Alternative Approaches for Managing Emerging Market Equity Portfolios

EXECUTIVE SUMMARY

The use of indexing in institutional investing has grown strongly over the last 15 years, roughly at the same time emerging markets have become more accepted as an asset class and a destination for investors creating global portfolios. This has meant some “leapfrogging” over the more usual chronology of a large number of active managers gaining expertise in emerging markets. Asset owners have been indexing into equity markets that are by definition immature, representing economies and political systems that are still developing.

This focus on indexing can present opportunities for active managers. The shortcomings of indexing are especially evident in frontier markets, where some very small markets have significant weights.

A wide dispersion of available returns is expected among emerging markets given the underlying countries, currencies and sectors. On an all-cap basis, emerging markets provide an extensive universe that is growing strongly in terms of newly listed equities (helped by private-equity formation).

This paper discusses three approaches for targeting inefficiencies in emerging markets, with the goal of capturing some of the investment returns missed by traditional methods. The three broad approaches discussed are:

- Targeting small companies

- Targeting frontier markets and emerging small countries

- Targeting select companies across all market-cap segments

Within these approaches, a number of strategies can be employed for managing portfolio risk and volatility, while potentially enhancing returns. These include:

- Focusing on high-quality companies with defensible business models and sustainable competitive advantages

- Avoiding global cyclical companies

- Underweighting or avoiding countries dependent upon exports to the developed world

- Emphasizing countries with attractively valued stock markets and growing consumer economies driven by domestic (home-country) demand and an expanding middle class

TYPICAL APPROACHES TO EMERGING MARKETS

Countries with large stock-market capitalizations— together with the largest-capitalization companies from other emerging markets—traditionally have accounted for the greater part of emerging-market equity portfolios. Among the reasons for this are the prevalence of index investing and the practice of benchmarking relative to an index. Indices heavily weighted in large-cap (often mega-cap) companies encourage even the active manager to build a portfolio around the index in order to reduce the risk of seriously underperforming his or her benchmark.

To the extent that an actively managed portfolio departs from its benchmark, incentives for the manager to favor large-cap companies remain significant. First, by taking positions in large companies closely correlated with the index, the manager can closely track the benchmark without being restricted to investing only in its components. Second, conducting proprietary research in emerging markets can be difficult. The tendency for institutional research to focus on the larger countries and companies may limit the manager’s access to information outside those areas. Third, structural impediments to investing in certain countries and small companies may constrain some asset-management firms. Fourth, a portfolio of large companies is more readily scalable and offers greater potential fees for the firm.

Large Exporting Countries

One of the key weaknesses of typical approaches to emerging markets is poor diversification with respect to geography. For example, as of March 31, 2014, 55% of the MSCI Emerging Markets Index was represented by its four most-heavily weighted countries—China, Korea, Taiwan and Brazil. Those countries, as well as many of the companies typically favored by emerging-market investors, are large exporters of products to the developed world.

The outcome can be a portfolio laden with global cyclical companies and other holdings offering more exposure to developed countries than to their own. High correlation among portfolio securities is a common result (especially in the materials and energy sectors, which tend to be influenced by global prices). The tendency for the stocks of large, globally oriented companies to move in unison adds to portfolio volatility, as well as to the perceived riskiness of emerging-market investing. Those factors, in turn, may serve to further discourage managers from venturing into smaller companies in even less familiar locations.

State-Owned Companies

Significant exposure to state-owned companies is another common problem. In the 1990s, most of these companies were little more than government departments. Investors assumed that, as the countries grew, their state owned companies would be privatized or shut down. Today, government-backed companies are bigger than ever. For example, the world’s 10 largest oil-and-gas producers, as measured by reserves, are all state-owned.

State-owned companies do not always operate in the best interests of shareholders. These companies may instead pursue national interests or the government’s own political objectives. Nevertheless, many of the companies in emerging-market indices are state owned—including eight of the 20 largest positions in the MSCI Emerging Markets Index. Government-backed companies account for approximately 80% of China’s market capitalization and 60% of Russia’s. From 2003 to 2010, about one-third of all direct foreign investment in emerging markets went into state-owned companies. State capitalism for some countries is a strategic policy.

Efficient Price Discovery

With so much attention focused on the large-cap segments of emerging markets, the securities of large companies are more likely to be efficiently priced or overpriced, and less likely to represent compelling investment opportunities. As in other categories of investing, excessive conformity to traditional approaches has created opportunities for those willing to look elsewhere.

Seeking a Better Way

Each of the following alternative approaches targets a different segment of the emerging-market universe. By focusing more attention on smaller companies and on companies located outside the largest of the emerging markets, these approaches seek to identify high-growth investments that are not yet widely recognized. These approaches share a common investment style that emphasizes high quality, reasonable valuation and a long term horizon.

ALTERNATIVE APPROACH #1: TARGETING SMALL COMPANIES

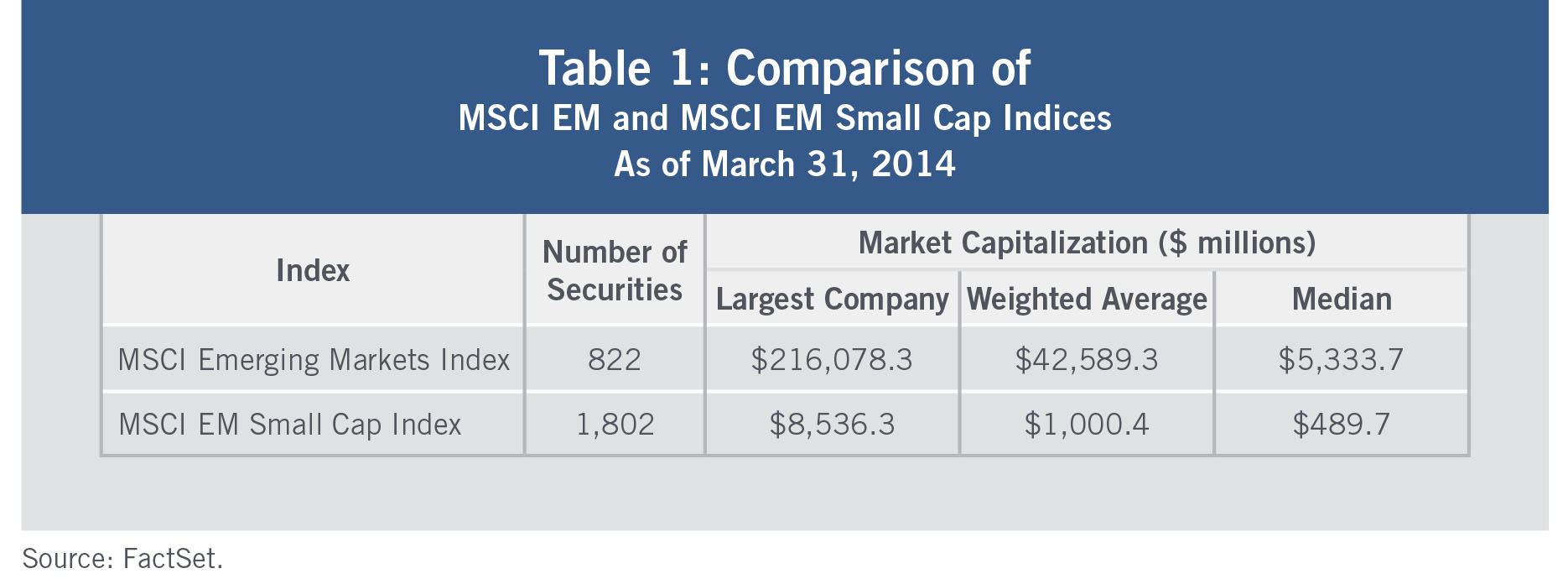

As a practical matter, small companies can be defined as those with market capitalizations less than the largest company in the MSCI Emerging Markets Small Cap Index. As shown in Table 1, that currently would include companies with capitalizations up to about $8.5 billion.

