"Complacency is a state of mind that exists only in retrospective; it has to be shattered before being ascertained.” - Vladimir Nabokov

Key Takeaways:

Lulled into complacency by unprecedented central bank accommodation, investors have driven prices across multiple asset classes to record levels. The foray into risky assets has occurred despite widespread global economic weakness following the Great Recession. Further efforts to restructure debt-heavy private sector balance sheets, fiscal consolidation aimed at gaping budget deficits, and restrained credit availability due to more onerous regulation will continue to act as economic headwinds.

- We look for inflation expectations to remain well anchored with average price increases falling short of the 2% official targets by the Fed, the ECB and the BoJ in the face of tepid economic growth, high unemployment and excess global productive capacity.

- Backdropped by weak growth and low inflation, we project relatively low rates of return on all asset classes over the next five years. Equities, especially US equities which had an explosive rise in 2013, appear most vulnerable as the economy fails to achieve escape velocity. In contrast, we overweigh exposure to EM equities as the composition of global output continues to shift towards these economies. Other attractive features of EM markets include favorable demographics, rising standards of living, rapidly expanding middle-class wealth, and maturing financial markets.

- We also overweigh exposure to high-quality dollar and non-dollar bonds. With political risks continuing high, US Treasuries will continue to attract substantial “safe haven” flows, ensuring that the 10-year yield stays in a narrow 2.5% - 3.5% trading range. Also deserving outweight are sovereign and corporate bonds in EMs with strong fiscal positions and current account surpluses.

Complacency is a dangerous mindset, especially for investors. Having been generously rewarded beyond their expectations, investors were coddled in the arms of complacency as 2013 drew to a close. The Dow Jones Index was flirting with the 2007 record peak. Junk bond yields had fallen to record lows, compressing spreads to within a shouting distance from risk-free Treasuries. Securitization was coming back from the dead, while M&A activity was starting to boom.

Investor complacency was not confined to the US. In Japan, despite a setback in 2H2013, the Nikkei 225 Index had climbed to a four-year high spurred by new government stimulus aimed to shake the economy out of its prolonged lethargy. And in a rare show of support, the advance seemed to have reawakened the enthusiasm of domestic retail investors, who for the previous twenty years had come to expect that stock prices only go down.

In Europe, with the sovereign debt and the bank crises in remission thanks to unprecedented support by the European Central Bank, the S&P European 100 Index climbed a “wall of worry” and stood at a stone’s throw away from the 2007 record peak. Meanwhile, against long odds, the euro had regained a hard currency luster.

Similarly, prices of emerging market debt denominated both in hard and local currency were at near record highs, shrinking the yield spread over US Treasuries to near record lows as investors seemed eager to substitute interest rate risk for credit risk.

And The Beat Goes On

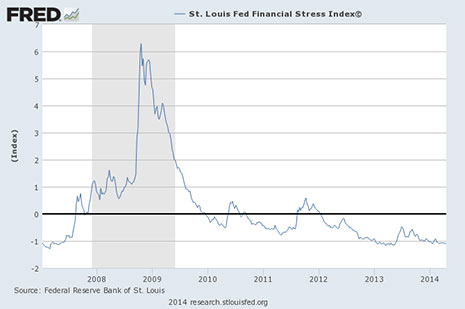

Shrugging off a few engine knocks – negative 1Q US GDP growth, Fed taper, sagging housing, anemic capex, at times choppy equity markets, and ominous geopolitical tensions abroad – the sense of complacency carried through the first half of 2014. The CBOE Volatility Index (VIX), a measure of risk and fear, continued to trend lower (Exhibit 1), while the St. Louis Fed’s Financial Stress Index, which gauges financial market tensions, was been plumbing new depths (Exhibit 2). Other symptoms of complacency included a near record level of margin debt and extremely positive readings by various investor sentiment surveys like the well-regarded Ned Davis Crowd Sentiment Poll.

A consistently dire drumbeat by high-profile perma bears of an imminent collapse was unable to dent investors’ enthusiasm for stocks. Meanwhile, surprisingly and to the astonishment of most pundits, bond yields, instead of starting the long-waited upward march, moved lower.

