“Imagination is a poor substitute for experience.”

Havelock Ellis

The accident

It was late in the evening of the 12th March. I was going to bed early as I had a big day ahead of me. Cycling is my sport and I had lined up a handful of Danish friends for a challenging few days in the mountains of Majorca, the beautiful Spanish island. We were all keen cyclists and wanted to take advantage of the early arrival of spring in Southern Europe to get some miles in the legs.

The next morning I took the first lead out of Esporles, a nice village on the edge of the Tramuntana - the mountain chain running along the Northwest coast of Majorca. We aimed for S’Esgleita with me in front – keen to show the other Danes that I hadn’t completely neglected my winter training despite the very wet winter in the UK. In S’Esgleita we took a right turn towards Santa Maria and Alaro, heading towards the serious mountains.

I had shown what I wanted to show and had dropped back to fourth position when the accident happened. The rider in front of me made a mistake and took a heavy fall. Riding on his wheel (in hindsight too closely!), I couldn’t escape the accident and went straight over him, hit the rocky ground myself and was knocked unconscious.

The rest is history. Too much time in hospital and a long recovery at home explains the absence of the Absolute Return Letter over the past seven months. The most difficult part has been to get the body functioning again, but I am (slowly) getting there, and I am excited to be back.

Enough about the accident. Now to what I much prefer to think and write about, but, before I do that, please allow me to thank all those of you who have sent me well wishes. Quite extraordinary and hugely appreciated!

Because of the long break, this letter is a little different from the typical Absolute Return Letter. Instead of picking on a particular subject, as I would normally do, this is more a summary of our views across asset classes. I hope you’ll find it interesting nevertheless. Next month I will return to the familiar format.

When I look at the world passing by outside my window, there is little doubt in my mind that the world is not as safe today as it was six months ago. For starters we have just had a very important referendum in Scotland. We now know the outcome but not yet the full implications. In about 3 years – unless Labour regains the control of the UK parliament – we will have an even more important referendum in the UK (more important economically if not emotionally) on the future relationship between the UK and the EU.

In the meantime, Putin and his cronies have played a very dangerous game in Ukraine. This is his third war, following armed conflicts with both Chechnya and Georgia, and the signs are that he is not going to walk away quietly. Even without Putin’s (outright) involvement, we have armed conflicts and new terror threats in many countries at present. Libya, Syria, Iraq, Sudan and Israel/Palestine to name a few.

In Europe, the economic recovery is limited to a handful of countries and the ECB has been forced to not only prolong but also intensify its de facto QE programme. The European powerhouse of yesteryear, Germany, looks surprisingly vulnerable and Italy is not in a good state either. The combination of almost zero inflation and high national debt, as in the case of Italy, is a bad one.

The ECB may have a serious job to do in Italy over the next 12-24 months if economic growth doesn’t pick up. Italy’s debt-to-GDP now stands at 145% and nobody knows when financial markets will decide that enough is enough. Before Italy is declared a complete write-off, though, one needs to remember that private savings in Italy are amongst the highest in the world.

Debt-wise, households and companies (but not countries) are widely believed to have improved since 2007. Following the severe near world-wide recession in 2008-09 the story doing the rounds was that both households and companies were now deleveraging, but the reality is not quite so simple. In many countries around the world total private debt has actually increased since 2007.

For all these reasons – and a few more – the world certainly looks less stable today than it did half a year ago. Why then, do equities keep going up and where are they likely to go from here?

Scotland

“In the end it came down to heart, not head” according to one commentator[1] the morning after the Scottish referendum. Totally wrong. The UK government ran a misguided No-campaign which was high on emotions throughout, and the Yes-campaign gathered rapid momentum as a result. Only when the economic argument was pushed to the front in the last few days, did the No-campaign begin to gather momentum.

I actually expected the No-campaign to win all along but by a smaller margin than they did. Now that the Union will continue, at least for the time being, David Cameron’s job is more secure than it looked like only a few weeks ago. His great advantage is that there is no strong challenger within the conservative party but, for now, that probably doesn’t matter.

Going forward, the British political system is likely to change as a result of the Scottish referendum. The political power within the UK is very concentrated in London and Cameron has already promised the regions more autonomy, similar to how the German bundesländer are run.