For purposes of this discussion, however, the precise way one chooses to define the terms “small-cap,” “mid cap” and “large-cap” is not important. What matters is finding inefficiently priced companies and those with characteristics shared by successful small companies.

Thinking Small

Small companies, by their very nature, can grow faster than large ones. Their small size enables them to be nimble and responsive. The most-successful small companies possess characteristics such as new products, new services, new markets and innovative delivery systems that allow them to rapidly increase sales, market share and earnings.

Information about small companies can be difficult to obtain. Coverage by research analysts may be minimal or non-existent. Large institutions and exchange-traded funds (ETFs) are not as interested in companies whose small size limits their potential for investment.

For these reasons, small companies are more likely to be overlooked by investors, and their securities are more likely to be inefficiently priced. So it seems plausible that a well-executed, small-company strategy might produce higher investment returns than a more-typical approach focused mainly on the largest companies.

Risk: An Overview

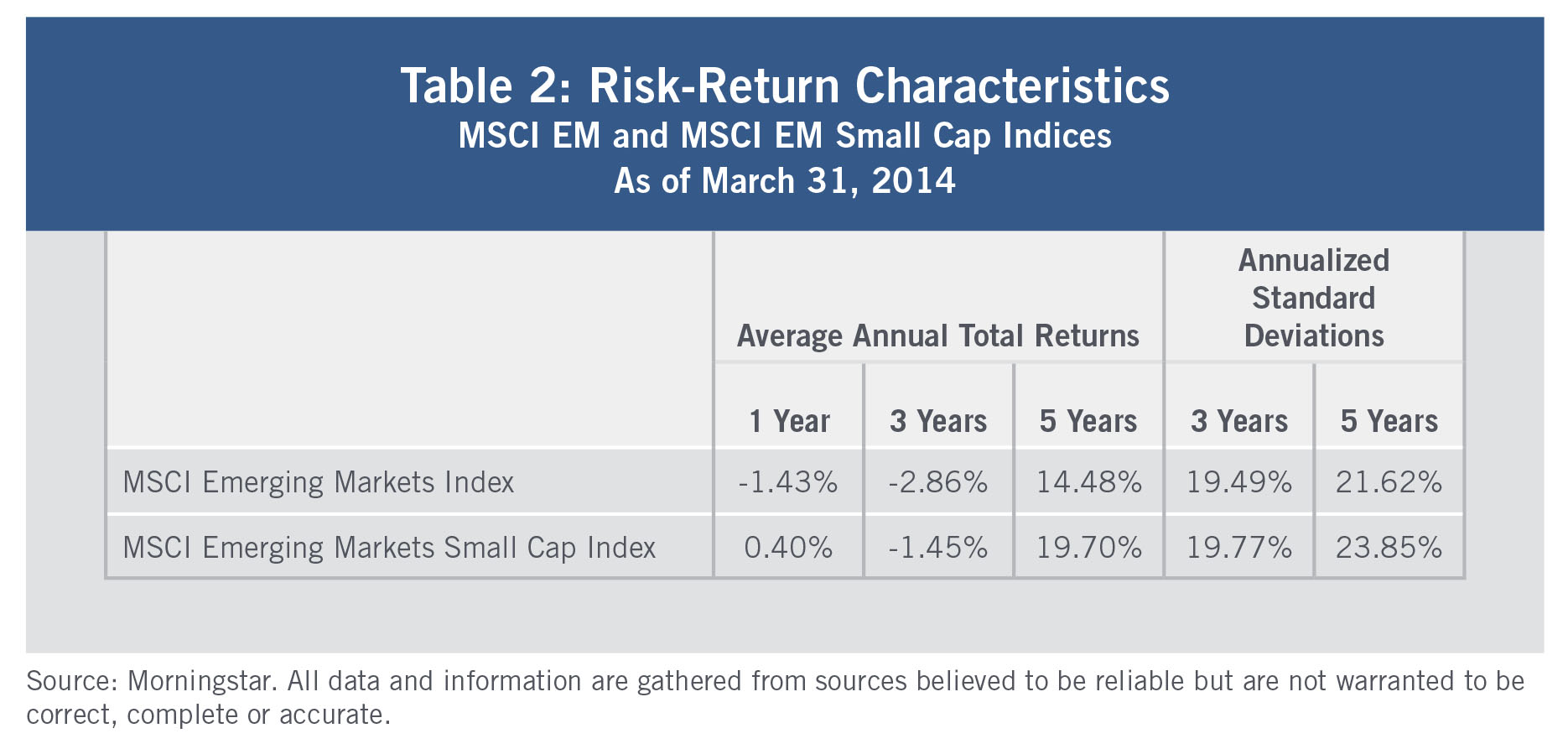

A logical question to ask is, “Does investing in small companies significantly increase portfolio volatility?” The answer suggested by Table 2 is, “Not necessarily.” Using standard deviation as the relevant measure, the MSCI Emerging Markets Small Cap Index has been only slightly more volatile than the MSCI Emerging Markets Index over the past three years (19.77% vs. 19.49%) and only moderately more volatile over the past five years (23.85% vs. 21.62%).

Despite common perceptions, small-company stock portfolios need not be significantly more volatile than comparable large-cap portfolios. The reason is the tendency for small-company stocks to behave rather idiosyncratically relative to global market and industry influences.[i] That is to say, stock-picking is more important when investing in small-caps than it is with respect to large-caps, which tend to demonstrate higher dependency on sector dynamics and the general economy. The country effect, with domestic factors being more significant, is also a major influence.

A focus on high-quality companies can help reduce small-company risk even further. Generally speaking, a geographically diversified emerging-market portfolio of quality small-cap growth companies may be expected to have a standard deviation roughly in line with the MSCI Emerging Markets Index over three- and five-year time periods.

Quality Growth Companies

High-quality growth companies possess identifiable, sustainable competitive advantages, are well-managed, and produce above-average earnings growth relative to their industries and countries of origin. In emerging markets (including frontier markets and emerging small countries), characteristics of quality companies include:

- Sustainable competitive advantages

- An experienced, proven management team

- Potential for significant and sustained revenue and earnings growth

- High return on capital

- Market leadership and/or growing market share

- Ability to capitalize on favorable long-term trends

- Strong financial health and controls

- Reasonable use of debt

- Expanding operating margins

- Substantial insider ownership

- Attractive valuation

There is also an argument to be made that for emerging markets, the opportunities available to quality companies are higher given the difficulties of access to financing.