Exhibit 1

Exhibit 2

Nourishing this “devil-may-care” attitude has been the elixir of the Fed’s zero-interest-rate-policy (ZIRP), and the promise to hold short rates near zero for a prolonged period, most likely until mid-2015 or longer depending on the economy’s state of health. And with abundant central bank liquidity, all boats floated higher (if they were in the water).

Investors also seemed to be emboldened by the widely anticipated rebound in business activity following the 1Q14 setback, continuing strength in corporate earnings amazingly so late in the business cycle, and a steeply upward sloping yield curve, which is conducive to pushing out risk boundaries. The confluence of these forces had pushed the MSCI US Index 6.8% higher and to a new peak by June 30th.

A sense of complacency also continued to play abroad. The MSCI Europe Index in USD terms was up a strong 5.5% through June 30th (ironically paced by stocks in troubled economies like Italy and Spain which were up 14.5% and 12.3%, respectively), as global asset allocators continued to tilt portfolios away from the US, which was perceived to be expensive.

In comparison, the MSCI Far East Index was up a meagre 1.4% in 1H2014, dragged down by Japan. Japanese equities, heavily dependent on “the kindness” of foreigners, were essentially flat rising 0.7%, as investors stood by for more evidence that Abenomics is gaining traction. Some unwinding of the enormous long positions by hedge funds put on last year played a role in the Nikkei’s lackluster performance durng this time.

Similarly, emerging market equities, following last year’s significant setback inspired by growing fears of Fed tapering and rising interest rates, regained their footing, climbing 6.2% in 1H2014 as measured by the MSCI EM Index. Among the regions, SE Asia took the gold rising 9.5%, while Latin America took the silver with a 7.2% advance. Emerging Europe, still caught in the backwash of the sovereign debt crisis failed to stay in the race turning in only a 0.3% rise during this period. Similarly, China continued to disappoint, falling about 1%, as a result of the economic slowdown engineered by the government’s efforts to tame excessive credit growth and deflate what was perceived to be a housing bubble.

Complacency also spilled over into the bond markets in 1H2014. The surprising drop in US long-term Treasury yields most likely reflects reassessment of growth prospects ahead (both the IMF and the OECD had trimmed global growth prospects in their mid-year updates), as well as a run to safety in the face of rising geopolitical tensions. Remarkably, extensive underlying economic weakness and low credit ratings have not detered bond investors thirsty for yield from snapping up sovereign paper of the eurozone’s periphery, driving 10-year yields down to pre-crisis levels, and in some instances, i.e. Italy and Spain matching the default-free US Treasuries. The ECB’s aggressive policies and its mantra that it will do “whatever it takes” to keep the euro intact also figured in the mix.

Rifts in The Lute

The melody of complacency started to miss a few notes with the start of the second half. In the US, equity markets have been choppy, ebbing and flowing since the end of June, as investors tried to navigate the cross-currents of economic and geopolitical events. Following a steep fall in July, stocks regained their footing in August, steadied by indications that the Fed will not veer off its low interest rate course until sometime in 2015 and only if economic conditions warrant. Despite a meekly 1.3% average gain for the two months, the MSCI US Index had posted a respectable 9.5% gain through the end of August.

By comparison, equity markets came under severe pressure in Europe, hit by the double whammy of deteriorating economic conditions and the rising tensions of the Russian-Ukrainian conflict. Having fallen 3.8% in July, the MSCI Europe Index managed only a 0.4% rebound in August. The resulting 1.9% YTD advance in the Europe Index through August pales against the 9.5% YTD gain in US equities during this period.

Equity markets in the Far East have faired only marginally better, holding essentially flat overall during this two-moth period undermined by weakness in Japan, the dominant player in this lot. The Japanese market had a tiny 0.5% gain in July, but gave all that back and more in August with a negative 2.2% return, and a YTD return of minus 0.9%. Smaller developed markets in the region, like Australia, Singapore and New Zealand, have managed to hold on to positive returns so far in 2H2014.