I have an inkling, though, that the Yes-side won’t give up this easily. With 45% of the votes, they know that independence is not that far away, and I suspect that something will happen in the next few years, whatever it is. Alex Salmond, the Yes-campaign’s leader, has already made a fool of himself by suggesting that Scotland should just declare independence unilaterally, but his comments suggest that the problem won’t go away.

I am not a great fan of how Europe is run, but we still need Europe to stick together going forward. UK Prime Minister David Cameron has promised the British people a vote on the EU by 2017, and whilst a modest majority of the English are in favour of exiting the EU, there is a solid majority in Scotland in favour of continued membership. Scotland’s No-vote is therefore a positive for continued UK EU membership.

Economically the EU vote will be far more important for the UK, and also for the rest of the EU, than the Scottish independence vote, and investors should pay serious attention. A British exit would strengthen the position of other north European anti-EU parties (which are gathering momentum already), and it is not entirely impossible that countries such as Sweden, Denmark, France and the Netherlands have their own vote at some point.

If the relatively rich North begins to exit, the EU as we know it today will effectively be over and financial markets will inevitably get more and more jittery. Having said that, amongst ordinary people, I suspect the apparent anti-EU psychology is as much a disillusion with politicians in general, as it is a sentiment against the EU itself. Hence politicians need to grow up and begin to treat people with dignity. In that respect, choosing Jean-Claude Juncker as the EU Commission’s new President was a massive mistake.

Japan-style deflation in our backyard?

It is no secret that we have been long-standing believers in deflation being a more probable outcome of the 2008-09 crisis than high inflation. What has changed over the past six months is that the world has begun to move in different directions. Whereas rising unit labour costs in the U.S. make outright deflation in that country quite unlikely, the same cannot be said of the Eurozone.

Chart 1: Japanese working age population and core CPI

Source: Barclays Equity Gilt Study 2014

Japan-style deflation across the Eurozone is no longer an outrageous thought. As you can see from chart 1, there is a close link between CPI and demographics. That has certainly been the case in Japan and I don’t see any reasons why it should be any different in Europe. The negative demographic trends are perhaps not as acute in Europe as they were in Japan in the early to mid 1990s, so one might expect a less dramatic outcome here, but the writing is on the wall.

Furthermore, Japan’s problems were multiplied due to an almost complete lack of political recognition and willingness to take drastic action. At least, with Mario Draghi in charge of the ECB, there seems to be a willingness to do something.

The obvious implication of this, if true, is that European equities are not as cheap as many suggest they are. Chart 2 looks at equity performance in different inflation environments and it is obvious that there is a sweet spot when inflation is positive but modest. The chart is based on U.S. data but there is no reason to believe it is any different in Europe. When inflation is too high, or alternatively too low, equities tend to deliver relatively poor returns which is at the extreme right and extreme left of chart 2. Deflation is obviously not a given yet but worth keeping an eye on.

Chart 2: Average U.S. equity performance across inflation deciles

Source: Barclays Equity Gilt Study 2014

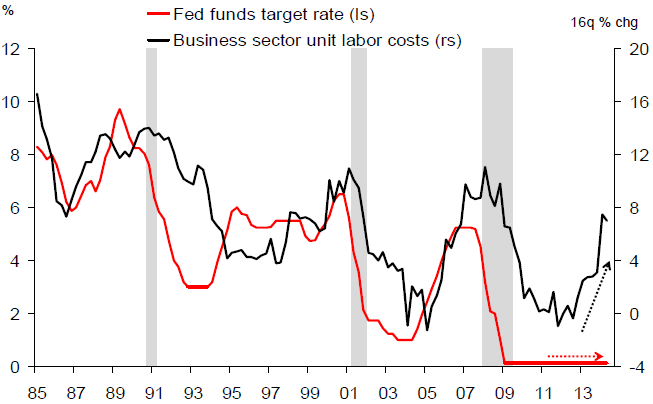

Is the Fed falling behind the curve?

As mentioned earlier, the picture in the U.S. – and to a degree also in the UK - is quite different. The Fed increasingly looks like it is behind the curve with the Fed Funds rate remaining unchanged despite a significant rise in unit labour costs (chart 3). Not only does that suggest a meaningful rise in the U.S. policy rate over the next couple of years – and therefore also possibly a further rise in longer term rates - but it also suggests a relatively strong U.S. dollar.