Geographic Diversification

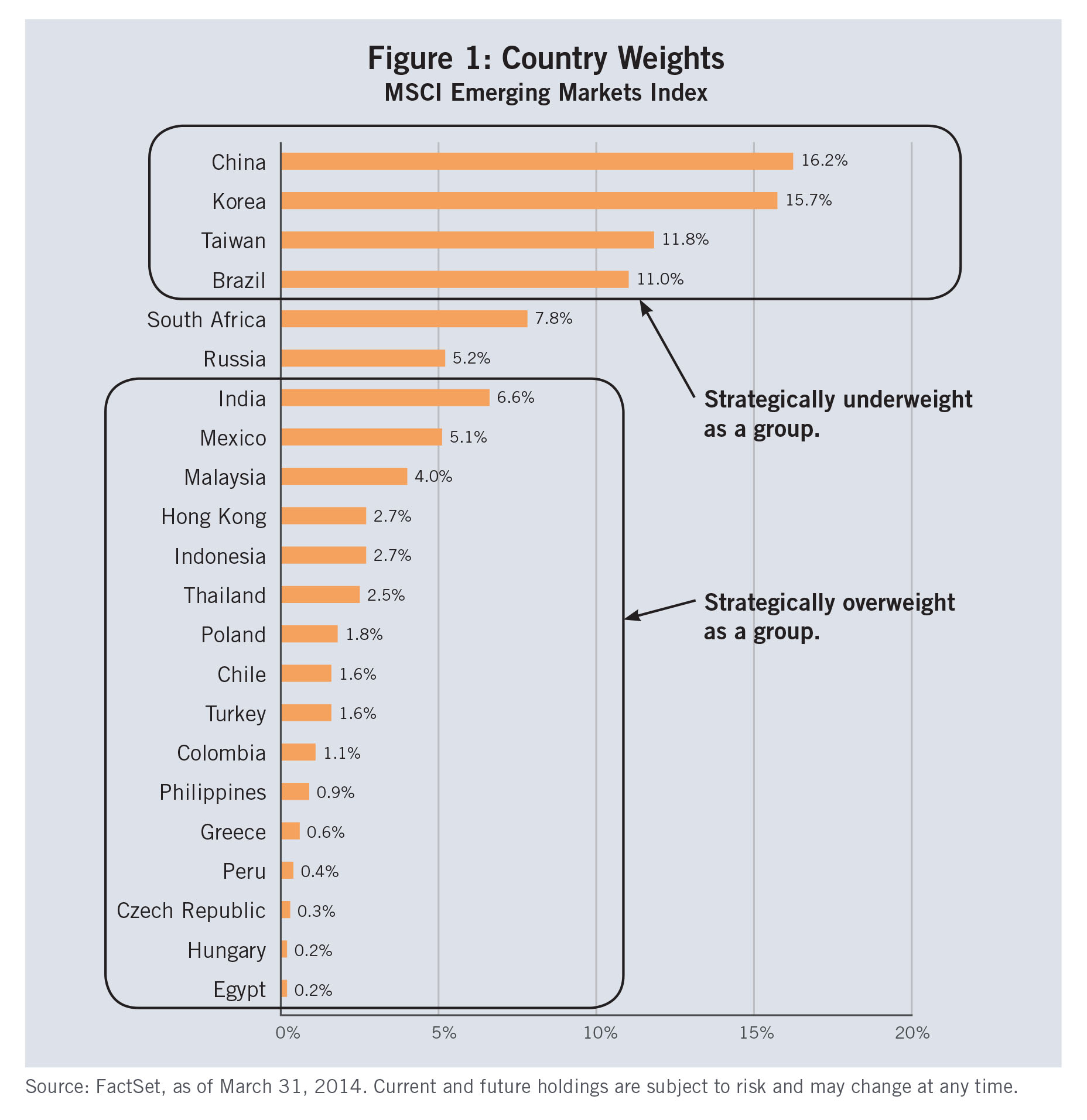

Diversification with respect to geography is another essential aspect of managing risk in emerging markets. Country weights for the MSCI Emerging Markets Index are plotted in Figure 1, which illustrates the Index’s focus on large-capitalization countries. The major, export-oriented markets of China and Korea, for example, represent 32% of the Index, while the frequently underinvested countries of Indonesia, Thailand, the Philippines and Turkey together account for only 8%.

By strategically underweighting economies driven largely by global economic factors—while strategically overweighting countries less dependent upon exports to the developed world—the emerging-market equity manager can construct a portfolio that is potentially less volatile and less correlated with developed markets.

In applying the alternative approaches described in this paper, the manager should seek countries with attractively valued stock markets and growing domestic economies. They also may be countries with a strong talent base (e.g., computer engineers) or particular structural advantages (e.g., language). In contrast, the emerging-market indices typically are constructed without regard to fundamental investment considerations such as P/E ratios or the cash flows of the underlying businesses.

ALTERNATIVE APPROACH #2: TARGETING FRONTIER MARKETS AND EMERGING SMALL COUNTRIES

Of the three alternatives, this approach ventures the furthest afield. As yet undiscovered by many investors, frontier markets and emerging small countries have lower capitalizations and less liquidity than more-developed emerging markets. Frontier and emerging small country investments include publicly listed companies across Asia, Africa, Europe, Latin America and the Middle East. Many companies in frontier markets and emerging small countries have limited analyst coverage and offer untapped investment opportunities.

The approach of targeting these countries is based on the thesis that frontier markets are in the early stages of a potentially long-term investment cycle. Frontier countries currently account for 21.6% of the world’s population, 6% of its nominal gross domestic product (GDP) and only 3.1% of world market capitalization.[ii] Large, young populations are driving urbanization and a growing middle class. Meanwhile, as burdensome regulations and taxation within the developed world continue to escalate, there is every reason to believe outsourcing and globalization trends will continue to create jobs and drive growth toward frontier markets.

The preceding factors—together with higher GDP growth trends, nascent consumer economies and low debt-to-GDP ratios—make frontier markets and the counties that are the smallest within the traditional emerging-market indices a potentially appealing country group for emerging-market investors. The goal is to capture the next generation of large emerging markets—the next BRICs (Brazil, Russia, India and China), Korea and Taiwan. As in the other alternative approaches, it is important to maintain geographic diversification and a high quality company focus when targeting frontier markets.