This lackluster performance by non-US equities also raises questions about prevailing wisdom among investment strategists who have been advocating tilting portfolios away from the US. There is a reason why Europe and Japan appear relatively cheap, and they might even get cheaper as the year unfolds and economic conditions fail to live up to expectations. Ironically, using net flows into mutual funds as a yardstick, there has been a net outflow of $16.4BN through August this year from US equities, compared with $70BN inflow into international equity funds.

In contrast, bucking the developed market weakness, emerging markets have posted gains so far in the second half. The MSCI Emergng Markets Index is up 2.2% as of the end of August, bringing the YTD return to 10.6%. Is this a reflection of regained investor optimism about EM prospects, or the result of trading off central bank, mostly the Fed’s, ZIRP policies and liquidity largesse? Our best guess is the latter.

In the US, other indicators suggesting a slippery road ahead for equities include weakness in small cap stocks, the rotation away from cyclicals and industrials and into defensive sectors such as utilities and consumer staples, and large caps with strong balance sheets, the selloff in high yield bonds, and widening spreads against Treasuries. And with profits and profit margins at peak and the US dollar strengthening, any weakness as a result of sluggish economic conditions and anemic top-line revenue growth would translate quickly into a setback for equities.

The Real Valuation Please Stand Up

Market valuation is another bone of contention hotly picked over. Those who feel the market has long legs base their agrument on the extraordinary ability of companies to generate earnings and maintain profit margins. And without any apparent potholes on the road ahead, corporate profitability might continue to surprise on the upside, helping markets to grind higher. In comparison, advocates of an imminent pullback point to several gauges, such as the Shiller CAPE, corporate equities to GDP, the Tobin Q, and corporate equities to net worth, all of which are flashing “over-valuation” signals.

Deciding on the market’s life expectancy based on valuation measures is almost like calling the weather: Is it mostly sunny or partly cloudy? Only the weatherman thinks he knows the difference. Recognizing that this market is equally hated by bulls and bears suggests that valuation is an imperfect yardstick to judge the future. Our friends at Princeton Capital Management offer the most appropriate way to look at market valuation. In their latest Market Commentary, they write, “The American stock market includes such a broad variety; there is nearly always the overvalued, the reasonably valued, the attractively valued, and the overlooked undervalued.” To which we would add that valuation yardsticks based on historical performance are a poor compass of forecasting future direction. Among other things, the profile of the indexes is different over different market cycles, and rarely, if ever, two business cycles are alike. And as our officemate, Craig Drill of Craig Drill Capital, has often said, “Valuation tends not to be an important variable during a bull market…only when it ends”.

Through a Glass Darkly

Mindfull that in recent years surprises have tended to overwhelm predictions, we have chosen not to speculate as to how much longer markets would continue to dance to the siren song of complacency. To be sure, bull markets in stocks, like business cycles, do not die of old age; they typically fall victim to policy errors and exogenous influences that undermine investor and business confidence.

Presently, growing corporate earnings, an upward sloping yield curve, well-anchored inflation expectations, strong M&A activity and rising dividends are all supportive of further gains in stock prices. Yet, pundits, are still trying to time the market and they continue to ask what time it is. But as our late officemate Jerry Goodman, a.k.a. Adam Smith, wrote, “the clocks have no hands.” Instead, we prefer to highlight certain aspects of the investment landscape that are likely to shake investor complacency and influence asset prices over the next few years.

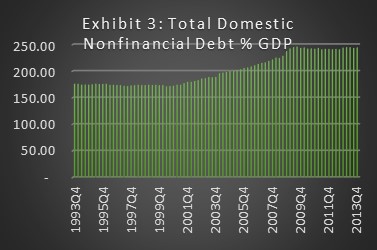

Lethargic growth in the developed world in the aftermath of of the Great Recession appears endemic and well entrenched. In the US, the economy continues to heal, but there are no obvious drivers to promote faster growth. Most importantly, the country still carries a heavy load of debt that acts as a dead weight on growth (Exhibit 3).

