“You’re Going to Need a Bigger Boat”: Alpha and Interest Rates

Caution has been the dominant sentiment among investors in recent times even as equities have continued to march along. But as the prospect of rising US interest rates becomes ever more real, Brooks Ritchey, senior managing director at K2 Advisors, Franklin Templeton Solutions, takes a look at how some individuals and institutions are changing their guarded approach. He says alternative investments could find increased interest among savvy investors as interest rates start to tick higher.

Every year during the dog days of summer, coinciding with Discovery channel’s immensely popular “Shark Week†programming, it seems that references to Steven Spielberg’s classic blockbuster movie Jaws abound. And this year was no different.

To me, Roy Scheider’s infamous line about needing a bigger boat (a brilliant ad lib by the way) allegorically brings to mind the current state of the markets.

While the market appeared relatively tranquil on the surface during the second quarter, an over-arching theme has been an increasing sense of trepidation—or uncertainty—related to potential threats lurking below.

Macroeconomic concerns, including geopolitical hot spots, China’s status, and whether or not global GDP growth can be sustained, all pose legitimate problems for market stability. As market volatility has increased we have seen signs of tension surface in recent weeks.

In our view, perhaps the most significant and pressing concern today, and certainly one the majority of market observers are keenly focused on, is the threat of rising interest rates in the United States. Given the current market environment, particularly as it relates to fixed income securities, rising interest rates could represent a macroeconomic risk for portfolios not suitably positioned. Despite the fact that a rise in interest rates is seen as an eventual certainty by market watchers, there are solutions for investors looking to weather the possible storm. We think seeking to inject some alpha—or manager-added value—into portfolios constructed largely on the basis of equity and bond exposure to general market conditions, could provide a better “boat.â€Â Â

I want to highlight the relationship I see between alpha–which we define as a risk-adjusted measure of the value that an active portfolio manager adds to or subtracts from a portfolio’s return—and interest rates, and why in my view a portfolio constructed with alpha components can potentially prove beneficial when the inevitable rate rise surfaces. There are several other points with regard to alpha that I think are worth noting.

Alpha is a measurable and tangible market by-product. It is the noise inefficiency residual that shadows the market signal, and it creates a value ‘song’ that can be captured and appreciated by market participants with discerning ears…and the right equipment.

Another observation I would like to make relates to alpha and its cyclical nature. Alpha, like many other aspects of the market, is a cyclical phenomenon that waxes and wanes with macroeconomic environments, demographics and investor behaviors. Alpha can be stronger on average in some economic cycles or environments, such as periods with higher interest rates, and weaker in others.

The last point I would like to make relates to alpha and the strong relationship I have observed it has had with interest rates.

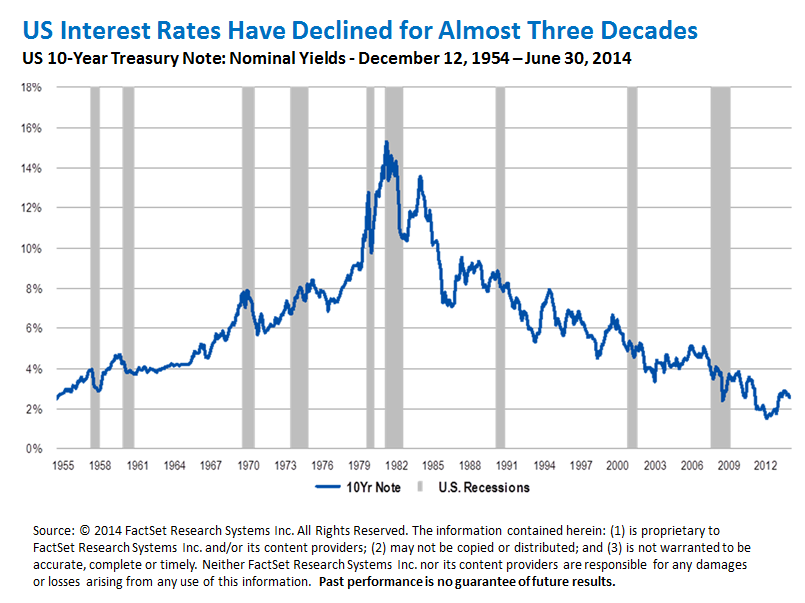

I should note that most financial market observers believe the US Federal Reserve will start to raise interest rates at some point in the not-too-distant future, perhaps as early as the second half of 2015. Fixed income has enjoyed a bull market rally spanning close to 30 years now, give or take a few outliers here and there such as 1994. US interest rates have steadily declined from the mid-teens in the late 1970s to single digits today.

This inexorable decline and associated increase in bond prices has helped protect many investors against rate and duration1Â risk for an extended period. But it seems inevitable to us that this long-term trend of lower rates and higher bond prices will likely eventually reverse, and not preparing for this shift appropriately will leave some boats taking on substantial water.

With rising rates being the likely course ahead, we see many institutions seeking to reduce  these risks by looking to alternative investment funds that use alternative strategies, where portfolios can be structured that seek to soften interest rate and duration exposure.

We believe alternative strategies used within a retail mutual fund can be particularly attractive in a rising rate environment because they can be structured with the goal of providing both potential protection, and also potential gain, from rising rates.

Alternative investments cover a varied set of asset classes and strategies that go beyond traditional stocks and bonds. Alternative investment asset classes include real estate, real assets (e.g., commodities, infrastructure) and private equity, while alternative strategies primarily consist of hedge strategies. Hedge strategies typically have the ability to utilize short positions (i.e. seeking to profit on a decline in value of an individual security or index) in contrast to traditional mutual fund strategies which typically permit only long positions.