Why Indexing Fails

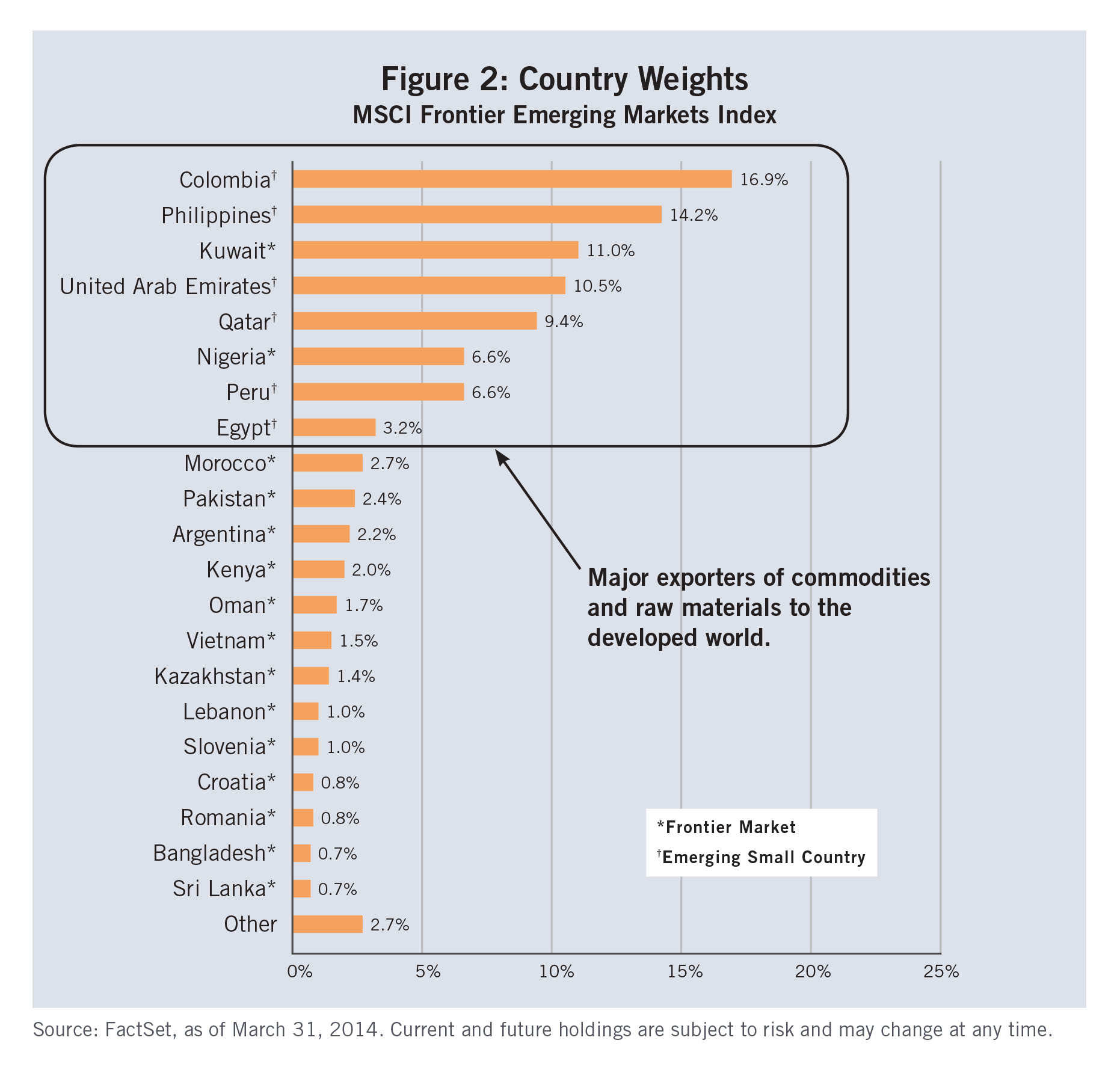

Country weights for the MSCI Frontier Emerging Markets Index are presented in Figure 2. As the figure illustrates, heavy weightings in export-dependent economies make this Index a poor candidate for passive investing. The Index also includes many state-owned companies, as well as mining companies, oil-and-gas producers and other exporters of commodities and raw materials to the developed world. Because the fortunes of these companies rise and fall as the prices of their exports fluctuate in response to global economic cycles, the components of this Index tend to be highly correlated with developed countries and with one another.

Why Geographic Diversification Works

While all world stock markets are correlated to some extent, the degree of correlation between emerging markets generally is less than for developed countries. Frontier markets tend to be the least correlated of all.

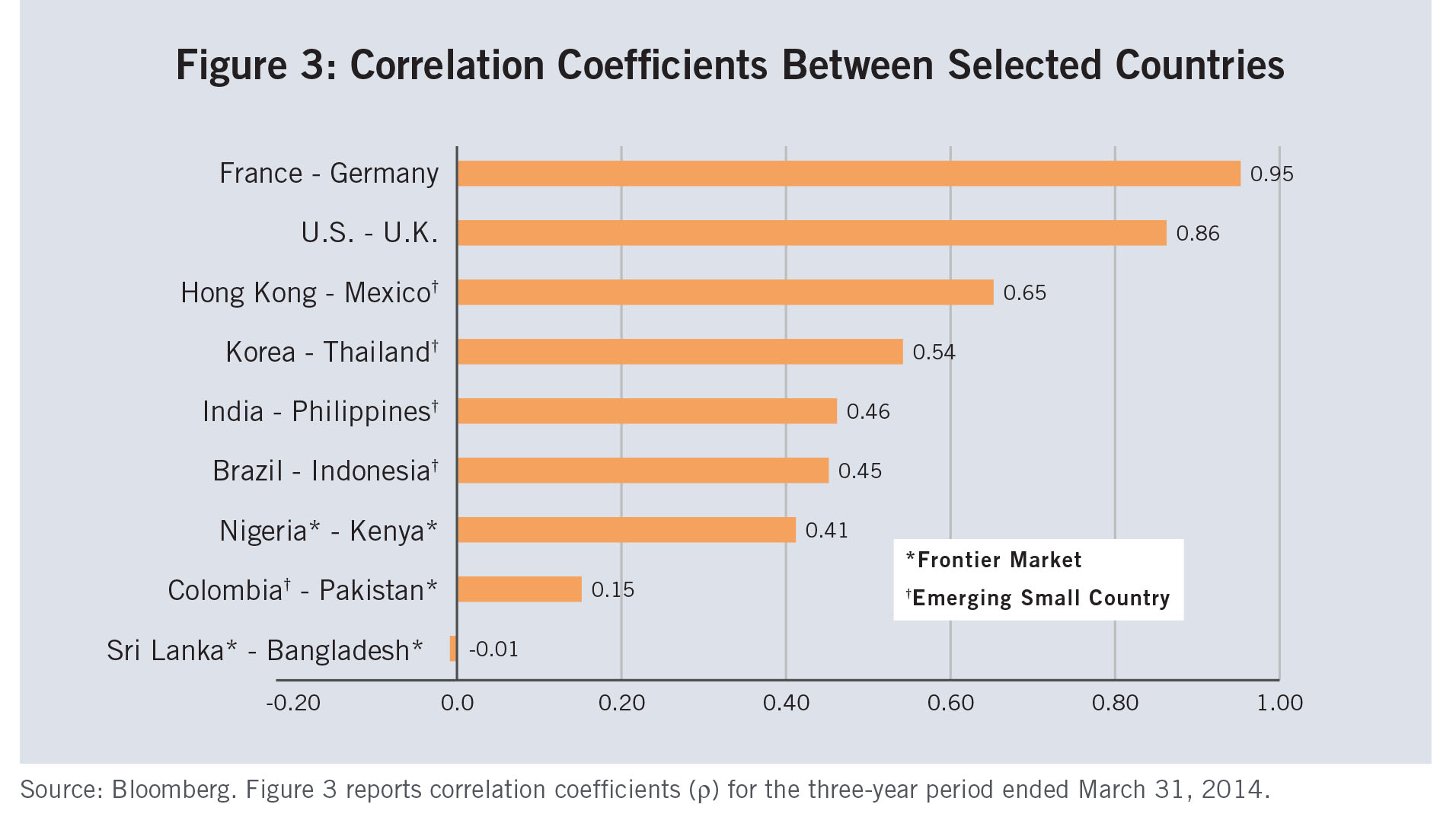

Figure 3 compares the correlation coefficients (r) between selected pairs of countries. Of the pairings shown, France and Germany (r = 0.95) are the most highly correlated. Next is U.S.-United Kingdom (U.K.) at 0.86, a number that indicates about 74% (0.862) of the variation in the British stock market can be explained by what happens on Wall Street. Among emerging markets, the correlation coefficients begin to drop off appreciably. For the three pairs including frontier markets, the coefficients are small: 0.41 for Nigeria-Kenya, 0.15 for Colombia-Pakistan and -0.01 for Sri Lanka-Bangladesh.