Source: FRB, Flow of Funds

Source: FRB, Flow of Funds

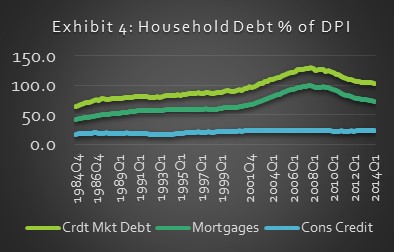

More specifically, in the aftermath of the Great Recession, US households have made significant progress in deleveraging their liabilities. Yet, from a historical perspective, total debt levels at over 100% are still high relative to income (Exhibit 4). Despite this progress, the restructuring of household assets and liabilities is a long-term process and deleveraging has further to go. Absent a strong recovery in employment and income, this process will continue to be a brake on consumption.

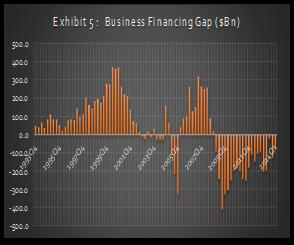

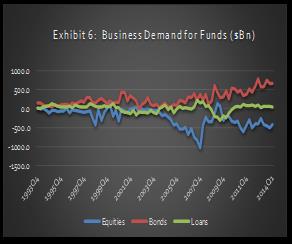

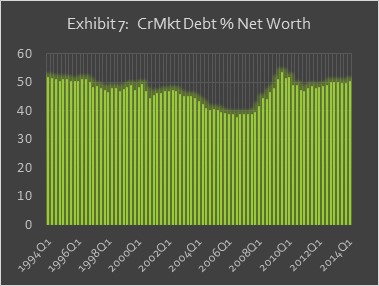

The restructuring of business balance sheets, meanwhile, is more cosmetic than substantive. Taking advantage of cheap credit, nofinancial corporations, top-rated and lower-quality alike, have issued a massive amount of debt. But facing a global slowdown in demand, instead of boosting capex, companies have used the proceeds to refinance more expensive debt, buy back equities, increase dividends, and aggressively pursue mergers and acquisitions. With a hefty cushion of free cash (Exhibit 5), there has been limited appetite bank financing (Exhibit 6). As a result of these activities, the leverage of business balance sheets, as measured by the ratio of debt to net worth, now stands above pre-crisis levels (Exhibit 7).

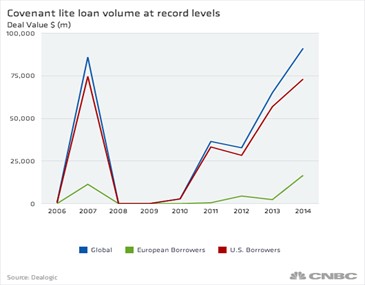

The composition of corporate debt that is a matter of considerable concern. Responding to investor hunger for yield, there has been a surge in issuance of low-rated paper and leveraged loans with diluted covenants (Exhibit 8). Also, mutual funds and ETFs, often nervous investors, hold a significant amount of these instruments. In the event of a sentiment turn due to a change in monetary policy or inflation expectations, a rush for the exits by these investors could clog the credit pipelines, causing dislocations in the real economy.

Although the state of the balance sheet is a significant driver of business investment, other factors also play a role as well. For instance, there is a growing chorus clamoring for a renaissance in US manufacturing. Unquestionably, cheaper energy and feedstock, and the ability of companies to substitute capital for labor have greatly increased the competitiveness of US manafacturing. Also, the rising cost of offshore supply lines, coupled with concerns about quality control, have caused some onshoring of manufacturing. The primary reason, however, that US companies have migrated overseas remains: High growth rates, especially in emerging markets. Rapidly expanding middle classes, rising incomes and standards of living, and rapidly expanding middle classes offer irrisistable opportunities; “overlook these and risk falling behind” is a battle cry echoed in every US boardroom.

Nor are conditions overseas supportive of a spurt in capex. Having wiped out a generation of consumers in the aftermath of the financial crisis, lofty unemployment and weak bank credit and trade flows, Europe is well along the way of a “Lost Decade.” In Japan, Prime Minister Abe’s three-arrow policies – expansionary fiscal and monetary policies, coupled with structural reforms – have yet to hit their target to revive the economy. Instead of boosting domestic capex, Japanese companies have continued to expand their operations overseas, where, just like their American counterparts, they perceive greater growth opportunities. Meanwhile, China, a major driver of global growth in the previous business cycle, has lost a great deal of economic momentum as the government tries to contain excessive credit expansion. Huge overcapacity in many sectors, weak export demand and falling profit margins are likely to stifle capex expansion.

