Historical Trends Offer Perspective, Not Predictions

The cyclicality of the stock market seems to be something most investors accept even if they don’t fully understand it. Certain seasonal adages for stocks will doubtless sound familiar. "As goes January, so goes the year" seems to be repeated as a rule sometime in early February, while "Sell in May and go away" reflects not only the conditioned expectation of summer weakness, but also a preference for sayings that rhyme. This helps explain why "Buy in November . . ." never really caught on, even though that’s the complementary subsequent action you’d take if you expected weakness in stocks from April to October.

Perhaps the proliferation of these sayings partially explains why the actual timing of cyclical shifts can catch some investors off guard. It’s important to remember these sayings reflect historical experiences that may or may not hold under current circumstances. For example, "sell in May" was widely discussed ahead of time this year, however (and not too surprisingly) stocks moved higher through that period and didn’t see a substantial selloff until late July. When a historical pattern becomes too widely known, its usefulness may actually be diminished.

Instead of living by the adage and attempting to time the markets, we track historical patterns as a risk management exercise within our overall weight-of-the-evidence framework. And in that light, history may provide some valuable lessons.

Donkeys, Elephants and Bulls?

In the current environment, some of the most intriguing historical patterns to watch stem from the four-year Presidential election cycle. Without getting too far into the “why,” it’s worth noting that mid-term election years represent the furthest point away from presidential elections. Stimulus provided in advance of the previous election has typically worn off and the incumbent has usually not yet focused on efforts to assure re-election (or, in the current scenario, one party’s control of the White House). As such, mid-term election years tend to be the weakest for stocks during the four years of a president’s term. That weakness is usually limited to the months just ahead of the elections, and is often just an amplification of the annual “sell in May” phenomenon discussed previously. So history would lead us to anticipate elevated market risk on our way into the voting booth.

Another interesting historical tidbit: Midterm election years have been the only years (since 1979) where small-caps, on average, have lost ground to large-caps, and much of this weakness tends to show in the six months ahead of elections. While stocks overall might not conform to prospective seasonal patterns, the behavior of small-caps so far in 2014 has been largely in line with election-year trends. This could be a good sign both for small-caps relative to large-caps and for stocks as a whole, as the passage of mid-term elections often represents a turning point in seasonal patterns. Historically stocks tend to bottom as the results of elections become clear. If this holds true in 2014, seasonal headwinds could become tailwinds as the fourth quarter unfolds.

Historical Numerology

Additional good news might be read in the pattern of stock returns over the course of a decade. Based on data from Ned Davis Research, years ending in “5” have seen the best average returns and, since the final decade of the 1800s, the S&P 500 has been up every time the calendar shows a year ending in “5.” The average return in these years has been more than 22% - dwarfing the returns of the next best group (years ending in “8” had average annual returns of 14%, but posted a nearly 40% decline the last time around). The worst performing years of a decade have historically ended in “7” and “0,” both of which boast negative cumulative returns and together have posted gains less than 50% of the time.

Looking just at historical and seasonal patterns, the current message would be one of caution with anticipation of perhaps an improving market environment later this year and into the next. But for specific recommendations, we must look much more closely at the here and now.

Not Last Century’s Tech Sector

Investors still harboring mistrust for the Technology sector post the bursting of the NASDAQ bubble in 2000 may be well-served to consider increasing exposure there now. The current Technology sector is much more fundamentally sound and decidedly different than the sector bearing that name a decade and a half ago. Valuations are more reasonable and, better yet, based on actual earnings. As of late last year, the market cap for the top-ten companies in the NASDAQ was nearly 20% below that seen near the bubble’s peak, while earnings for those companies were more than three times as great.

In many ways, today’s Technology sector looks more like the Industrial sector – both in terms of its financial profile and its increasingly widespread importance on our daily lives. The companies are more well-established and some even pay dividends.

This isn’t to say the Tech sector doesn’t have its risks, and certainly any exposure should be considered in the context of a broader asset allocation plan, but cyclical and secular opportunities certainly exist.

About the Author

William A. Delwiche, CMT, CFA, is Baird’s Investment Strategist and is a member of the Investment Policy Committee. Since 2004, he has also been the co-manager of Baird's ETF-based ALIGN Tactical Portfolios. Before joining Baird in 1999, he worked as a researcher at the Committee for Economic Development, a Washington, D.C., pro-business think tank.

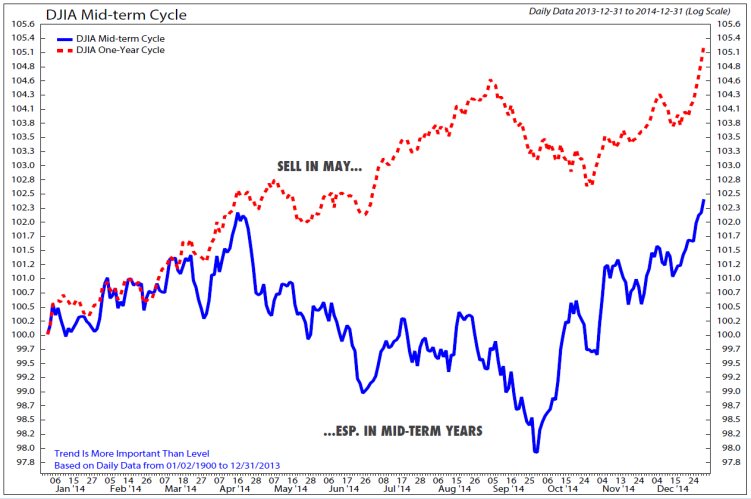

Dow Jones Industrial Average Midterm Cycle

The chart below, based on daily data from January 1900 to December 2013, shows there may be some truth to the old adage about selling stocks in the springtime – particularly in mid-term election years.

DJIA One-Year Cycle

DJIA Midterm Cycle (based on data from 1/1900-12/2013)

Source: Ned Davis Research Group, May 2014