The message of Figure 3 is that emerging markets tend to be more local in character, driven largely by the country’s own economic and political development and less subject to whims of the global economy. This is especially true for frontier markets and emerging small countries.

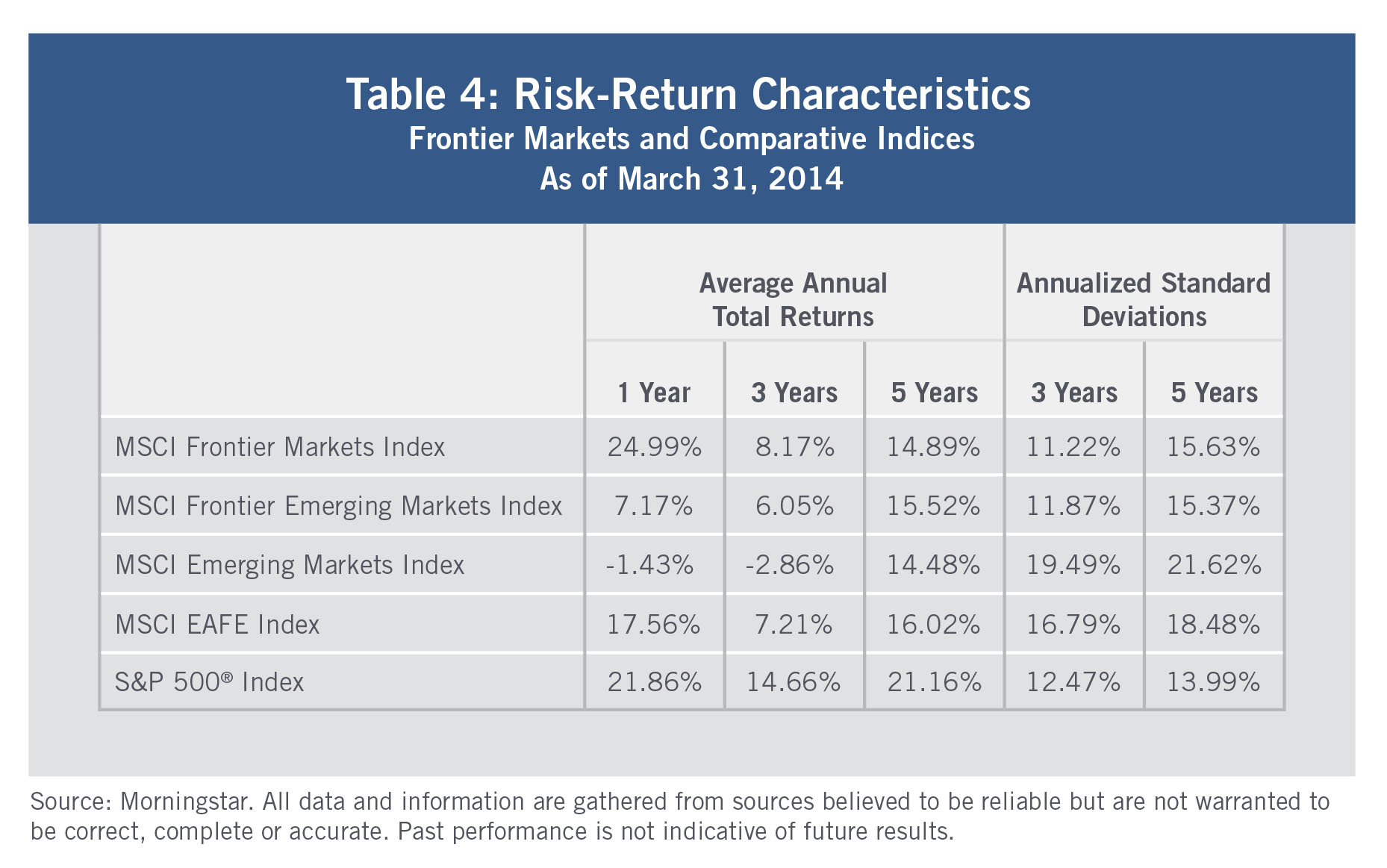

Low correlations between the holdings in a portfolio may reduce its volatility because investments that are less correlated are less likely to move together in price. This effect can be observed at work in frontier markets in Table 4, which shows returns and standard deviations for the MSCI Frontier Markets Index, the MSCI Frontier Emerging Markets Index and three other indices included for comparison. Here, as in Table 2, standard deviations provide a generally accepted yardstick for comparing the volatility of one index with another.

Even though the frontier-market indices are not as well diversified as they could be, it’s worth noting that their three-year standard deviations (11.22% and 11.87% for MSCI Frontier Markets and MSCI Frontier Emerging Markets, respectively) are lower than the indices included for comparison in Table 4. Over five years, only the S&P 500 was less volatile than the frontier indices.

Practical Implications

Low-to-moderate correlation between countries has important implications for actively managed emerging- market portfolios. In the first two alternative approaches, the benefits of geographic diversification—together with a focus on high-quality growth companies—helped offset small-company risk and small-country risk, respectively. Another consequence is that through careful portfolio construction, reasonable diversification can be achieved with fewer stocks. This important result suggests a third targeting approach: a concentrated portfolio of select companies.

