It’s Time for Your Portfolio to Break from Tradition

A multisector approach may be helpful in addressing a challenging bond market

Authors: Kathleen Gaffney and Kevin Dachille

SUMMARY

- Investors with a traditional core allocation to fixed income may not be able to rely on yesterday’s sources of risk and return.

- An allocation to a multisector bond approach with exposure to nontraditional fixed-income asset classes may help restore some of the missing return potential.

- In today’s challenging bond market, we see idiosyncratic risks – factors pertaining to individual issuers – as a source of potential return.

For several years now, investors have been hearing the alarm bells ring about the threat rising interest rates pose to their fixed-income portfolios. But so far, it has been mostly smoke and little fire. After the U.S. Federal Reserve (Fed) first indicated in May 2013 that it was prepared to scale back its long-term bond purchases, the yield on the 10-year U.S. Treasury nearly doubled from 1.66% in May 2013 to 3.04% at the end of 2013. Since then, the 10-year Treasury yield has fallen below 2.40% (as of 8/31/2014). Slow global growth may have, indeed, helped postpone the likely pain from a further significant rise in long-term rates.

Even so, over the past couple of years, investors who rely on traditional core and core-plus strategies are finding the bond market environment even less conducive to help meet their fixed-income return targets. That is because the yields on high-yield bonds and other volatile assets have also fallen as yield-starved investors have sought alternatives to the paltry returns on government issues.

In a very challenging bond market, we argue in this Insight in favor of a multisector bond approach with an expanded global opportunity set. This strategy may allow investors to take advantage of attractively priced individual issues in both traditional and nontraditional asset classes across the globe.

Traditional bond market risks look increasingly expensive

In the recovery phase of a typical corporate credit cycle, risky assets like high-yield bonds historically have outperformed U.S. Treasurys. In a typical recovery scenario, stronger growth results in increasing rates along with improved corporate balance sheets and profitability. As a result, the yield spreads of corporate debt over U.S. Treasurys have typically tightened as rates have risen.

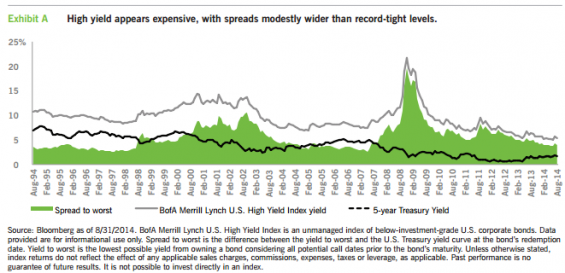

The recent recovery has turned into an economic expansion – one that has differed from the historical pattern in that rates have fallen – and there has already been significant spread compression in all fixed-income sectors, as Exhibit A shows. For us, the implication of this is that once long-term rates start to rise, there is little likelihood of significant further tightening – there would be no expectation that credit instruments, as a whole, outperform U.S. Treasurys.

Thus, we are in a position where interest rates and credit – the two biggest bond market systematic risks – appear to offer significant risk, without comparable return potential. Unfortunately, the difficult environment also includes the emergence of other broad risk factors, like liquidity.

Liquidity appears to be the next big challenge

The huge volume of funds flowing into more volatile asset classes can help set the stage for a technical correction if too many investors – for whatever reason – seek the exit at the same time. We don’t anticipate anything on the order of magnitude of the 2008 financial crisis, but that episode underscores the fact that nothing except government issues should be considered immune to liquidity crunches.

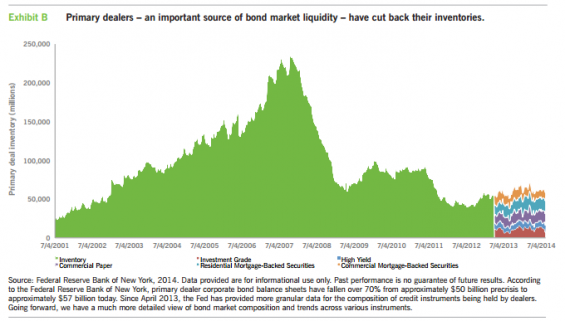

Moreover, in the postcrisis period, primary bond dealers – those who deal directly with the Fed – have cut back their corporate bond inventories (Exhibit B). This means that in a time of diminished liquidity, we are less likely to see dealers step up and provide a “backstop†as a buyer of last resort.

