Key Points

- The U.S. stock market continues to reach new highs but sentiment is extended and we are entering a period that has historically seen weakness. We believe the ultimate trend is higher, but bumps could get more pronounced in the near future.

- The U.S. economy is improving, with data suggesting self-supporting expansion is taking hold. Whether this means accelerated Fed interest rate hikes is being closely watched, while midterm elections often inject some more uncertainty into the market.

- The European Central Bank (ECB) finally acted, but structural issues and lack of demand remain problems. Japan also faces longer-term problems but near-term upside possibilities remain, while both China and the broader emerging markets look attractive for international allocations.

Stocks in the United States continue to move higher, with new records becoming a regular occurrence; supported by strengthening economic and earnings growth, fair valuations, and a still-accommodative Federal Reserve. But there are risks. A growing concern comes from across the pond as the European economy has weakened, with high unemployment, deflation concerns, and confidence being further dented by Russian sanctions. The continued strength in the U.S. stock market and economy is encouraging, and divergences are likely to remain heightened, but according to our friends at Cornerstone Macro Research, roughly 20% of U.S. company earnings come from the eurozone. We are encouraged by the recent actions by the European Central Bank (ECB), detailed below, but remain skeptical that without more substantial structural reforms, sustainable economic growth can be achieved.

More local risks are also growing.  Several key investor sentiment indexes have again moved into territory depicting extreme optimism. Additionally, September has historically been the worst performing month for U.S. stocks, with Bespoke Investment Group reporting that since 1928 the S&P 500’s average September return has been -1.07%, with only 45% of Septembers showing a positive return. Combine that with a September Fed meeting, continuing geopolitical uncertainty, and upcoming midterm elections, and you have the ingredients for a pullback.Â

Despite these risks, we remain bullish on the U.S. stock market and would view a decent sized pullback in a positive light as it could allow sentiment to correct and the market to catch its breath. We believe such an event would be a buying opportunity but warn investors that if they can’t handle a quick selloff in their stock portfolio, they may need to rethink their overall asset allocation.

Economy heating up

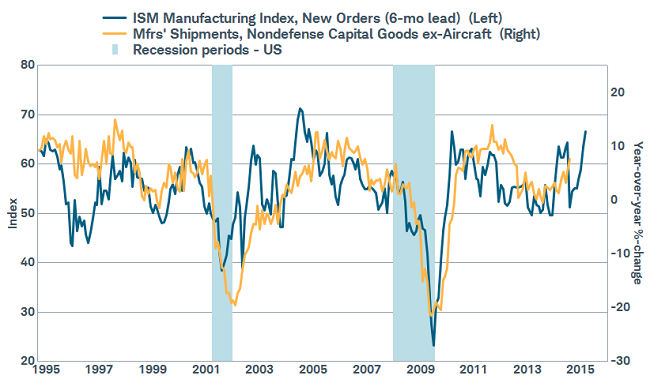

The recent round of economic releases have shown an unambiguous picture of a strengthening U.S. economy, helping to support our bullish view on stocks and showing signs of a self-sustaining expansion. The Job Opening and Labor Turnover Survey (JOLTS) showed a spike in job openings and an increase in the “quit rate;†the Philly Fed Business Outlook Survey posted the highest reading since 2010 for the current activity index; existing home sales and housing starts rose; and consumer confidence continues to improve. Adding to the positive tone, the Institute for Supply Management’s (ISM) Manufacturing Index rose to 59.0, which was the best reading since March 2011, while the new orders component spiked to 66.7, a good indicator of future growth and supportive of our theme of a capital expenditure resurgence.

Capital Expenditures Seem Set to Expand Further

Â

Source: FactSet, ISM, U.S. Census Bureau. As of Sept. 5, 2014.

Also, the service side continued to show strength, as the ISM Non-Manufacturing Index rose to its best level since August 2005 at 59.6.Â

Finally, the labor market continues to show strength, despite a disappointing August payroll report that could just be an outlier; as initial jobless claims hover around the 300,000 mark, hiring surveys are showing increasing plans to add to staff, and the aforementioned JOLTS reports have been quite encouraging. The jobs report showed that 142,000 jobs were added, fewer than expected and the weakest reading of the year, although the unemployment rate fell to 6.1% from 6.2%. Given the other jobs data that did not jibe with this weaker release—and the fact that August payrolls have the highest historical upward revision rate of all months—we do not think the trend of stronger job growth has shifted. Â

