September 2014

Following an explosive re-rating in 2013 that saw the Tokyo Stock Price Index (TOPIX) gain approximately 51% (in local currency terms), we have seen a reversal of Japan’s equity markets so far this year. As of August, the TOPIX year-to-date was down slightly, underperforming the U.S. and other Asian markets. This has led some investors to question the efficacy of “Abenomics.” With the recent announcement of Prime Minister Shinzo Abe’s revamped growth strategy, I believe it’s a good time to reassess the impact of his economic plan, and consider what the future may hold.

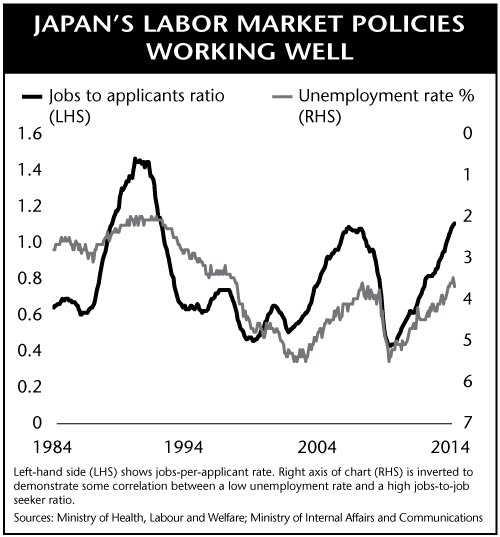

There are literally hundreds of components that comprise Abenomics but one successful area has been job creation. Since it took over at the end of 2012, the Abe administration has created more than 1 million new jobs, with more likely to come given the robust growth in job offers. The job offer-to-applicant ratio recently hit a 22-year high while the unemployment rate has concurrently declined. Discouraged job seekers who had previously left the labor pool have begun to re-enter the workforce. Critics often note that many of these jobs are at the low end of the wage curve in primarily part-time jobs but for the incremental worker and the economy as a whole, a job at a low wage is better than no wage at all. Supported in part by these job gains, corporate earnings have remained robust. Earnings for the April–June quarter—the quarter most affected by the reactionary fall in consumption following Japan’s April sales tax hike—have come out ahead of both company guidance and market expectations. Granted, guidance and market expectations were quite conservative to begin with, but quarterly earnings growth still managed to outpace the S&P 500 Index. The bottom-up picture appears fine as better earnings and share price underperformance have made valuations in Japan that much cheaper.

Meanwhile, over the past year, inflation has turned higher. At the end of 2012, Japan’s consumer price index excluding fresh food—the Bank of Japan’s preferred inflation benchmark—was -0.2%. But by the end of 2013, that had advanced to +1.3%, quite a big change in just 12 months. I believe this transition to an inflationary environment is slowly starting to change corporate mindsets. In aggregate, Japanese companies have been sitting on piles of cash, which would lose value in real terms in an inflationary world. Share buybacks announced so far in 2014 have already surpassed 2013. We’ve seen companies raise dividends and more have started to set specific dividend payout ratios in lieu of “stable dividends” (i.e. investors get whatever companies feel like paying). Phrases like “return on equity target” and “increasing capital efficiency” have become more common during conversations with management. The direct trigger of these shareholder returns may be stronger earnings, but corporate managers seem to be more acutely aware of the risk of holding excess cash in an inflationary environment.

At the same time, measures to strengthen corporate governance are being put forth. The recently introduced Japanese Stewardship Code, adopted by more than 100 domestic and foreign firms, requires institutional investors to engage more actively with company management for the benefit of their investors. Though this may sound very primitive to U.S. or European investors, domestic Japanese money managers, who have rarely engaged deeply with portfolio companies, will now have to reconsider their approach to even basic things like proxy voting. By the middle of next year, Prime Minister Abe intends to establish a corporate governance code that will require, amongst other things, stronger oversight by independent directors. Amid rising external pressure, the percentage of companies with independent directors listed on the Tokyo Stock Exchange 1st Section has increased to 61% this year from 47% in 2013. This should be particularly impactful for banks and insurance companies that own large amounts of equity for “business relationship purposes” as these holdings will be subject to even more scrutiny. Of course, better governance is no guarantee of success but it should, on average, improve the quality of decision-making that goes on inside Japanese board rooms.