Plentiful Liquidity, but Limited Credit

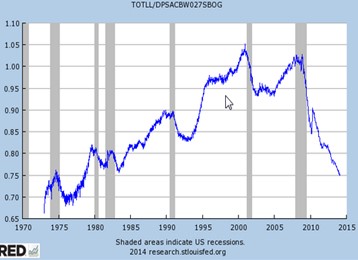

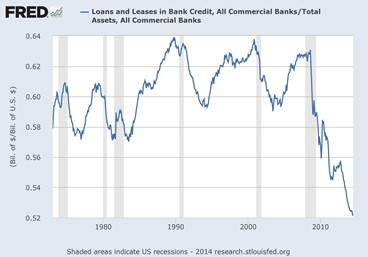

Looking at the big picture, we find that the primary cause of the global malaise is restrained credit growth, especially bank credit. In the US, a noticeable pickup in bank and finance company lending, albeit in large part the result of looser credit standards, has been supporting auto sales and credit card purchases. Yet, the revival of mortgage lending, which is by far the most important item in consumer spending, is lagging seriously. The reluctance by banks to open up the credit spigot is strikingly obvious in the loan-to-deposit ratio which is at a 35 year low (Exhibit 9), and the ratio of loans-to-total-assets which at 52% is the lowest on record (Exhibit 10). A more onerous regulatory environment also figures in the mix.

Exhibit 9

Exhibit 10

Lending by European banks is even more constrained by impaired collateral and higher capital requirements. This is significant in that they are the main credit pipeline for world trade, especially Asian trade flows. Meanwhile, bank lending in Japan is missing in action. After selling a hefty amount of government bonds (JGBs) to BoJ, they are sitting on a fat cushion of liquidity, but unable to put it to work spurned by companies which are themselves top-heavy with liquidity.

Therein lies the challenge for central banks. Having pumped massive amounts of liquidity to stabilize the banking sector, the recipients of their largesse are unwilling or unable to find profitable lending outlets. As our officemate, Al Wojnilower, has often pointed out, total credit to nonfinancial entities has to grow at about the same rate as nominal GDP, or about 4-5%, to get the economy on a sustainable long-term growth path. Absent this response, the consternation of pundits over an expected increase in the official fed funds rate is amusing. Would raising the fed funds by a couple of percentage points, if that much, be such a disastrous event likely to derail the economic expansion? Lest we forget, except in rare circumstances, it is always the availability or lack thereof and not the price of credit that cripples economic activity as the Great Recession made perfectly clear.

Besides growth prospects, three other macro factors that influence asset prices are inflation, interest rates and currencies. Regarding prospects for inflation, our central-case continues to call for disinflation, or even a mild case of deflation in the foreseeable future. It will take time for production gaps to close in the face of anemic global output growth thereby keeping labor costs and raw material prices under control. Strong pronouncements by central banks wishing to boost prices are fall backs to earlier times when globalization was in its infancy and production was largely driven by domestic demand. And what’s so magic about 2% being a sustainable inflation level? Even if achieved, trying to control it is like saying that a woman will remain constantly two months pregnant.

Furthermore, the view promoted by some economists that monetary expansion begets inflation is false as the experience in Europe and Japan clearly attests. Similar outcries by prominent experts in the US, including some members of the Federal Reserve, are driven more by political dogma and anachronistic thinking than by appreciation of facts underscoring that inflation is not primarily a monetary phenomenon. Except during periods of war and the outlier bout in the 1970s (brought on by misguided government policies and structural impediments to production), the US never had an inflation bias. But it regularly confronted high unemployment which led to the passing of the Employment Security Act of 1947, and continues to confront policy makers today six years after the Great Recession. And lest we forget, government debt is deflationary to the extent it finds its way into private sector portfolios rather than spent on consumption. In the face of tepid global growth and subdued inflation expectations, we consider the case for rising interest rates to be moot. In the US, long yields are likely to remain range-bound between 2.50% and 3.25% on 10-year Treasuries, held down by the gravitational forces of record low yields in Europe and Japan, and the continuing appetite for “safe haven” US paper by foreign investors.