AÂ hedge fund is a pooled investment fund, usually a private partnership, that seeks to maximize returns using a broad range of strategies, including unconventional and illiquid investments.

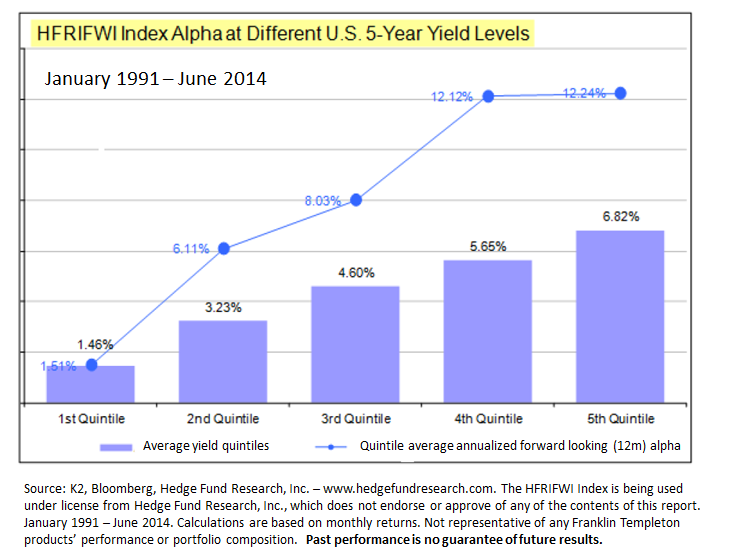

When interest rates go up bonds will naturally suffer somewhat, as bond prices trade inversely to yield. In my view, equities generally could probably weather the environment, or at least tread water. However, I think an alpha-seeking approach—use of hedging strategies, for example—has more potential to outperform in a rising-rate environment. Statistical analysis of the historical relationship between interest rates and alpha support this. The graph below illustrates the historic relationship between alpha levels on the Hedge Fund Research Index Fund Weighted Composite Index (HFRI FWI)2 and US five-year Treasury yield levels.

As you can see, when interest rate level averages over the last 23 years have been at their lowest, represented by the first quintile bar on the left, average alpha levels have also been at their lowest.

Clearly, higher nominal yields of government bonds, such as US five-year Treasuries, have on average historically corresponded with increased average annualized hedge fund alpha capture as well. In my experience, the vast majority of alternative investment funds that use hedge strategies are defensive with respect to interest rate risk, while some macro managers see it as a speculative opportunity.

A similar dynamic occurs for companies and countries when rates rise. The result is a pressure on profit margins, and the variances in profit margin pressures are reflected in the variance in security performance. The inefficiencies created by these variances promote alpha potential.

I believe the implication of rising rates for individual and institutional portfolios, particularly for constrained or traditional fixed-income investments, could be troublesome as they could be confronted with either diminishing returns with small losses or potentially significant losses—depending upon the magnitude and velocity of the rate rise. Alternative strategies, we believe, can potentially offer a better boat to help navigate this interest-rate sea change.

As We See it: An Outlook for the Rest of 2014

We believe the rest of 2014 could be more interesting than what we’ve seen so far, as markets work through uncertainties and if global growth trajectories improve and divergences materialize in central bank policy expectations.

The somewhat uneven path of the US recovery thus far in 2014 has remained a problem for central banks globally, as many had hoped the US rate normalization would be further along and that the US dollar would be higher.

The lack of a rise in US rates has been the source of some idiosyncratic market activity in recent months, and we believe this environment could persist for some time.

The strong results from equity markets over the second quarter have been encouraging to us. Investors have rightly cheered their gains, but in our view the time for caution is just when things appear to look best. Market volatility had declined to significantly low levels in the second quarter, which we believe may signal more possible storms ahead. In addition, we remain vigilant with regard to high yield corporate debt, as the market reconsiders the current low yields relative to historic levels.

Events in Iraq, Ukraine and, recently, Israel, still warrant close attention, in our view, as more downside volatility could be triggered given the impact the regional strife may have on global energy prices and investor sentiment.

We will be paying close attention to developments in Asia and the Middle East regions. The US Federal Reserve again pledged that it would continue with its bond purchase “taper†while maintaining an accommodative stance with regard to rates. We anticipate the central bank’s policies will likely remain supportive for risk assets for the foreseeable future.

If you’ve been inspired by Brooks’ shark-themed approach, be sure to check out this Behavioral Finance for Everyday Investors video which offers some insight on how the toothy creatures can help explain the concept of availability bias… with extra bite:

Brooks Ritchey’s comments, opinions and analyses are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

What Are the Risks?

All investments involve risks, including possible loss of principal. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Bond prices generally move in the opposite direction of interest rates. Changes in the financial strength of a bond issuer or in a bond’s credit rating may affect its value. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline.

Investment in hedge funds is a speculative investment, entails significant risk and should not be considered a complete investment program. An investment in hedge funds provides for only limited liquidity and is suitable only for persons who can afford to lose the entire amount of their investment. There can be no assurance that the investment strategies employed by hedge fund managers will be successful.

Investment in these types of hedge fund strategies is subject to those market risks common to entities investing in all types of securities, including market volatility.

1. Duration is a measure of the sensitivity of the price (the value of principal) of a fixed-income investment to a change in interest rates. Duration is expressed as a number of years.

2. Source:Â HFRI Fund of Funds Composite Index:Â Funds of Funds invest with multiple managers through funds or managed accounts. The strategy designs a diversified portfolio of managers with the objective of significantly lowering the risk (volatility) of investing with an individual manager. The Fund of Funds manager has discretion in choosing which strategies to invest in for the portfolio. A manager may allocate funds to numerous managers within a single strategy, or with numerous managers in multiple strategies.

© Franklin Templeton Investments