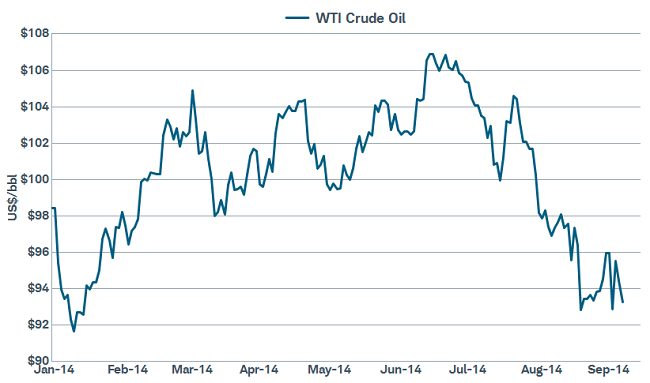

With consumer confidence at its highest level since 2008 according to the Conference Board, we could start to see the consumer kick more in to the economic expansion, with positive momentum likely heading into the holiday shopping season. An additional tailwind is coming from the energy complex as oil has fallen in recent weeks, indicating lower gasoline prices in the coming month, and potentially more moderate heating costs as we move closer to the winter heating season.Â

A tailwind for consumers

Source: FactSet, Commodity Research Bureau. As of Sept. 5, 2014.

Fed closing in, midterms in view

The decline in oil and other commodities, combined with still modest wage acceleration, should keep the doves at the Fed happy, although there is increasing dissent among the voting members. There is no doubt that the direction of the Fed is diverging from most other central banks in the world, notably the ECB and Japan, with the first rate hike in sight here, while easing has been stepped up elsewhere. These divergent policies, along with some risk that rate hikes could come sooner than expected,  has helped to strengthen the U.S. dollar; which in turn has put pressure on gold, oil, and other commodities. We note that stocks have continued to rise along with the dollar, contrary to some investors’ beliefs. Although the stock market generally prefers dollar stability, history does show a positive correlation between stocks and the dollar.

And it may be hard to believe at times, but relative U.S. political stability also makes the dollar attractive, especially in times of heighted geopolitical worries. We may fight and squabble, but peaceful and lawful transfer of power is often taken for granted here. That doesn’t mean there won’t be some nastiness over the next couple of months heading into the midterm elections where the balance of power in the House and the Senate is up for grabs. Increased volatility and a pullback in stocks have tended to occur in the lead up to midterm elections, so be prepared; but the period following the election has usually been quite good for stocks, reinforcing our belief that a decent pullback in equities would represent a buying opportunity.Â

Europe’s weak foundation suppressing growth

While the Fed has been viewed by some as being too accommodative, the opposite could be said for the European Central Bank (ECB), which has been accused of not doing enough. Add to the mix a regional economy that lacks the dynamic nature of the United States, due to regulations that stifle innovation and competitiveness, and it’s not surprising that the euro zone recovery has lagged.

Additionally, complications for Europe keep recurring. After returning to growth in 2013 in the aftermath of the peripheral sovereign debt crisis, new threats have emerged; including unrest in the Ukraine, and now the possibility Scotland could break away from the United Kingdom (U.K.). We believe voters are unlikely to ultimately cast a yes vote given the many uncertainties surrounding a separation, but the vote could create volatility and disruptions in markets. Equally important are implications for the future membership of the U.K. in the European Union and for separatist campaigns across Europe; particularly in the region of Catalonia, where an unauthorized vote to secede from Spain is targeted for November 9.

Deflation, or a broad-based decline in prices, is also a threat in Europe. Because the amount of debt doesn’t change when prices and incomes fall, more income is needed to service the debt, which can then result in spending cuts. Additionally, once consumers and businesses believe prices will be lower in the future, they typically postpone spending, creating a negatively-reinforcing economic slowdown. A slip in inflation expectations by the bond market in August forced the ECB’s hand to announce a quantitative easing (QE) program to purchase asset-backed securities and covered bonds starting in October.

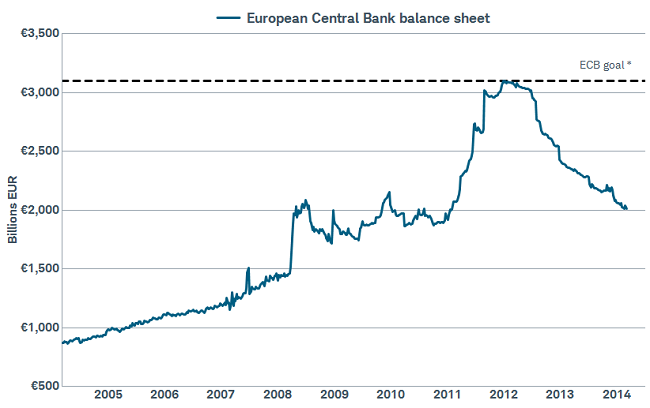

ECB aims for a significant stimulus

Source: FactSet, European Central Bank. As of Sept. 9, 2014. * The European Central Bank's (ECB) aim is to steer the size of the balance sheet to the level at the beginning of 2012.

The ECB’s QE announcement is a positive development if it keeps downward pressure on the euro. This would help the euro zone by making exports less expensive and therefore more competitive; and could help generate some inflation through higher import prices.