A perceived divergence of central bank policies – less accommodative Fed contrasted with more aggressive easing by ECB and BoJ – coupled with wider yield spreads in favor of long Treasuries against equivalents in Europe and Japan, has weakened a basket of currencies against the dollar. Most notable are the declines in the euro and the yen in the wake of investor loss of enthusiasm over economic prospects in Europe and Japan. But, it is premature to start speculating of a significant rise in US bond yields at this stage of the cycle. Interest rate guidance notwithstanding, the Fed has limited influence over domestic bond yields, which are largely driven by international factors, including geopolitical events, beyond its control. From a portfolio perspective, hedging currency swings besides being expensive, they also tend to be a wash over a full market cycle. Going forward, although the dollar is likely to maintain its alpha currency status, we do not expect the weakness of other major currencies to persist as the widely anticipated rise in US bond yields on the back of stronger activity gives way to a more somber assessment of US prospects.

Geopolitics: Known Unknowns

Geopolitics, always a hot topic of discussion, seems to be just fodder for the media. There is no way of predicting when political tensions will assert themselves, or how they might play out. At times, they might inspire market volatility, but as serious crises in Ukraine, the Middle East and Africa demonstrate, they have yet to undermine investor complacency, the increased appetite for US Treasuries notwithstanding. But, a more disquieting development with potentially serious investment consequences over the longer time horizon is the perceived identity crisis of US foreign policy. On the trade front, the Trans Pacific Pact (TPP), a core strategy underlying the Obama Administration’s Asia pivot designed to counter growing Chinese influence has yet to gain traction, a fate also shared by negotiations to strengthen trade ties with the European Union. Similarly, with the US foreign policy playing defense, geopolitical tensions have flared up, threatening to rearrange world order. It is unlikely that a clearer global geopolitical picture will emerge until after the 2016 national elections.

Asset Allocation: Rising Lower Expectations

Combining global macroeconomic and geopolitics developments into a coherent asset allocation matrix, usually a challenge under the best of circumstances, becomes more difficult in a regime of unorthodox central bank policies breeding complacency, e.g., central bank “put”, and encouraging investors to push out the boundaries of risk. This is especially true when trying to divine events over a longer time frame. There are high-powered econometric models designed to make precise predictions several years out, but, as the 2008 financial crisis and its aftermath clearly underscore, their prognostications are often wide of the mark in magnitude and direction.

Relying on past experience, models simply cannot adapt quickly to structural changes, or policy responses to unfolding events. Models are particularly inept in replicating financial market behavior, which is often driven by irrational exuberance or paralyzing fear. This is especially true in today’s environment replete with geopolitical risks, weird correlations among asset classes and a business cycle seemingly unresponsive to unprecedented fiscal and monetary policies.

Mindful that hands-on experience of how the global economy work always trumps high-power models brings to mind a discussion over lunch nearly 30 years ago with an old friend, who was the head of a major Greek shipping company based in New York City. Having traveled around the world many times over, he had captivating stories to tell about people, places and events. When we asked him where we would find the most promising investment opportunities 20 or 30 years down the road, his vision turned out to be remarkably prescient. He said, “Go east my young friend; Asia is the place where the action will be.” And what about Europe, we queried? “By then, Europe will have become a museum,” he replied. We pressed on, “And what’s in store for America 30 years on?” Without missing a beat, the voice of experience replied, “By then, America will be contemplating its navel.”

While we often reflect on our old friend’s wisdom as we try to navigate the challenging global investment landscape, we also take into account the extensive changes that have reshaped the world economy during all these years. In this regard, there are a few known unknowns worth keeping in mind when trying to determine longer-term global asset allocations.

- Neither economists nor policy-makers have been able to suspend the business cycle; there will always be short-duration cycles within longer-term cycles. The challenge will always be to separate fact from noise, and to distinguish trend from fad.