Forward rates on the Fed Funds rate suggest it will reach 1.50% by June of next year; however, if the latest estimates for unit labour costs are painting a true picture of inflation in the pipeline, one could argue that the Fed Funds rate could go substantially higher.

The situation in Euroland is still dire

The ECB has done a superb job convincing (most) investors that the situation in Europe is actually on the mend and, as mentioned earlier, private balance sheets - both corporate and households’ - have been mentioned more than once as one of the areas of improvement. The reality, however, is somewhat different.

Debt-to-equity in the non-financial corporate sector has clearly deteriorated across the board (chart 4a) which in the not so distant future will have negative implications for both take-over activity and share buy-back activity and hence also should impact overall equity performance. The only question is when.

Chart 3: U.S. unit labour costs vs. Fed funds rate

Source: Deutsche Bank Global Markets Research

Debt-to disposable income in households (chart 4b) has improved in some countries whilst the ratio has deteriorated in others. On balance, though, household debt has not changed dramatically.

Chart 4a: Debt-to-equity ratio of non-financial corporations (%)

Chart 4b: Debt-to-disposable income in households in selected countries (%)

Source: Deutsche Bank Global Markets Research

On this basis it is hard to argue that the debt situation has improved pretty much across the board as some do. Due to low interest rates, the cost of servicing the debt may have fallen, but it is a ticking time bomb. Policy makers obviously know this and are likely to keep rates lower than what can strictly speaking be justified from an inflation point of view, in order to keep the economic recovery on track (falling behind the curve, as economists call it). This is precisely why we have predicted for a while that the main adjustment factor between the stronger economies and the more problematic ones may not be interest rates in this particular cycle, as is usually the case, but currencies. We continue to expect currencies to move more than interest rates, relatively speaking.

Should we polka with Putin?

Politically, the world is a fair bit messier than it was six months ago. In recent months Putin hasn’t exactly endeared himself to the West with his antics, and neither have some Muslims in certain countries with particularly radical views. As far as Russia is concerned, we in the West have to decide whether we are interested in doing business with Russia or whether we care more about political principles. We have an equally difficult moral dilemma in relation to certain Middle Eastern countries. In both crises the political leadership of the West has not exactly covered itself in glory so far.

Having said that, I keep reminding myself that political crises rarely have a long-standing effect on financial markets, so I wouldn’t expect a political crisis like the one in Ukraine to trigger the next bear market, unless it turns particularly ugly. Other events, such as rising interest rates or similar economic incidents, are far more likely to take the steam out of the equity rally when it eventually happens (a political crisis can obviously lead to rising interest rates, so the two cannot be seen as completely separable).

Which equity markets offer most potential?

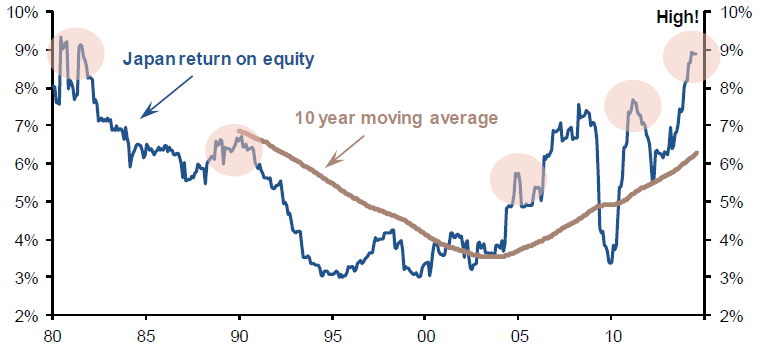

One area I have not elaborated on yet is Japan. There are strong indications that Japan has finally turned the corner economically. At the same time, return on equity has returned to pre-crisis levels in Japan (chart 5), but valuations have not.

Chart 5: Japanese return on equity is back to an all-time high

Source: Societe Generale Cross Asset Research

With a more or less fully priced U.S. equity market and a Federal Reserve Bank at risk of falling seriously behind the curve, and a Europe where it is hard to see where growth is going to come from (ex. U.K.), Japan looks remarkably interesting, and I expect it to be one of the better performing mature equity markets over the next few years. Just don’t forget to hedge your currency risk. I am not saying that the Yen will fall, but there is enough uncertainty surrounding the Yen that I would rather not have to worry about that aspect.