Another important technical factor – one that is unique to the postcrisis era – involves the winding down of the Fed’s purchases of mortgage-backed securities (MBS) as part of quantitative easing (QE). Fed MBS purchases were reported to be about $40 billion per month prior to the “tapering†that began last year, and is now scheduled to end in October. Even with its purchases winding down, the Fed owns roughly one-third of all outstanding issues. MBS are a major component of the bond market, comprising 29% of the Barclays U.S. Aggregate Bond Index. The withdrawal of this big chunk of demand by the Fed is likely to be a significant downward force on MBS prices.

Keys to multisector success

With the traditional macro factors apparently “out of steam†in terms of driving positive fixed-income returns, we believe that a multisector approach is best positioned to find relative value. This involves both expanding the opportunity set to include nontraditional asset classes across the globe and using intensive, proprietary research to discover attractively priced individual issues within that larger universe.

Â

Â

The multisector approach relies principally on analyzing idiosyncratic factors pertaining to individual issuers rather than the global forces we have discussed. These factors encompass the entire range of fundamental analysis, such as understanding a company’s product line, sector, competitive positioning, management strengths and weaknesses, balance sheet, cash flow and so forth. In our opinion, success in multisector investing typically requires:

- Skill across multiple sectors: A portfolio management team must have the expertise and depth to independently analyze portfolio holdings across many sectors and regions, in contrast to an approach that intensively studies a handful of macro factors.

- Being nimble: In today’s environment, the windows of opportunity for perceived value often don’t last long. Managers must be able to move quickly, and this often depends on the teamwork, communication and preparation that are the foundation for good research.

- Wider tracking error: Because of the wide latitude the manager has both in the size of positions and out-of-index investments, investors should allow for the likelihood that there will be less correlation between a traditional fixed income index, like the Barclays U.S. Aggregate Bond Index, and a multisector strategy.

How a multisector approach may fit within a portfolio

Thus far, we have addressed the advantages in today’s environment of seeking return from idiosyncratic risk. But we also believe the addition of idiosyncratic risk can aid the construction of portfolios, regardless of current conditions. We assume that the great majority of fixed-income allocations are predominantly index-based and, therefore, are mostly exposed to traditional bond market risks, like interest rates or credit. From that perspective, idiosyncratic risk can be viewed as a good diversifier – not just as a matter of expectation, but of definition. Idiosyncratic risk is the residual that cannot be explained by overall market variance.

A core tenet of portfolio theory also notes that idiosyncratic risk can be diversified away, unlike systematic risk. Thus, risk can be minimized within a well-constructed multisector strategy with multiple exposures, even when viewed as a stand-alone portfolio.

In our approach to investing, we do not tie ourselves to a particular sector, style box or benchmark. By removing biases to investing, we can objectively and tactically look for potential investment opportunities, which may deviate from consensus. We believe in embracing uncertainty in order to find opportunities.

Finally, we believe that the attractiveness of a multisector allocation will endure across business and economic cycles, even when the expected return for systematic risk becomes more favorable. The bond market, in our view, will always be rife with inefficiencies and mispricings, so there will always be the potential for managers with skill and expertise to add value.

Bond market risks that may still be worth taking

Following are examples of sectors that we believe offer the best opportunities for value in today’s environment:

- Fallen angels: Global M&A reached a seven-year high in 2014, which also implies that much debt was issued to finance the transactions. Inevitably, some acquiring companies lose their investment-grade rating in the process of adding more debt. Careful analysis can often discern “fallen angels†that may offer more value than their downgrading implies.

- Non-U.S. developed-market debt: Even though interest rates are low globally, we believe that non-U.S. corporate and sovereign issuers of nondollar-denominated debt often offer better relative value than U.S. debt. Expanding the opportunity set this way may allow managers to construct higher-yielding, better-diversified portfolios.

- Local emerging-market debt: The markets of many developing countries have matured to the point of supporting debt issuance in the local currency. It is the fastest-growing segment of the non-U.S. debt market, offering the potential for both higher yields than in the U.S. and a way to diversify away from the U.S. dollar.

- Municipal “crossover†investments: The municipal market historically has been driven by different factors than the bond market as a whole, such as the financial condition of state and local governments, and the prospects for changes in the tax law. Periodically, such factors can make prices sufficiently appealing to crossover buyers, including tax-exempt investors who gain no advantage from the tax-free status of municipal bonds.

- Commodity-linked credits: This category includes a broad array of issuers, both corporate and sovereign, whose balance sheets are backed by real assets such as gold and timber. Such debt may serve as an inflation hedge once the global economy gains steam and the trillions of dollars worth of reserves created by central banks in recent years starts flowing into the system.