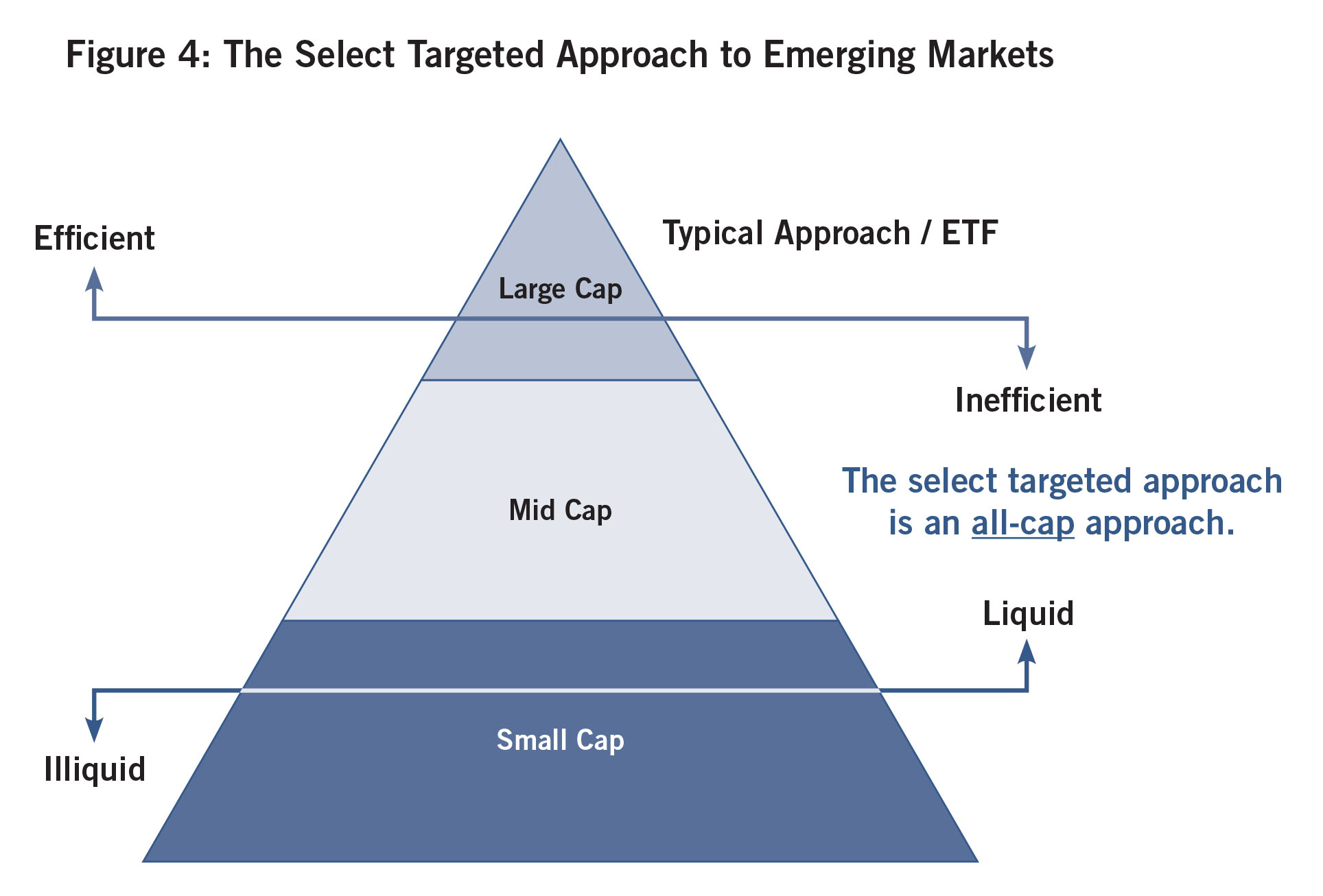

ALTERNATIVE APPROACH #3: TARGETTING SELECT COMPANIES ACROSS ALL MARKET-CAP SEGMENTS

Ideally, small companies will develop into larger companies—and thus outgrow the typically small-cap investment mandates of the already limited number of foreign portfolios that hold them. Frequently, members of this select group of companies may graduate out of the small-cap space while they remain essentially unknown to foreign investors. In addition, these companies often are neglected and poorly understood by analysts.

The select targeted approach is designed to take advantage of such inefficiencies in addition to other opportunities within the world of emerging markets, while maintaining the flexibility to invest in companies of any size. Normally, this approach involves investing in between 30 and 50 high-quality growth companies. These may be businesses the portfolio manager has followed for years while the companies were still small. Having graduated beyond the small-cap space, many of the companies may now be market leaders within their respective countries and still have room to grow.

A New Approach for Today’s Opportunities

The select targeted approach is designed for today’s emerging markets. Important aspects include a 30 to 50 stock portfolio, a typical allocation to mid-cap stocks, broad country diversification and flexibility to invest in companies of all sizes.

The proliferation of emerging-market mutual funds and exchange-traded funds (ETFs) has paralleled the development of U.S. investing. However, emerging-market investing has progressed in reverse order. Domestic U.S. mutual funds evolved from purely active management about 30 years ago, to a market-cap/style focus in the 1990s, and eventually to the heavy reliance on indexing observed today. For emerging markets, on the other hand, indexing was sufficiently prevalent at the outset that analyst coverage has been slow to develop, especially with regard to small-cap companies, mid-cap companies and smaller countries. The end result is that indexing has, in a sense, made investors blind to the opportunities available to those with the expertise and willingness to exploit these opportunities.