However, we are skeptical the ECB’s QE will be enough to lift the euro zone economy out of its anemic recovery. We believe the euro zone needs to do more to address its structural issues, and the ECB’s move could reduce the pressure to pursue structural reforms. These reforms are particularly needed in the large economies of France and Italy. We believe economic growth and corporate earnings have downside risks, keeping us neutral on European stocks.

Will Japan’s companies unleash their cash?

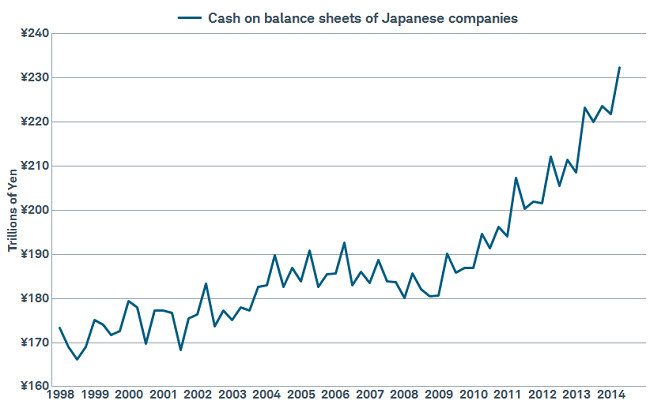

Japan is renowned for its dreaded “Ds:†deflation, debt and aging demographics—all of which stifle demand. These problems have resulted in a very cautious corporate sector, inclined to hoard cash. While this has been the case in other countries, particularly after the global financial crisis, nowhere is it more apparent than in Japan. As a ratio of stock market capitalization, Japanese companies’ cash averaged 40% of market cap during 2004-2012, compared to a range of 15-27% for other G7 countries, and has reached close to 50% of nominal GDP according to the International Monetary Fund.

Will Japan Inc Start Using Cash?

Source: FactSet, Bank of Japan. As of Sept. 9, 2014.

We are encouraged by policy moves to improve corporate governance and the return on equity of Japanese companies. Corporate cash could be unlocked by either returning money to shareholders or increasing investment to improve productivity. Japanese stocks could perform well in the near term despite Japan’s longer-term structural issues; particularly if changes to corporate taxes, the asset allocation of the Government Pension Investment Fund (GPIF), and extension of the Bank of Japan’s (BoJ) QE, are enacted.

China: a tenuous balancing act

In contrast with many other countries, China needs less investment and more consumption. Positively, Chinese policymakers have undertaken a long-term reform plan to transition away from a government-directed economy toward one that is market-based. However, these reforms are likely to slow growth, so the trick is to pursue reforms at a pace that keeps growth from slipping too much. As a result, the economy could experience bumps up and down.Â

Investors are still getting accustomed to both slower, as well as more variable, growth in China. Concerns about debt defaults and payoffs earlier this year resulted in fears about an economic hard landing, but the relative stability in the economy has encouraged investors to begin returning to Chinese stocks.

We are encouraged by a stabilization in Chinese exports and emerging market growth overall. This is despite still sluggish European and Japanese economies, as emerging market countries increasingly transact with each other. The United States remains a major export destination for many countries, and the strengthening of its economy adds to China’s growth.

However, interest rates, and therefore credit, remain somewhat restrictive, as the effective rate for corporate borrowers is often higher than published rates due to extra fees and costs imposed by banks; and favorable mortgage rates are reserved for borrowers with large bank accounts. The government is still testing new targeted easing measures during the transition to a market-based economy, which could result in policy mistakes in the interim.

We believe the Chinese government has plenty of levers to stimulate growth in the event it slips too far. Despite the concerns about infrastructure overbuilding, China’s economy still has room to improve in the basics of water and energy. As examples, the second leg of the $62 billion South-North Water Transfer Project is set to open in October, highlighting the water issues in China; and reportedly the government recently has been considering a $16 billion investment in electric car charging infrastructure.

Although Chinese stocks may need to take a breather, and the property market remains a longer-term risk, we believe there is more upside. Chinese stocks are likely to benefit from further stimulus, attractive valuations, and continued reform moves, as well as the upcoming cross-exchange Shanghai - Hong Kong Stock Connect (SHKSC), or “through train.â€

Additionally, we are warming to the overall emerging market stock universe due to a stabilization in growth and because emerging market stocks are one of the few asset classes where valuations are attractive in what has become an increasingly expensive world. Read more international commentary at www.schwab.com/oninternational.

So what?

A correction is always possible and risks are all around but we believe a relatively strong U.S. economy can help to support further gains in stocks and that inevitable pullbacks should be used as buying opportunities. Fed timing and election uncertainty could raise volatility, so be prepared for some bumps along the way. The ECB finally acted but we are skeptical it can stimulate demand and more structural changes are needed; while Japan could continue to perform well in the near term. China faces a tough balancing act and stocks may be due for a near-term pullback, but we remain positive on Chinese and emerging market equities.