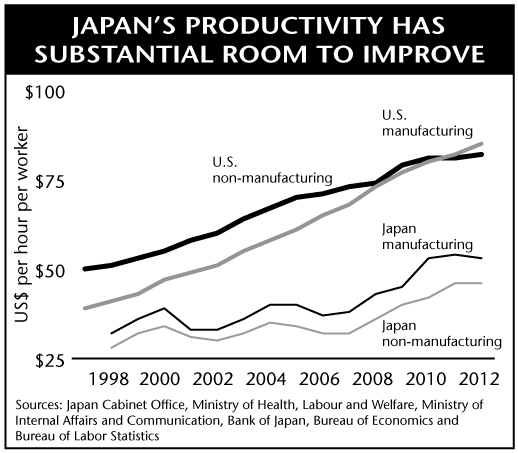

The potential for productivity enhancement induced by better corporate governance is enormous. In fact, I believe that productivity improvements will be the most important driver of growth for Japan going forward. Currently, productivity of Japan’s manufacturing and non-manufacturing sectors, as measured by output per worker per hour, remains far lower than the U.S., as highlighted in the chart below. Why? Pretty simple: over a decade of deflation caused by oversupply. There are many sectors of Japan Inc. that remain simply too fragmented and companies have little or no pricing power. Such fragmentation causes duplication of capacity and development costs, while keeping competition unnecessarily high, lowering selling prices and profitability. For example, let’s take the diaper industry. In the U.S., the two leading companies dominate with a combined market share of roughly 80% in a growing market. In Japan, a country where the sales of adult diapers has surpassed that of infant diapers, there are still four domestic producers competing with each other and foreign brands over a shrinking pie. For some of these players, diapers aren't even the core business but they continue to hang on, which leads to low industry profitability.

Japan needs consolidation for more meaningful improvement in productivity. One example of consolidation that may serve as a benchmark is Japan’s non-life insurance sector. Over the past decade, Japan’s non-life insurance industry has consolidated into three groups that control 94% of total revenue. Previously, the industry had more than a dozen players and was locked in stiff price competition as each player sought to grab a larger portion of the overall insurance pie. However, revenues began to fall in the early 2000s while insurance claims increased due to the rise in accidents and natural disasters. As a result, many firms fell into a loss, prompting several waves of consolidation. During that process, insurers streamlined operations and removed duplicate spending on IT systems to rationalize costs. More importantly, they have been able to raise prices. Since 2009, non-life insurers have raised prices every year, resulting in higher overall premium revenues for the industry and improved profitability. Sure enough, Japanese non-life insurers pay some of the highest wages in the country.

In addition to consolidation, the emergence of Internet-based services with disruptive business models can also make an impact on productivity. These new companies don’t carry the legacy costs that plague many incumbent players. Through the application of technology, we've seen companies in fields such as health care, e-commerce and content creation take market share away from their brick-and-mortar competitors. Recently, we’re starting to see evidence that risk-taking is creeping up as Japan’s entrepreneurs attract more capital. Through June, Japanese start-ups attracted 32% more investment from venture capital firms compared to last year. Despite this year’s stagnant markets, investor appetite for new IPOs has remained resilient and venture capital funds seek to seize this opportunity. A government initiative to allow state-owned universities to set up venture capital funds that will invest in the commercialization of innovative research is also being set forth.

Improving productivity in Japan will involve making many difficult choices. For many years, managers have opted to kick the can down the road. But there isn’t much road left anymore. With a shift to inflation, an impending labor shortage, ever-strengthening demand for higher returns from shareholders and the introduction of disruptive forces, the pressure is mounting to make those tough decisions. These developments have me feeling more optimistic over the prospects for Japanese companies over the medium term.

Kenichi Amaki

Portfolio Manager

Matthews Asia

The views and information discussed in this article are as of the date of publication, are subject to change and may not reflect the writers' current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of any securities or any sectors mentioned herein.

The subject matter contained herein has been derived from several sources believed to be reliable and accurate at the time of compilation. Matthews International Capital Management, LLC does not accept any liability for losses either direct or consequential caused by the use of this information.