Managing Risk as Well as Returns

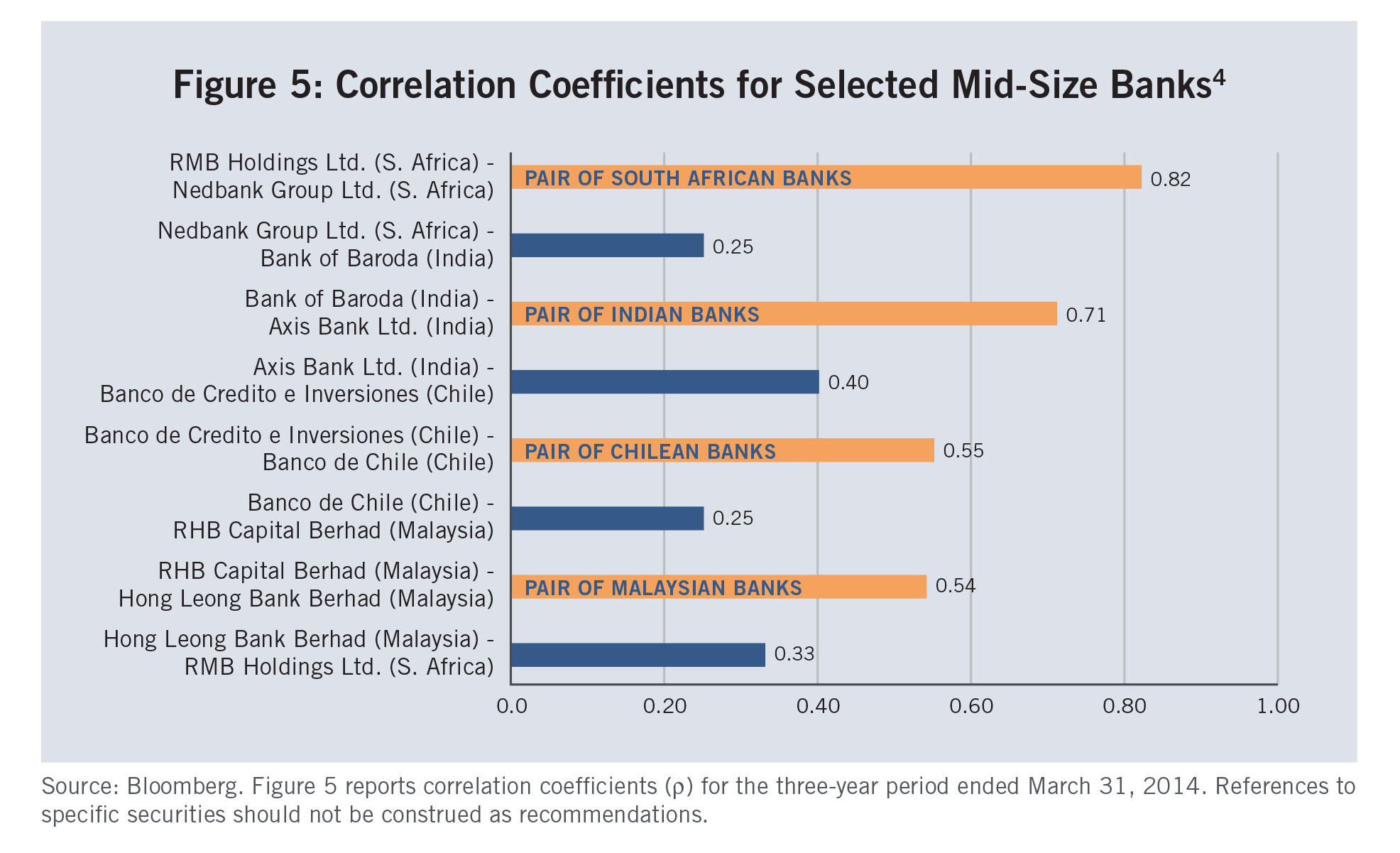

Managing a portfolio of as few as 30 stocks requires careful attention to risk. Accordingly, the risk-mitigating factors discussed previously—high-quality focus, extensive geographic diversification and low correlations between countries—take on added importance in the select targeted approach. An additional, potentially helpful dynamic is that small- to mid-cap stocks tend to display less sensitivity to global industry influences than large-cap stocks.[iii] The effects can be observed in Figure 5, which plots correlation coefficients for mid-size banks in four emerging markets.

The four orange bars in Figure 5 represent four countries—South Africa, India, Chile and Malaysia. Each orange bar plots the correlation coefficient (r) for a pair of mid-size banks located in the represented country. The blue bars in between the orange bars plot] correlations between the previous bank listed (located in the country represented by the orange bar above the blue bar), and the following bank listed (located in the country represented by the orange bar below the blue bar).

Taking the two Indian banks as examples, the second orange bar from the top represents India and shows a correlation coefficient of 0.71 for Bank of Baroda and Axis Bank Ltd. That means about 50% (0.712) of the variation in the price of either stock can be explained by variations in the price of the other. For companies of similar size operating within the same country (India) and the same industry (banking), that is only a moderate degree of correlation to begin with. However, the blue bar above the India bar shows a sharp drop-off in correlation to only 0.25 between Bank of Baroda and the previous bank listed, Nedbank Group Ltd. of South Africa. Note that for these two banks the explained variation has fallen to only 0.252, or 6.3%. The remaining 93.7% (100% – 6.3% = 93.7%) of the variation in each bank’s stock price occurs independently of the other bank’s stock price.

Continuing with the example of the Indian banks, the blue bar below the orange India bar denotes a correlation of 0.40 between the second Indian bank, Axis Bank Ltd., and the following bank listed, Banco de Credito e Inversiones of Chile. For this pair, only about 16% (0.402) of the variation in one bank’s stock price can be explained by variations in the price of the other. Together, the examples in Figure 5 serve to illustrate the weak industry correlation effects for emerging-market mid-caps, especially between companies in different countries.

The upshot for emerging-market mid-cap as an asset class is that research and analysis of individual companies, security selection and country allocation are likely to be better risk-control tools than top-down industry allocation. Moreover, for an emerging-market mid-cap portfolio that is already geographically diversified, the risk benefits of additional industry diversification are not great, and so it is not necessary to have large numbers of stocks in the portfolio.

Exploiting Inefficiencies

The approach of targeting 30 to 50 select companies is a promising way to exploit new opportunities that arise from inefficiencies in today’s emerging markets. The approach may be appropriate for core exposure to emerging markets, or for a high-alpha complement to existing investments.

SUMMARY AND CONCLUSIONS

Each of the three alternative approaches presented uses a different targeting method to seek returns with different drivers and different sources of alpha. Consequently, these approaches are designed to fit together and complement each other within an investment portfolio. Overlap between the approaches is generally minimal, so investors may reasonably employ all three

Key Drivers

Urbanization, deregulation, population growth, an emerging middle class and GDP growth resulting in rising personal incomes are some of the well-documented drivers of economic change in emerging economies. Demographic trends are also favorable for many of these countries. For these trends to be translated into well-founded growth, it requires improving institutional arrangements in these countries. This growth has to be backed by functioning banking systems, and ideally stable currencies and interest rates. It is a delicate balancing act to reap the dividend of population growth and increased productivity.

Companies with domestic-demand orientations tend to be less sensitive to global economic factors and more dependent upon developments within their home countries. Accordingly, extensive geographic diversification may provide risk benefits not available to index funds that are heavily weighted in larger exporting countries tied to the developed world.

Long-Term Horizon

Because the drivers behind these approaches to emerging markets are long-term in nature, portfolio managers and investors are well-advised to adopt a long-term horizon. Especially in frontier markets and emerging small countries, these approaches are designed to benefit from secular trends and long-term themes that may progress gradually or in fits and starts. In addition, high exposure to countries less correlated with developed markets may cause these approaches to perform poorly when developed countries are doing well. However, for managers and investors with realistic, long-term perspectives, these approaches provide attractive alternatives to traditional emerging-market investing.

ABOUT THE PORTFOLIO MANAGERS

Roger Edgley is Director of International Research and the Lead Portfolio Manager for the Wasatch International Growth, International Opportunities, and Emerging Markets Small Cap Funds. He is also a Portfolio Manager for the Wasatch Emerging Markets Select Fund. He joined Wasatch Advisors in 2002 and is a member of the Board of Directors. A native of the United Kingdom, he also holds U.S. citizenship and has many years of international investing experience.

Prior to joining Wasatch Advisors, Mr. Edgley was a principal, director of international research and portfolio manager for Chicago-based Liberty Wanger Asset Management, which managed the Acorn Funds. He was also a co-manager for the Acorn Foreign Forty Fund. Earlier, he worked in Hong Kong as a financial-services analyst for Societe Generale Asia/Crosby Securities and as

Mr. Edgley has a Master of Arts in Philosophy from the University of Sussex and a Master of Science in Social Psychology with Statistics from the London School of Economics, where he was awarded a Social Science Research Scholarship. He earned a Bachelor of Science with honors in Psychology from the University of Hertfordshire. He is also a CFA charterholder.

Laura Geritz is the Lead Portfolio Manager for the Wasatch Frontier Emerging Small Countries Fund. She has been a Portfolio Manager for the Wasatch Emerging Markets Small Countries Fund. She has been a Portfolio Manager for the Wasatch Emerging Markets Small Cap Fund since 2009 and a Portfolio Manager for the Wasatch International Opportunities Fund since 2011. She first joined Wasatch Advisors in 2006 as a Senior Equities Analyst on the international research team.

Before joining Wasatch Advisors, Ms. Geritz worked as a senior analyst for Mellon Corporation, where she made investment recommendations for two of the company’s small-cap growth funds. Prior to joining Mellon Corporation, she spent four years analyzing securities for various products at American Century Investments, where her stock selections represented approximately one-third of the assets held in each mid-cap growth portfolio.