Another observation I would like to make relates to the Eurozone. As already mentioned, there is a not insignificant risk that the whole €-area falls into deflation. On the other hand, there are also early signs that Europe is coming back to life. Activity is picking up in both Greece and Spain, and overall credit growth in the Eurozone has begun to recover, even if it is still negative (chart 6). At this juncture, Europe could turn out to be a phenomenal recovery story or it could prove a multi-year failure. In my book, I still think the latter is (marginally) more likely than the former, but nothing can be excluded at this juncture.

Chart 6: Credit growth to private sector in euro area (% year-on-year)

Source: Deutsche Bank Global Markets Research

A recovery in Europe will also be helped by the strong U.S. dollar that I am predicting. Given the necessity for the U.S. Fed to tighten sooner rather than later, it is hard to see how the U.S. dollar will not substantially outperform the euro over the next couple of years.

EM equities could potentially face a more difficult time if I turn out to be right about the U.S. dollar. If one rewinds quickly to the 2008-09 bear market, it is pretty obvious that the strong dollar at the time did a lot of damage to EM equities. The U.S. dollar is often a significant risk in emerging countries because a lot of borrowing takes place in U.S. dollars. It is obviously too early to paint an overly negative picture, but a powerful rally in the U.S. dollar which is a distinct possibility, will not be good news for EM equities.

Famous last words from Bill Gross?[2]

In his latest letter to investors (“For Wonks Only” – see here), Bill Gross makes a very important point. In a credit-based economy (as opposed to cash), credit growth is a necessary (but not sufficient) condition for economic growth.

In the long run, as Bill Gross states: “...economic growth depends on investment and a rejuvenation of capitalistic animal spirits – a condition which currently does not exist. [...] The U.S. and global economy ultimately cannot be safely delevered with artificially low interest rates, unless they lead to higher levels of productive investment.”

The implication is obvious. We are in an era of low credit expansion. In the U.S. credit has expanded at an annual rate of 2% over the past 5 years and 3.5% over the most recent 12 months; in Europe credit growth is negative. One should continue to expect below-par economic growth and, as a result, lower than average EPS growth and relatively low interest rates over the next few years.

This is precisely why the Fed and other central banks will most likely continue to be behind the curve. They fully understand that credit growth is an absolute necessity in today’s environment and that rising inflation, as long as it doesn’t run amok, is not necessarily a bad thing.

Commodities in a bear market?

Commodities also deserve a mention. As can be seen from chart 7, commodity prices are in a multi-year slump. Based on the broad Bloomberg commodity index, commodity prices recently hit a five year low. The fall is quite broad and covers areas as diverse as iron ore and crude oil. This is obviously not precisely what those countries leaning towards deflation need right now, but it is nevertheless an important fact.

Chart 7: Overall commodity prices in recent years

Source: Daily Telegraph

In order to understand exactly what is going on, one needs to distinguish between those countries dominated by consumers (e.g. U.S., U.K.) and those countries where investment spending accounts for a bigger share of GDP (e.g. Germany, China). The global consumer is clearly getting more and more confident and, as a result, has started to spend more, which explains the relatively robust growth in GDP in some countries while it lags in others.

Obviously, the two cannot diverge forever. However, to suggest that global GDP is collapsing and that falling commodity prices are a sign thereof, as some do[3], is simply not true. If anything, economic momentum is gathering strength in some of the largest economies in the World (e.g. U.S., Japan, U.K., Spain). Falling commodity prices are more likely a result of banks in many countries exiting commodity trading, but that is not nearly as good a story.

In the context of all of the above, gold is not likely to be a superior performer any time soon. We live in an age where global GDP growth, and inflation, are both likely to remain relatively subdued, which do not provide the best conditions for a gold rally. If you believe the ultra pessimists and their prediction that the global economy is about to tank again, you might want to buy some insurance (gold), but I don’t share that view.

