Treesdale Partners, portfolio manager of the AdvisorShares Gartman Gold/Euro ETF (GEUR), AdvisorShares Gartman Gold/British Pound ETF (GGBP), AdvisorShares Gartman Gold/Yen ETF (GYEN) and AdvisorShares International Gold ETF (GLDE), share their thoughts about the gold space.

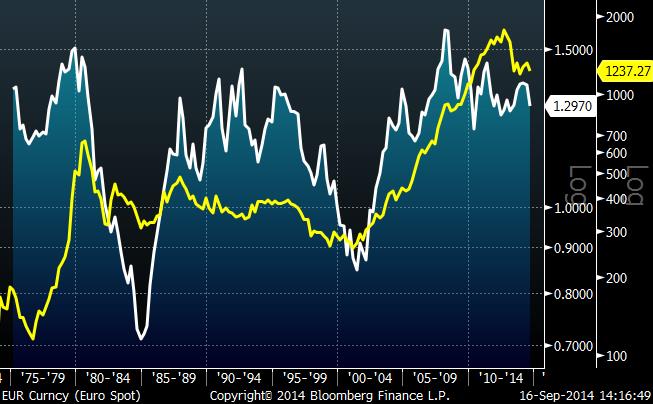

Notes: Yellow - Gold prince in US Dollar; White – Euro/US Dollar FX rate. A higher FX rate indicates a weaker dollar. Past performance is not indicative of future performance

We continue on the theme gold and the dollar but this week take a short look at their “long-term” relationship and relative movement over the last 40 years. In particular we focus on the period post the ending of the Bretton-Woods agreement by the Nixon administration in 1971 (the so-called “Nixon Shock”) which terminated dollar convertibility to gold and thus established the dollar as a fiat currency. In the chart the yellow line is the gold price expressed in dollars per ounce and the white line is our proxy for the value of the dollar, the euro/USD FX rate, with a higher FX rate representing a weaker dollar. Note that both time series are plotted on a log scale to better reflect the large moves in both time series over the 40 year period. Of course the euro did not exist prior to January 1st 1999 so prior to this date the value of the German mark, expressed in euro at its fixed conversion rate is used to imply the euro/USD FX rate.

In our most recent weekly manager notes we discussed in detail the strong, historical but inverse relationship between the dollar and the gold price in dollars; when the dollar has been weak on currency markets, the gold price in dollars has tended to be strong. The essential point we wished to emphasize was the inherent nature of gold as a (physical) currency whose value is often expressed relative to other currencies. Most commonly the gold price is expressed in “dollars per ounce” i.e. how many dollars would an investor require to purchase an ounce of gold. When thought of in these terms the inverse relationship between gold and the currency in which it is financed becomes self evident; as the dollar weakens, all things being equal, an investor will require more dollars to purchase that same ounce of gold. Of course in these discussion pieces we focused on shorter time periods but a long period must by definition be the sum of a series of shorter time periods and as such it should not be surprising that over longer time periods, the inverse relationship between gold in dollars and the value of the dollar is still strongly observable.

Returning to the chart above, it can be seen how the stratospheric rise in the value of gold in dollar terms, in particular over the last 14 years, has been in an environment of a sharply weakening dollar – an investor today requires over 450% more dollars to buy an ounce gold compared to its value in 2001! The extent of the weakening in the dollar is often a surprise to many US investors but it is evident that it has been a significant factor in the strong returns investors have earned from holding non-dollar assets including gold over this period. And it is this long-term trend in the dollar on which we believe US investors should start to focus. Despite its recent strength, the dollar both in terms of the euro/usd FX rate and the USDX Intercontinental Exchange Trade Weighted Dollar Index is still close to its lows experienced post the breakup of the Bretton-Woods agreement. But following a period of strongly synchronized central bank policy across the globe since the onset of the credit crisis we now note the stark divergence in monetary policy between the US Federal Reserve which stands poised to normalize monetary policy and other major central banks which appear ready to extend unconventional policy measures as their economies teeter on the edge of slipping back into contraction. Should this divergence persist for any significant period of time this would be expected to be strongly beneficial for the dollar and might be a driving factor that leads to a new cycle of dollar strength over the coming years.

As investors we still favor owning gold as a valuable asset for portfolio diversification but remain concerned about the potential impact a strengthening dollar might have on the price of gold in dollars. And to that end we favor owning gold financed in non-dollar currencies thereby avoiding short exposure to a potentially resurgent dollar. And for investors that prefer not to have gold exposure financed in a single currency, albeit non-dollars, we would recommend a diversified approach financing a gold investment with a diversified basket of major currencies.