In typical fashion, last week’s European Central Bank (ECB) announcements found a way to bury the lede. The deposit rate cut to -20 basis points from -10 basis points was characterized as a “technical adjustment,” and the asset purchase program, while important, lacked a specific quantitative target—forcing investors to infer a rough figure from Mario Draghi’s comments in the press conference. Nevertheless, the steps taken by the ECB were critical for the outlook because they revealed something about the central bank’s reaction function—that policymakers will deploy unconventional tools to prevent inflation expectations from falling too far.

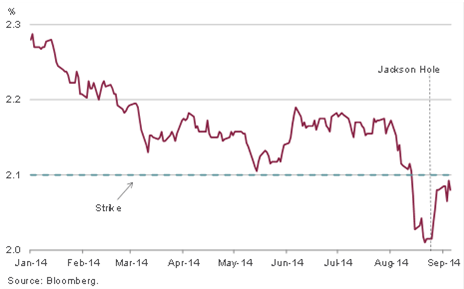

The financial market analogy that comes to mind is of interest rate caps and floors. A cap is a derivative instrument in which the seller pays a buyer if interest rates exceed a certain threshold. A floor works in the opposite way: the seller pays a buyer if interest rates fall below a certain threshold. This week’s ECB meeting—and comments from the Jackson Hole conference preceding it—can be thought of as revealing a “Draghi Floor.” The only substantive change between the August and September ECB meetings was that longer term inflation expectations fell sharply, and this shift prompted a meaningful easing from the governing council. Thus, investors should infer the existence of a “Draghi Floor” on inflation expectations—struck at around 2.1% for 5y5y inflation swaps (Exhibit 1). Below this level the ECB will act.

Exhibit 1: 5y5y eurozone inflation swap rate

So has the ECB done enough? Perhaps not. Unlike the Fed’s use of unconventional monetary policy over the last six years, there was no “shock and awe” moment—something definitively convincing investors that we’ll see a sustained recovery in the eurozone. We suspect that it will take better growth and inflation data, more monetary easing, or both, to re-anchor inflation expectations and restore confidence. But we now know the strike rate for the Draghi Floor, and this marks an important turning point for markets. The economy may muddle through a while longer, but deflation risks will be met with more monetary easing—limiting the odds of Japanification and the upside for bond prices.

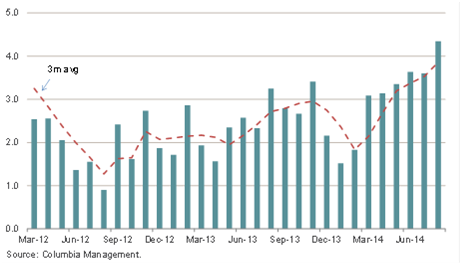

Meanwhile, the U.S. economy continues to outperform expectations. While the August employment report was mildly disappointing compared to expectations, other activity indicators showed signs of further acceleration (e.g. auto sales, services ISM). Our proprietary U.S. activity measure jumped to an above-4% growth rate for August, its best showing since early 2010. We doubt this pace of expansion will be sustained, but the long streak of above trend growth suggests we’ve seen more than a temporary rebound from cold winter weather—the U.S. expansion has shifted into high gear.

Exhibit 2: U.S. activity indicator

Aside from the activity data, there were two notable developments related to the Fed policy outlook. First, senior Fed staffers published an lengthy research paper arguing that most of the decline in labor force participation since 2007 can be explained by structural (as opposed to cyclical) factors. This result is consistent with the CBO, the White House, our own research, and even Janet Yellen’s comments at the Jackson Hole conference. Thus, the labor force participation rate debate is now more or less settled in favor of the “mostly structural” view.

Second, a speech from the new President of the Cleveland Fed, Loretta Mester, hinted at a possible change in forward guidance at the September 16-17 FOMC meeting. President Mester participates on the Fed’s subcommittee for communications, along with Governors Fischer and Powell and President Williams. Her prepared remarks noted bluntly: “With the end of the program [QE] nearing, I believe it is again time for the Committee to reformulate its forward guidance.” She added in Q&A that the current forward guidance looks “stale” (according to Bloomberg). Her comments deserve only limited weight for now, but at the very least they indicate a change will be on the table at the meeting.

Overall this week’s news did little to change our forecasts for Fed policy, but it raised our convictions a bit. We continue to expect the Fed’s first rate hike in June 2015 or a little sooner, and a steady pace of increases thereafter. At the upcoming meeting the committee will undoubtedly trim its bond buying program again, and we see 50/50 odds that policymakers will revise the key forward guidance phrase in the statement: “it likely will be appropriate to maintain the current target range for the federal funds rate for a considerable time after the asset purchase program ends” (emphasis added). Exceptionally strong results from next week’s data—particularly the retail sales and Quarterly Services Survey (QSS) reports—could push the odds of a change above 50%. Lastly, look for Fed officials to modestly trim their forecasts for the unemployment rate and nudge up their forecasts for the funds rate in the Summary of Economic Projections (SEP). New projections for 2017 should show the funds rate returning to equilibrium, which most Fed officials view as 3.75%.

Disclosure

The views expressed are as of 9/8/14, may change as market or other conditions change, and may differ from views expressed by other Columbia Management Investment Advisers, LLC (CMIA) associates or affiliates. Actual investments or investment decisions made by CMIA and its affiliates, whether for its own account or on behalf of clients, will not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not account for individual investor circumstances. Investment decisions should always be made based on an investor's specific financial needs, objectives, goals, time horizon, and risk tolerance. Asset classes described may not be suitable for all investors. Past performance does not guarantee future results and no forecast should be considered a guarantee either. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or that the forecasts are accurate.

This material may contain certain statements that may be deemed forward-looking. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those discussed. There is no guarantee that investment objectives will be achieved or that any particular investment will be profitable.

Investment products are not federally or FDIC-insured, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.

Securities products offered through Columbia Management Investment Distributors, Inc., member FINRA. Advisory services provided by Columbia Management Investment Advisers, LLC.

© 2014 Columbia Management Investment Distributors, Inc. All rights reserved.

1008265