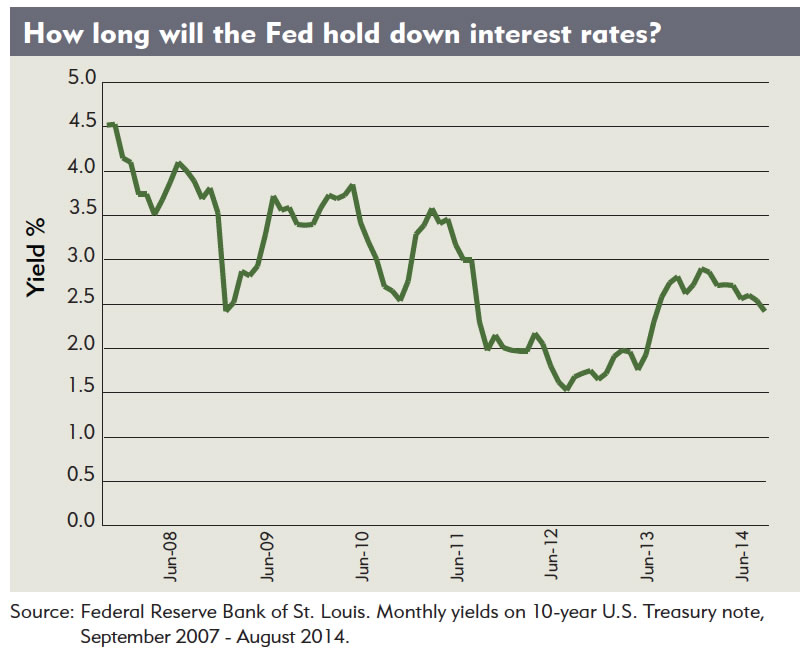

Markets now expect interest rates to begin rising some time in 2015, and possibly as soon as June, from levels near zero since the global financial crisis that began in 2008. Yields on the 10-year U.S. Treasury today are around 2.6%. That’s roughly 1 percentage point higher than the level of May 2013, when the Fed introduced the idea of ending QE3, but down from forecasts coming into 2014 of 3.0 to 3.5%. This is despite a prolonged period of what we consider unconventional monetary policies by global central banks.

Market volatility has increased in the past when the Fed implied it would make changes. As it brings the taper to a close, articulates an exit strategy for the additional securities on its balance sheet and proceeds to raise interest rates, we think those market adjustments will persist. We believe this is a critical period for Fed communication and implementation, and think any missteps could be a detriment to the ongoing economic recovery.

We also think volatility could increase dramatically if the markets were to believe interest rates would increase too quickly or that the process of unwinding the Fed’s balance sheet could destabilize the economy. In our view, the Fed does not want to induce such a choppy environment and will be cautious with policy announcements. We think the likely outcome is a period of interest-rate fluctuations as the bond market tries to anticipate the Fed’s future moves, with rates toward the lower end of a 2.5 to 3.5% range.

The macro view

We think the global economy remains, at least somewhat, in the crisis that began in 2008. Central banks around the developed world are trying to fight disinflationary or deflationary trends and spur economic growth. However, we believe the fundamentals supporting the U.S. economic recovery are in place and provide a backdrop for better sentiment and spending from here.

We do not think there will be a sharp upturn in U.S. economic growth but believe real gross domestic product (GDP) is likely to be positive and stay at a lower growth rate than previous cycles.

Heightened geopolitical risk in areas such as the Mideast and Russia/Ukraine lingers to some degree in market sentiment, but the ill effects from recent flare-ups have been short lived and commodity prices have moved lower, not higher. These events have made “safe harbor” markets even more attractive and supported valuations at higher levels than fundamental factors might have indicated. We believe this is another factor behind this year’s steady gains in U.S. equity and credit markets.

Focus on stock selection

There is an ongoing debate about whether the U.S. stock market is overvalued or undervalued, based on traditional ways of valuing equities such as the price/earnings (P/E) ratio on forward estimated earnings. The historical range of the P/E ratio is 15 to 16, but we are not certain that is the best way to think about valuation multiples after such a protracted period of low interest rates. In our view, this classic measurement may not be as useful in the current environment, given that discounted cash flows in company models would be higher with low rates.

If the lower growth environment continues, we believe investors may seek companies that can generate higher revenues and translate them to higher earnings growth. That’s a stark contrast to what we have seen since the start of the financial crisis, in which companies increased earnings per share by drastically cutting costs or reducing their total shares outstanding through buybacks.