- Powerful structural changes are transforming the global economy in ways that have yet to be accounted for by econometric models. Included in these developments are: the rise of China and other emerging economies with globally competitive companies (“Alibaba, Samsung, Embraer, Ranbaxy, anyone?”); shifting demographics (most countries in the Western world have stopped breeding in step with rising standards of living - it has been said that the world’s most effective birth control device is money); and the wholesale restructuring of traditional business models in manufacturing in the face of globalization.

- The development of a complex, tightly interwoven and truly boundaryless financial system which is beyond the control of any given jurisdiction, and where contagion and powerful knock-on effects can be transmitted instantaneously around the world.

- Changing geopolitical dynamics in the face of new economic alliances, shifting trade patterns, immigration flows and the rise of Islamic fundamentalism give rise to increased level of geopolitical risk and hard to predict “fat tail” risks and “black swans”.

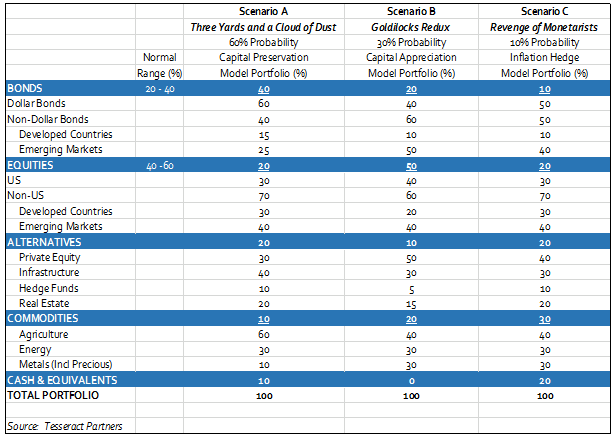

In constructing global portfolios, instead of relying on single point estimates of return on various asset classes, we use scenario analysis ascribing probability weights to key return drivers and how they might influence different outcomes. The three most probable scenarios likely to play out over the next few years with the corresponding portfolios are shown in Tables A, B and C.

Scenario A: “Three Yards and a Cloud of Dust” (60% probability). A favorite offense tactic of Woody Hayes, the famous Ohio State coach (instead of having his players throw long passes and gain many yards at a time, he preferred to have them keep the ball close to the ground and move it in small increments) best describes the most likely environment ahead. A grinding world economy gains traction incrementally in the face of continuing deleveraging, sluggish world trade, constrained credit growth and bouts of disinflation generates only modest overall investment returns.

Scenario B: “Goldilocks Redux” (30% probability). Years of aggressive central bank policies, coupled with lessened fiscal austerity, help to boost global growth to trend, while productivity improvements on the back of strong capex spending keeps inflation under control. Stocks outperform bonds and alternative investments.

Scenario C: “Revenge of the Monetarists” (10% probability). Like a spontaneous combustion, excessive global liquidity translates into rapid economic growth across a wide swath of developed and developing countries as money velocity rebounds, but causes inflation to rise sharply as final demand outpaces supply, forcing central bank tightening, and eventually bringing about a severe asset price deflation.

Exhibit 11: Asset Allocation under Different Scenarios

Constructing global portfolios based on scenario analysis and probable outcomes provides helpful insights into the interplay of various asset classes, making for a more disciplined and better structured investment process. Nevertheless, even the best constructed strategies could be humbled by the increasingly complex and complicated global investment landscape. As our officemate, Craig Drill, recently wrote, “We live east of Eden…in an imperfect and dangerous world.”

Dimitri Balatsos is Managing Partner and Chief Investment Officer of Tesseract Partners, an investment advisory firm he founded in 1996. Tesseract Partners offers discretionary and non-discretionary investment management, as well as third-party marketing services.

Disclaimer: This report was prepared by Dimitri Balatsos of Tesseract Partners and reflects the current opinion of the author. It is confidential and proprietary. It is for information purposes only and is not intended to be used, and may not be used, as an investment or tax advice. No express or implied representation or warranty is being made with respect to its accuracy or completeness. It is based upon sources and data believed to be accurate and reliable. Opinions and forward-looking statements expressed are subject to change without notice. This report does not constitute a solicitation or an offer to buy or sell any security or investment products, or to provide investment advisory services. Investing involves risk. There is no guarantee or other promise as to any results that may be obtained from using the report. Past performance is not indicative of future performance.