After a strong summer rally, the first two weeks of September have not been kind to US financial markets, with both stock and bond markets generating negative returns. In the month to date, ten year Treasury yields have risen twenty five basis points to 2.60%, the highest such level since the first week of July. Though the rise in interest rates has been fairly consistent across all points along the yield curve, market reaction and trading volumes have been fairly orderly. With geopolitical events abating somewhat last week (for now), interest rate risk and fears of a material change in Federal Reserve policy has returned as the number one concern in US financial markets. The generous yield differential between US benchmark yields relative to Europe and Japan seems to be providing a degree of order during the recent sell off.

Despite last week’s retail sales figure recording its best level in four months and forcing many economists to adjust higher their 3rd quarter GDP estimate, risk markets—namely equity and high yield—surprisingly sold off. We have long opined that risk assets were the biggest beneficiary of unprecedented stimulus by the Fed. With quantitative easing scheduled to end next month, and with the next move by the Federal Open Market Committee in interest rate policy to be a rise in rates, we suspect risk assets may well exhibit more volatility relative to high grade assets over the final months of 2014.

Volatility is expected to remain elevated this week, with the FOMC beginning a two day meeting Tuesday, and the Scottish separation vote scheduled for Thursday. Fundamentally, the latest data on inflation will be released as well, with Producer Price Index (PPI) on Tuesday and Consumer Price Index (CPI) on Wednesday. With inflation expected to remain subdued, and growth still stubbornly inconsistent, Castleton does not share the perspective that the Federal Reserve will choose this week’s meeting as a means to alter current thinking on the timing and pace of future interest rate policy.

Weekly Change: 10Y Treasury Yields vs. 10Y AAA MMD

Source: Bloomberg, Thomson Reuters and Castleton Partners

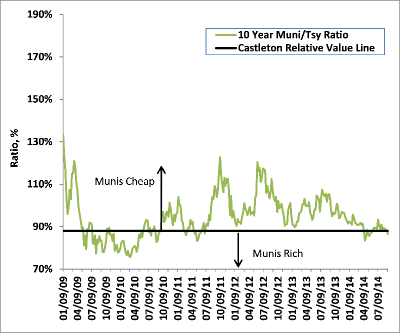

Ratio of 10Y Muni Yield to 10Y Treasury Yield

Source: Bloomberg, Thomson Reuters and Castleton Partners

Tax-Exempt

Taking direction from the recent rise in Treasury rates, municipal yields followed suit last week. At 2.26%, the benchmark 10 year muni rate has now risen 19 basis points since August, outperforming its taxable counterparts along the way. The 10 year Muni/ Treasury ratio now rests at 87%, the lowest such level since May. We expect municipals to continue their relative outperformance as fund flows and investor demand continue to favor the superior tax adjusted yields of the asset class. With nearly $500 million of new subscriptions to mutual funds last week, munis have now received positive fund flows for nine consecutive weeks.

Last week’s limited offering of new debt was quickly absorbed, as the ample cash on the sidelines and lack of recent supply favored new issuance over a thin secondary market. This week, supply stands at nearly $6 billion—hardly robust, but nearly double the previous week’s offering. The largest offerings are three credits which Castleton views as favorable and we anticipate strong interest: $481 million for San Francisco Airport (A1/A); $350 million Massachusetts G. O. (AA2/AA+); $300 million University of Pittsburgh Medical Center (AA3/A+).

AAA Municipal Market Data (MMD) Yield Curve

Source: Thomson Reuters

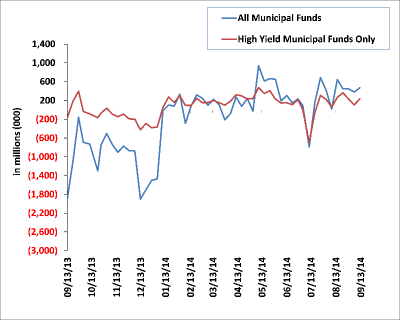

Weekly Municipal Mutual Fund Flow Data

Source: Lipper AMG Data

Taxable

Surprisingly, high grade spreads were relatively stable last week, despite a sharp rise in benchmark US interest rates. We find this somewhat concerning, as the historical negative correlation between spreads and sharp moves in yields appears to have broken down. We have long viewed high grade spreads as “expensive”, believing the lack of yield relative to Treasury rates would fail to provide enough cushion should interest rates rise. Should the recent rate selloff continue, we suspect spreads would start to underperform as retail investors withdraw from mutual funds, reacting to negative performance.

