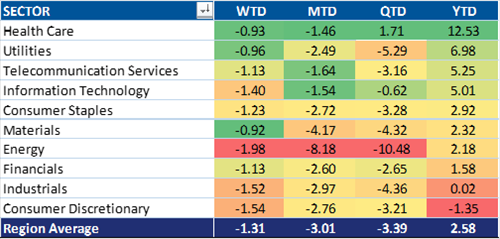

On an equal weighted basis, the MSCI World index is up 2.58% YTD, is down 3.39% QTD and down 3.01% MTD. The equal weight index gives us a better idea of our chances of picking stocks that outperform.

Performance of MSCI World Sectors

Next let's delve a little deeper in the internals of the market to give some context to the performance of the market in general. To set the table let me show the geographic breakdown of the MSCI World index. Roughly 44% of the 1,610 companies in the MSCI World Index are domiciled in North America, while 27.6% of companies are located in Europe and 28.2% are located in Asia.

Geographic Breakdown of MSCI World Index

Let’s start with a comparison between the main geographies that comprise the MSCI World index.

North America.

On equal weight basis, North America is up 6.33% YTD, with the health care sector in the lead.

Performance of MSCI North America Sectors

When we drill down and look and the percent of companies outperforming the MSCI World index, we can see that 55% of North American companies are outperforming YTD, with the highest rates of outperformance in the defensive utility and health care sectors.

Percent of MSCI North America Outperforming MSCI World Index

Europe

Performance in Europe has been comparatively worse. On average, European stocks are down 3.05% YTD, -7.58% QTD and -3.34% MTD. Here again, health care (and other defensive sectors) have led performance.

Performance of MSCI Europe Index

Only 34% of companies in Europe have outperformed the MSCI World index this year, which indicates the odds of picking outperforming stocks have been quite low.

Percent of Companies Outperforming MSCI World Index

Asia

The average company in Asia has fared somewhat better than Europe, but still not close to the performance of North America.

Performance MSCI Asia

The equal weight basket of Asian stocks is only up 2.22% YTD and is down 2.5% QTD and- 2.88% MTD. Once again defensive sectors have led, with health care the second best performing sector. Less than half of the companies in the MSCI Asia index have outperformed this year.

Percent Outperforming MSCI World Index

Next let me add some detail to illustrate the tumult underneath the surface of the market. A bear market is traditionally defined as down 20% from highs. In the table below, I break out the performance of all stocks in the MSCI world index by grouping.

Performance of MSCI World index By Group

Nearly 18% of the stocks in the MSCI World index are down more than 20% over their one year highs. A further 33% of stocks are down between 10-20%. So, 51% of all stocks in the MSCI World index are down at least 10% from one year highs.

Performance of MSCI Europe Index By Group

29% of European stocks are down more than 20% from one year highs, and 68% of European stocks are down more than 10% from one year highs. The odds of picking a loser have been high in Europe.

Performance of MSCI Asia Index by Group

18% of Asian stocks are down more than 20% from one year highs and an additional 40% are down 10-20% from one year highs. So, 58% of all Asian stocks are down more than 10% from one year highs.

Performance of MSCI North America By Group

By contrast, only 11% of North American companies are down more than 20% and 65% of all North American companies are down less than 10% from one year highs.

Below are some charts that reinforce the point that the bull market of the last few years has been exclusively an American phenomenon. While North America has outperformed (on a market cap weighted basis) by 20% over the last five years, Europe has underperformed by 20% and Asia by 25%.

Additionally, on a country basis, only the US and Denmark have outperformed over the last five years. That’s only 2 out of 24 countries that have outperformed the MSCI World Index.

For comparison, many major countries have had fairly dismal performance. For example, Japan, Germany and the UK have all underperformed significantly over the last five years.

From still another perspective, let me demonstrate the difficulty in stock picking over the last few years. Roughly 75% of the MSCI World Index is cyclicals—companies in the consumer discretionary, financial, technology, energy, materials and industrial sectors. Given all the fiscal/monetary stimulus of the last few years, one sure would have thought these cyclical areas would have outperformed. That would would have been incorrect. In the chart below I show the relative performance of all cyclicals in the MSCI World index.

So, roughly 75% of the companies in the MSCI World index have underperformed by 10% over the last four years. This means only 25% of the stocks in the MSCI World Index have driven the performance of the whole index. Leadership in the global equity market has been quite narrow, with cyclicals underperforming.

A very narrow slice of the global, developed equity markets have been in a bull market. North American health care, which represents only 9.2% of the MSCI World index, and North American consumer discretionary, which is 15.8% of the MSCI World Index have carried performance over the last five years for the whole MSCI World index.

Global equity market performance has been a bit of an optical illusion the last few years, with the vast majority of stocks underperforming the index, and those that did outperform tended to be counter-cyclical. Every day we see more evidence that even the bull market in the US is getting riskier and riskier. Recent evidence includes fewer sectors outperforming, high yield spreads widening, small cap stocks negative on the year, flattening yield curve, etc.