- Floating-rate loans: With the potential for increases in short-term rates seen on the horizon, the case for floating-rate loans is a fairly straightforward one: They are designed to keep pace with changes in short-term rates, based on a spread above Libor. That is why, historically, floating-rate loans have been negatively correlated with U.S. Treasurys. Floating-rate loans are unique in the bond world in that they are generally senior in the company's capital structure and secured by specific assets.

- Convertible bonds/preferred stock: These securities offer both the potential for income and exposure to the equity value of the issuer. With the flexibility to participate anywhere in a company’s capital structure – whether it involves bonds, convertibles, floating-rate loans or preferred stock – a manager can take advantage of possible inefficiencies that arise in the market, and have more opportunities to build value in the portfolio.

It’s time to break from tradition with your fixed-income allocation

The challenges of today’s bond market cannot be met by relying on yesterday’s sources of risk and return. The anticipated spread compression that historically boosts the credit sector when the economy takes off has already taken place – most of that juice has already been squeezed. Fortunately, the potential return from idiosyncratic risk is independent of the economic cycle. We believe that a multisector manager with the proper expertise and commitment to capturing that return can be of great value to investors seeking to stay on track in meeting their fixed-income targets.

About Asset Class Comparisons

Elements of this report include comparisons of different asset classes, each of which has distinct risk and return characteristics. Every investment carries risk, and principal values and performance will fluctuate with all asset classes shown, sometimes substantially. Asset classes shown are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. All asset classes shown are subject to risks, including possible loss of principal invested. The principal risks involved with investing in the asset classes shown are interest-rate risk, credit risk and liquidity risk, with each asset class shown offering a distinct combination of these risks. Generally, considered along a spectrum of risks and return potential, U.S. Treasury securities (which are guaranteed as to the payment of principal and interest by the U.S. government) offer lower credit risk, higher levels of liquidity, higher interest-rate risk and lower return potential, whereas asset classes such as high-yield corporate bonds and emerging-market bonds offer higher credit risk, lower levels of liquidity, lower interest-rate risk and higher return potential. Other asset classes shown carry different levels of each of these risk and return characteristics, and as a result generally fall varying degrees along the risk/return spectrum. Costs and expenses associated with investing in asset classes shown will vary, sometimes substantially, depending upon specific investment vehicles chosen. No investment in the asset classes shown is insured or guaranteed, unless explicitly stated for a specific investment vehicle. Interest income earned on asset classes shown is subject to ordinary federal, state and local income taxes, except U.S. Treasury securities (exempt from state and local income taxes) and municipal securities (exempt from federal income taxes, with certain securities exempt from federal, state and local income taxes). In addition, federal and/or state capital gains taxes may apply to investments that are sold at a profit. Eaton Vance does not provide tax or legal advice. Prospective investors should consult with a tax or legal advisor before making any investment decision.

About Risk

An imbalance in supply and demand in the income market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. Investments in foreign instruments or currencies can involve greater risk and volatility than U.S. investments because of adverse market, economic, political, regulatory, geopolitical or other conditions. In emerging countries, these risks may be more significant. As interest rates rise, the value of certain income investments is likely to decline. Investments in income securities may be affected by changes in the creditworthiness of the issuer and are subject to the risk of nonpayment of principal and interest. The value of income securities also may decline because of real or perceived concerns about the issuer’s ability to make principal and interest payments. No Fund is a complete investment program and you may lose money investing in a Fund. The Fund may engage in other investment practices that may involve additional risks and you should review the Fund prospectus for a complete description.

About Eaton Vance

Eaton Vance Corp. is one of the oldest investment management firms in the United States, with a history dating to 1924. Eaton Vance and its affiliates offer individuals and institutions a broad array of investment strategies and wealth management solutions. The Company’s long record of exemplary service, timely innovation and attractive returns through a variety of market conditions has made Eaton Vance the investment manager of choice for many of today’s most discerning investors. For more information, visit eatonvance.com.

The views expressed in this Insight are those of the authors and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and Eaton Vance disclaims any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Eaton Vance are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund.

This Insight may contain statements that are not historical facts, referred to as forward-looking statements. Future results may differ significantly from those stated in forward-looking statements, depending on factors such as changes in securities or financial markets or general economic conditions.

Before investing, investors should consider carefully the investment objectives, risks, charges and expenses of a mutual fund. This and other important information is contained in the prospectus and summary prospectus, which can be obtained from a financial advisor. Prospective investors should read the prospectus carefully before investing.

©2014 Eaton Vance Distributors, Inc | Member FINRA/SIPC | Two International Place, Boston, MA 02110 | 800.836.2414