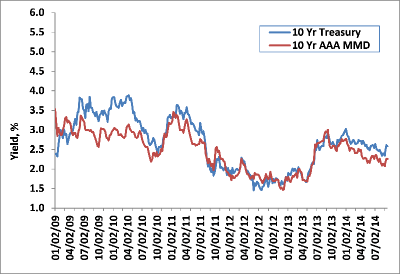

In a week defined by increased rate volatility, Treasury yields ended mixed, as the yield curve continued to flatten. Registering its first monthly decline in over a year, the Consumer Price Index (CPI) continued to support a benign inflationary environment, further supporting long-dated instruments. With global inflation subdued, central banks around the world remain more concerned about lapsing back into recession than about frothy risk markets and potential bubbles.

With the Federal Open Market Committee having concluded its September meeting last week, market participants are slowly accepting that the first hike in the next interest rate cycle will occur sometime in the middle of next year. We remind investors of the last time the Fed embarked on raising rates, June 2004 to August 2006, and very much expect a similar outcome—namely, a gradual and deliberate approach. During that period, the FOMC raised short rates a total of 425 basis points, from 1% to 5.25%. However, it was only short-dated maturities that rose, with maturities beyond ten years actually falling. In her post meeting press conference, FOMC Chair Janet Yellen reiterated that the Fed is completely data dependent. In other words, the economy—and less so the Fed—is going to drive the future direction of monetary policy. The next big event on the data calendar is not until the September jobs report on October 3rd.

This week is fairly quiet on the economic front, with the real hurdle for Treasuries being an additional $93 billion in new supply. With this supply heavily weighed inside of 5 years, we expect the “crowded” flattening trade to continue. With six members of the FOMC scheduled to speak, we suspect rate volatility—and perhaps trading opportunities—to remain elevated.

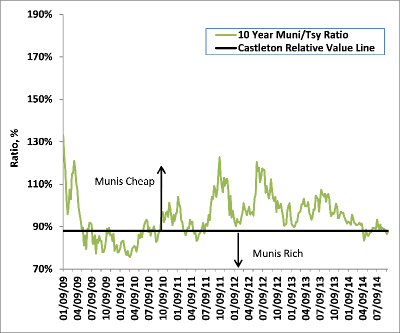

Weekly Change: 10Y Treasury Yields vs. Ratio of 10Y Muni Yield to 10Y Treasury Yield

10Y AAA MMD Source: Bloomberg, Thomson Reuters and Castleton Partners

Source: Bloomberg, Thomson Reuters and Castleton Partners

Tax-Exempt

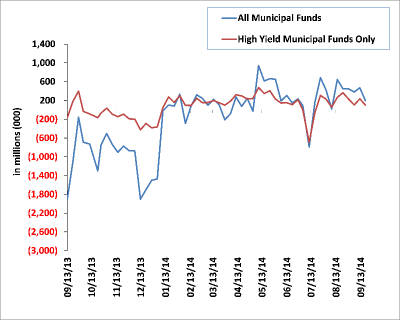

Municipal yields closed last week little changed, digesting with ease the largest new issue calendar in months. The tax exempt market continues to register strong investor demand—both from traditional and non-traditional sources. For the tenth consecutive week, mutual funds recorded net positive funds flows. Additionally, the latest data from the Federal Reserve recorded the highest holdings of tax exempts ever among banks: $435 billion! Banks continue to favor the high quality and relative safety of the asset class.

Like it’s Treasury counterpart, the municipal curve continues to flatten, with the 10y to 30y yield differential near its narrowest spread in over a year (92 basis points). We advocate the 10y to 15y area of the tax exempt curve as representing the best value. By positioning in the 10y to 15y area, investors capture 84% of the yield that is offered in the municipal high grade curve, while significantly reducing duration.

Supply remains elevated this week, with over $8 billion expected to price. However, over half of this total is headlined by two different negotiated loans: $2.5 billion California State G.O. (Aa3/A) and $2 billion for New York Sales Tax Receivables Corp (Aa1/ AAA). Being that these two loans are from two of the highest combined taxed states (federal + state), we anticipate strong investor interest. Additionally, the size of these two deals—and ensuing liquidity—should produce interest outside of the traditional tax exempt arena, as well.

AAA Municipal Market Data (MMD) Yield Curve

Source: Thomson Reuters

Weekly Municipal Mutual Fund Flow Data

Source: Lipper AMG Data

Taxable

Over the course of the week, high grade bond spreads widened by 2 basis points, with the non-financial sectors primarily accounting for the slight underperformance relative to Treasuries. With investor attention squarely focused on the FOMC meeting, supply dropped noticeably from the prior two weeks, to the lowest level in September. Financials accounted for nearly 60% of last week’s $26 billion of new debt, with the 5 year tenor the most issued maturity.

© 2014 Castleton Partners, LLC. All rights reserved.

THE FOLLOWING NOTES AND DISCLOSURES ARE AN INTEGRAL PART OF THIS REPORT: Past performance is not a guarantee of future results. Different investments involve varying degrees of risk, including the risk of illiquidity and the risk that you could lose part or all of your investment. There can be no assurance that the future performance of any specific investment, investment strategy, or product (including those discussed herein or recommended or undertaken by Castleton Partners, LLC) will be profitable, equal any corresponding indicated historical performance, be suitable for your portfolio or individual situation, or prove successful. Charts, graphs and indices are included herein only for reference and do not constitute forecasts of the past or predicted future performance of any investment. Indices are not investments. Due to changing market conditions and other factors the content herein may no longer reflect Castleton Partners, LLC’s current opinions or positions. Nothing discussed herein is or is intended as tax, legal, accounting or personalized investment advice from Castleton Partners, LLC. Should you have any questions regarding the applicability of any specific issue discussed herein we encourage you to consult competent advisers of your choosing. Nothing herein is or is intended as an offer to sell or a solicitation of offers to buy any security. Castleton Partners, LLC’s current written disclosure statement including discussion of our advisory services and fees is available upon request.