Conclusion

To sum it all up, I believe the major equity bull market of 2013, and also the somewhat weaker equity bull market of 2014, have been driven primarily by QE. One could even go as far as to suggest that without QE in the U.S. and the U.K., and without de facto QE in the Eurozone, equity markets would not look nearly as robust as they do today.

Meanwhile, interest rates have been driven down to levels that make most, if not all, fixed interest investments a relatively unattractive proposition. It is therefore quite reasonable to expect modest returns on traditional asset classes over the next few years – in the case of bonds, possibly even negative returns.

Investors (well, most investors) have not yet caught on to this and continue to pile in to equities, as if they are the solution to their return challenge (see chart 8). Pension funds are one example of such investors. If such pension funds have fixed obligations (called defined benefit plans in the UK), they currently struggle to generate the level of returns they need to meet their obligations.

Even if there are good reasons to believe that the prolonged rally can continue for a little longer, there are equally good reasons to believe that the current equity bull market may end in tears. Such is the disconnect between stock valuations and economic fundamentals in some markets.

Chart 8: Share of assets in equity funds and bond funds (%)

Source: Deutsche Bank Global Markets Research

Having said that, I am not predicting a repeat of 2008-09. Too many commentators engage in this kind of activity which, quite frankly, is daft, considering how rarely it happens. Statistically, equity markets fall 40-50% (as they did in 2008-09) only a couple of times in a life time, so why somebody is forecasting the next bloodbath to be around the corner is quite frankly beyond me.

A much more modest decline, but still a decline, is a likely outcome at some point over the next 12-18 months. From an investment perspective, one is further challenged by the fact that what looks most interesting from a currency point of view (the U.S. dollar), looks most overvalued and hence least attractive from an equity point of view, so one needs to be careful and hedge/invest accordingly.

Also, if one depends on a certain level of income, as many pension funds do, we recommend that one takes a serious look at what we call alternative income strategies. And in a world where there is an apparent disconnect between valuations and economic fundamentals, it is important to focus on investment strategies that are blessed with what we call ‘true economic value’ as they are least likely to be blown out of the water, just in case mayhem returns.

Niels C. Jensen

2 October 2014

©Absolute Return Partners LLP 2014. Registered in England No. OC303480. Authorised and Regulated by the Financial Conduct Authority. Registered Office: 16 Water Lane, Richmond, Surrey, TW9 1TJ, UK.

Important Notice

This material has been prepared by Absolute Return Partners LLP (ARP). ARP is authorised and regulated by the Financial Conduct Authority in the United Kingdom. It is provided for information purposes, is intended for your use only and does not constitute an invitation or offer to subscribe for or purchase any of the products or services mentioned. The information provided is not intended to provide a sufficient basis on which to make an investment decision. Information and opinions presented in this material have been obtained or derived from sources believed by ARP to be reliable, but ARP makes no representation as to their accuracy or completeness. ARP accepts no liability for any loss arising from the use of this material. The results referred to in this document are not a guide to the future performance of ARP. The value of investments can go down as well as up and the implementation of the approach described does not guarantee positive performance. Any reference to potential asset allocation and potential returns do not represent and should not be interpreted as projections.

Absolute Return Partners

Absolute Return Partners LLP is a London based client-driven, alternative investment boutique. We provide independent asset management and investment advisory services globally to institutional investors.

We are a company with a simple mission – delivering superior risk-adjusted returns to our clients. We believe that we can achieve this through a disciplined risk management approach and an investment process based on our open architecture platform.

Our focus is strictly on absolute returns. We use a diversified range of both traditional and alternative asset classes when creating portfolios for our clients.

We have eliminated all conflicts of interest with our transparent business model and we offer flexible solutions, tailored to match specific needs.

We are authorised and regulated by the Financial Conduct Authority in the UK.

Absolute Return Letter contributors:

|

Niels C. Jensen |

Tel +44 20 8939 2901 |

|

|

Gerard Ifill-Williams |

Tel +44 20 8939 2902 |

|

|

Nick Rees |

Tel +44 20 8939 2903 |

|

|

Tricia Ward |

Tel +44 20 8939 2906 |

[1] http://www.cityam.com/1411120245/after-scottish-referendum-results-its-what-happens-next-which-could-buffet-david-cameron.

[2] Since I wrote this, Bill Gross has resigned from PIMCO.