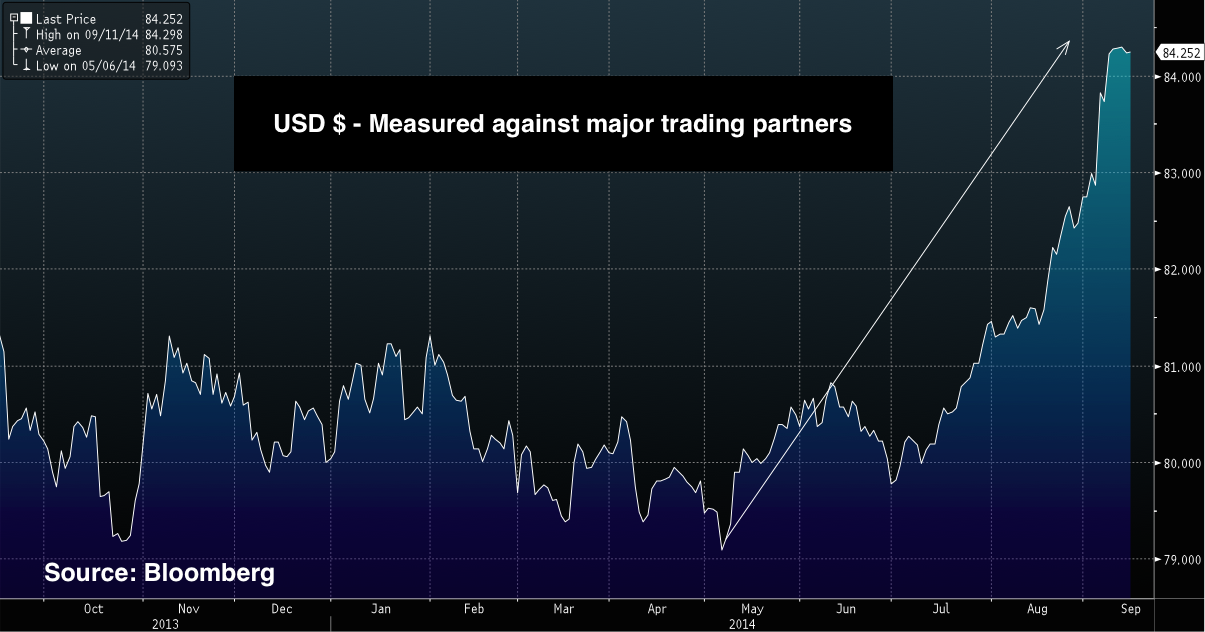

Another variable that we continue to measure in investment grade corporates is the recent rise in the US dollar relative to our major trading partners. US corporations, particularly those that rely heavily on overseas activity, will no doubt face some earnings pressure from the recent dollar strength, as well as from increased competition at home from foreign companies.

Supply—and the abundance of it—continues to increase among investment grade issuers. With 2015 expected to bring about a change in interest rate policy, many corporations are taking advantage of anemic yields now to lock in attractive financing rates. Nearly $40 billion of new debt was priced last week, with financials again a major contributor.

© 2014 Castleton Partners, LLC. All rights reserved.

THE FOLLOWING NOTES AND DISCLOSURES ARE AN INTEGRAL PART OF THIS REPORT: Past performance is not a guarantee of future results. Different investments involve varying degrees of risk, including the risk of illiquidity and the risk that you could lose part or all of your investment. There can be no assurance that the future performance of any specific investment, investment strategy, or product (including those discussed herein or recommended or undertaken by Castleton Partners, LLC) will be profitable, equal any corresponding indicated historical performance, be suitable for your portfolio or individual situation, or prove successful. Charts, graphs and indices are included herein only for reference and do not constitute forecasts of the past or predicted future performance of any investment. Indices are not investments. Due to changing market conditions and other factors the content herein may no longer reflect Castleton Partners, LLC’s current opinions or positions. Nothing discussed herein is or is intended as tax, legal, accounting or personalized investment advice from Castleton Partners, LLC. Should you have any questions regarding the applicability of any specific issue discussed herein we encourage you to consult competent advisers of your choosing. Nothing herein is or is intended as an offer to sell or a solicitation of offers to buy any security. Castleton Partners, LLC’s current written disclosure statement including discussion of our advisory services and fees is available upon request.