As we have stated in the past, we look for companies with solid balance sheets that generate strong free cash flows to repurchase shares or increase dividends and that offer a good or service for which they have pricing power, all leading to revenue growth. We think that may be the most relevant indicator for finding future opportunities.

In addition, we continue to assess the market’s willingness to pay for idiosyncratic risk. There have been periods in which equities tended to move together, particularly after a crisis of some type, with no distinction made between companies within sectors. However, today’s market is not tightly correlated, so we believe careful and active stock selection is a critical element of the process. In general, individual stock selection – not a target number of names or target sectors – drives our process and can be considered a function of how the market is pricing risk.

We have continued to reduce the cash allocation in the Fund, moving it toward what we consider a typical historical range of 10 to 20%. We think we have entered a phase in which investors have accepted an environment marked by lower growth, lower inflation and, at least for now, lower interest rates. In our view, that environment could persist longer than most investors would have expected at the start of the financial crisis. This is also a time when the Fund’s cash allocation could fluctuate within our historical range and reflect our outlook as well as ideas we think compensate us appropriately for the risks taken. Our general approach is to use price dislocations as times to invest in names that we think will do well in a low-growth global environment and periods of excessive optimism as opportunities to consider different investment choices.

Taking a look ahead

As part of managing investments in the Fund, we ask ourselves, “Where is global growth likely to come from in the future?” In our view, GDP growth in the Eurozone this year and perhaps in 2015 is likely to be only around 1% as that area continues grappling with very low inflation, repairing its banking system and implementing the European Central Bank’s version of quantitative easing. We think Japan’s growth also will be about 1% in 2014 and 2015, despite the monetary reforms enacted by the Bank of Japan.

We think real GDP growth globally will be at a slightly faster pace next year, with the U.S. providing much of the incremental change. Six years after the start of the global financial crisis, this is a welcome improvement considering increased U.S. consumer and business spending will in part be on goods and services produced around

the world.

Although we have seen a pause in consumer spending globally, including in emerging markets, we think the trend is likely to reverse at some point. That leads us to continue our focus on consumer-facing companies globally. While emerging-market countries have been growing faster than those in the developed world, we believe the Fund’s flexibility means this can present investment opportunities as companies that can benefit from this growth are domiciled across the globe. Our decisions thus are less about identifying specific geographic regions for investment and more about finding companies that not only serve a growing emerging market population with rising prosperity, but also a recovering U.S.

Past performance is not a guarantee of future results. The opinions expressed are those of the Fund’s portfolio managers and are not meant as investment advice or to predict or project the future performance of any investment product. The opinions are current through Sept. 19, 2014, and are subject to change due to market conditions or other factors.

Risk Factors. As with any mutual fund, the value of the Fund’s shares will change, and you could lose money on your investment. The Fund may allocate from 0 to 100% of its assets between stocks, bonds and short-term instruments of issuers around the globe, as well as investments in precious metals and investments with exposure to various foreign securities. International investing involves additional risks, including currency fluctuations, political or economic conditions affecting the foreign country, and differences in accounting standards and foreign regulations. These risks are magnified in emerging markets. Fixed-income securities are subject to interest-rate risk and, as such, the net asset value of the Fund may fall as interest rates rise. Investing in high-income securities may carry a greater risk of nonpayment of interest or principal than higher-rated bonds. The Fund may focus its investments in certain regions or industries, thereby increasing its potential vulnerability to market volatility. The Fund may seek to hedge market risk on various securities, increase exposure to various markets, manage exposure to various foreign currencies, precious metals and various markets, and seek to hedge certain event risks on positions held by the Fund. Such hedging involves additional risks, as the fluctuations in the values of the derivatives may not correlate perfectly with the overall securities markets or with the underlying asset from which the derivative’s value is derived. Investing in commodities is generally considered speculative because of the significant potential for investment loss due to cyclical economic conditions, sudden political events, and adverse international monetary policies. Markets for commodities are likely to be volatile and the Fund may pay more to store and accurately value its commodity holdings than it does with the Fund’s other holdings. These and other risks are more fully described in the Fund’s prospectus. Not all funds or fund classes may be offered at all broker/dealers.

Investors should consider the investment objectives, risks, charges and expenses of a fund carefully before investing. For a prospectus, or if available a summary prospectus, containing this and other information for the mutual funds offered by Ivy Funds, call your financial advisor or visit us online atwww.ivyfunds.com. Please read the prospectus or summary prospectus carefully before investing.

© Ivy Investment Management Company