Ms. Geritz graduated with honors from the University of Kansas with a Bachelor of Arts in Political Science and History. Later, she earned a Master’s Degree in East Asian Languages and Cultures. Before completing her Master’s Degree, she spent one year in Japan, where she translated and interpreted documents for the Board of Education and wrote and broadcast a weekly radio program in both English and Japanese. She is also a CFA charterholder and a member of the Denver Society of Financial Analysts.

Ajay Krishnan is the Lead Portfolio Manager for the Wasatch Emerging Markets Select and Emerging India Funds. He is also a Portfolio Manager for the Wasatch Global Opportunities Fund. He was a Portfolio Manager for the Ultra Growth Fund from 2000 to 2013. In addition, he was a Portfolio Manager for the World Innovators Fund from 2000 to 2007. He joined Wasatch Advisors as a Research Analyst in 1994. He was a Research Analyst on the Ultra Growth Fund prior to becoming a Portfolio Manager.

Mr. Krishnan earned a Master of Business Administration from Utah State University, where he also worked as a graduate assistant. He completed his undergraduate degree at Bombay University, earning a Bachelor of Science in Physics with a Minor in Mathematics.

Mr. Krishnan is a CFA charterholder and a member of the Salt Lake City Society of Financial Analysts. He specializes in analyzing the investment potential of fast- growing companies.

Ajay is a native of Mumbai, India and speaks Hindi and Malayalam. He enjoys traveling, reading, playing squash and road biking.

Andrey Kutuzov has been an Associate Portfolio Manager for the Wasatch Emerging Markets Small Cap Fund since 2014. He joined Wasatch Advisors in 2008 as a Senior Equities Analyst on the international research team. He also interned at Wasatch in 2007, while studying at the University of Wisconsin-Madison.

Prior to joining Wasatch Advisors, Mr. Kutuzov earned a Master of Business Administration from the University of Wisconsin’s Applied Security Analysis Program. While earning his degree, he was on a team that managed a student-run long/short equity portfolio. Prior to graduate school, he was a senior auditor at Deloitte, where his work included designing, performing, and supervising financial and internal control audits of commercial banks and investment companies under the U.S. GAAP as well as various international accounting standards.

Mr. Kutuzov also obtained a Bachelor’s and a Master’s of Accounting Degree at the University of Wisconsin- Madison. While pursuing his Master’s Degree, he taught an undergraduate course in Managerial Accounting. He is a Certified Public Accountant. He is also a CFA charterholder.

Andrey is a native Russian speaker. He enjoys traveling, sports and reading.

ABOUT WASATCH ADVISORS®

Wasatch Advisors is the investment manager to Wasatch Funds,® a family of no-load mutual funds, as well as to separately managed institutional and individual portfolios. Wasatch Advisors pursues a disciplined approach to investing, focused on bottom-up, fundamental analysis to develop a deep understanding of the investment potential of individual companies. In making investment decisions, the portfolio managers employ a uniquely collaborative process to leverage the knowledge and skill of the entire Wasatch Advisors research team.

Wasatch Advisors is an employee-owned investment advisor founded in 1975 and headquartered in Salt Lake City, Utah. The firm had $19.4 billion in assets under management as of March 31, 2014. Wasatch Advisors, Inc. is registered with the Securities and Exchange Commission under the Investment Advisers Act of 1940.

RISKS AND DISCLOSURES

In addition to the risks of investing in foreign securities in general, the risks of investing in the securities of companies domiciled in frontier and emerging- market countries include increased political or social instability, economies based on only a few industries, unstable currencies, runaway inflation, highly volatile securities markets, unpredictable shifts in policies relating to foreign investments, lack of protection for investors against parties that fail to complete transactions, and the potential for government seizure of assets or nationalization of companies.

Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds.

Being non-diversified, the Wasatch Emerging India, Wasatch Emerging Markets select and Wasatch Frontier Emerging small countries Funds can invest a larger portion of their assets in the stocks of a limited number of companies than diversified funds. Non-diversification increases the risk of loss to these Funds if the values of these securities decline.

An investor should consider investment objectives, risks, charges, and expenses carefully before investing. To obtain a prospectus, containing this and other information, visit www.WasatchFunds.com or call 800.551.1700. Please read it carefully before investing.

Information in this document regarding market or economic trends or the factors influencing historical or future performance reflects the opinions of management as of the date of this document.

These statements should not be relied upon for any other purpose. Past performance is no guarantee of future results, and there is no guarantee that the market forecasts discussed will be realized.

The investment objective of the Wasatch Emerging India, Wasatch Emerging Markets Select, Wasatch Emerging Markets Small Cap and Wasatch Frontier Emerging Small Countries Funds is long- term growth of capital.

CFA® is a trademark owned by CFA Institute.

ALPS Distributors, Inc. is not affiliated with Wasatch Advisors.

DEFINITIONS

alpha is a risk-adjusted measure of the so-called “excess return” on an investment. It is a common measure of assessing an active manager’s performance as it is the return in excess of a benchmark index or “risk-free” investment. The difference between the fair and actually expected rates of return on a stock is called the stock’s alpha.

correlation, in the financial world, is a statistical measure of how asset classes, securities, markets, or countries move in relation to each other.

debt-to-Gdp ratio is a measure of a country’s federal debt in relation to its gross domestic product (GDP). The higher the debt-to- GDP ratio, the less likely the country will be to pay back its debt, and the higher its risk of default.

Earnings growth is a measure of growth in a company’s net income over a specific period, often one year.

Gross domestic product (GDP) is a basic measure of a country’s economic performance and is the market value of all final goods and services made within the borders of a country in a year.

The price-to-earnings or P/E ratio is the price of a stock divided by its earnings per share.

Standard deviation is a statistical measure of the extent to which returns of an asset vary from its average.

Valuation is the process of determining the current worth of an asset or company.

The S&P 500 Index represents 500 of the United States’ largest stocks from a broad variety of industries.

The MscI Emerging Markets Index is a free float-adjusted mar- ket capitalization index designed to measure the equity market performance of emerging markets. The MscI Frontier Emerging Markets and MscI Frontier Markets indices are free float-adjusted market capitalization indices designed to measure equity market performance in the global frontier and emerging markets.

The MscI EaFE Index (Europe, Australasia, Far East Index) is designed to measure the equity market performance of developed markets, excluding the U.S. and Canada.

You cannot invest in these or any indices.

Source: MSCI. The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments, products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly dis- claims all warranties (including, without limitation, any warranties or originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages (http://www. msci.com).

[i] Huang, Wei, Eun, Cheol S. and Lai, Sandy, International Diversification with Large- and Small-Cap Stocks. Journal of Financial and Quantitative Analysis (JFQA), Forthcoming. Available at SSRN: http://ssrn.com/abstract=932961

[ii] Speidell, Lawrence, Frontier Market Equity Investing: Finding the Winners of the Future (May 2011). CFA Research Foundation of CFA Institute, ISBN 978-1-934667-36-1.

[iii] De Moor, Lieven and Sercu, Piet M. F. A., Country v. Sector Effects in Equity Returns: Are Emerging-Market Firms Just Small Firms? (May 2007). Available at SSRN: http://ssrn.com/ abstract=1025864 or http://dx.doi.org/10.2139/ssrn.1025864

© 2014 Wasatch Funds. All rights reserved. Wasatch Funds are distributed by ALPS Distributors, Inc. WAS003308 4/30/2015