When major market indexes reach new heights, some investors may become wary. Given that the US stock market has enjoyed robust total returns over the past five years (2009–2013), it’s only natural to question the sustainability of rising stock prices.Grant Bowers, portfolio manager of Franklin Growth Opportunities Fund, believes many of the same drivers of stock market performance over the past few years remain in place, including low inflation, healthy corporate profits and accommodative monetary policy. However, he also cautions that volatility is likely to pick up, particularly as investors continue to grapple with the prospect of rising US interest rates.

Grant Bowers

Grant Bowers

Vice President and Portfolio Manager

Franklin Equity Group®

When we step back to look at the bigger picture, we still see more reasons to be positive than negative and are optimistic about the US equity market. The US economy has continued to improve and has moved past the severe winter impact we saw in the first quarter of 2014. Economic data have been showing strength in key areas such as manufacturing, consumer spending and employment, all indicating to us that the US economy is on the right track, and in the middle of an economic expansion.

The market has rallied over the last few years on a healthy combination of earnings growth and multiple expansion. In our view here at Franklin Equity Group, stocks have been acting rationally, reflecting the improving economic backdrop we see in the United States. We think fundamentals remain strong for many companies, but valuations have also increased from the lows experienced during the financial crisis of 2008 and 2009 to levels closer to long-term historical averages.

Even with valuations increasing, many of the same factors that drove the market higher in the last few years appear to remain in place, in our view. In particular, we believe low inflation and accommodative monetary policy around the globe, combined with improving economic data and corporate profits in the United States, could be supportive of continued market growth in the years ahead. However, we would not be surprised to see more volatility in the equity markets going forward as investors continue to grapple with the Federal Reserve’s ongoing tapering process and with increased geopolitical risks. These periods of volatility can create great buying opportunities for long-term investors.

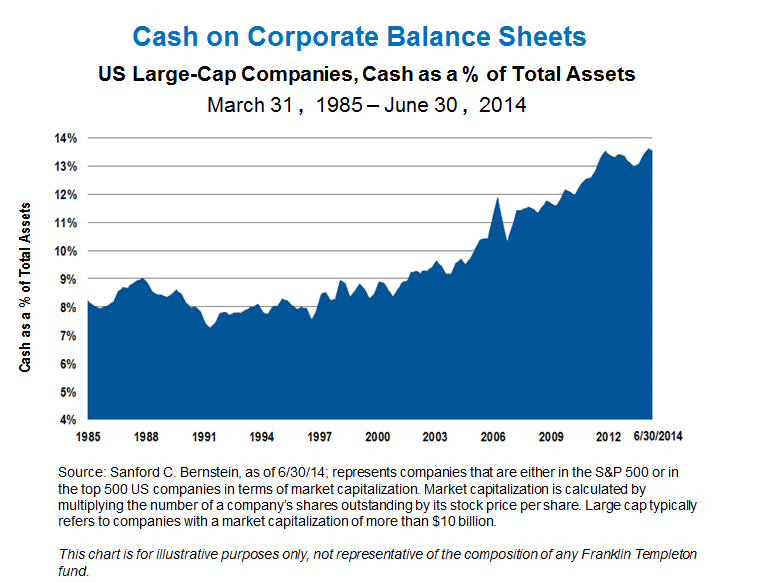

Looking forward, we believe strong corporate fundamentals will likely continue to support current valuation levels, and equity returns will likely be driven by earnings growth and, importantly, capital allocation decisions by corporate managements. Many US companies emerged from the global financial crisis leaner, stronger and more competitive than they were in 2007. This competitiveness, combined with strong cost controls, has resulted in record profits and driven the cash balances of many US companies to record levels.

For the past few years, US companies have focused their large cash balances on dividend increases and share repurchases, which, in an uncertain growth environment, can be a relatively safe and conservative use of cash for many companies. As the economic recovery has strengthened, these same companies have started to look at strategic mergers and acquisitions (M&A) to enhance their competitive position or to enter new growth markets. We started to see M&A activity pick up in 2013 and accelerate into 2014, with large deals being announced in the health care, media and industrials sectors. In an environment of low interest rates, record levels of corporate cash generation and healthy equity prices, we believe this trend should likely continue.

The Investment Case

We look for high-quality companies with what we view as having long-term growth potential, focusing on multi-year growth trends. We look to identify the leading companies—often those we believe are the number one or number two players in their industries—to be best positioned as the growth opportunity plays out over many years.

These growth companies often have some key characteristics that we focus on:

- Multi-year growth opportunities

- Strong competitive positions with high barriers to entry or wide economic moats

- Great management teams

- Financial strength; strong balance sheets and cash flow characteristics

We have been finding multi-year growth opportunities in many areas of the US market. These areas include traditional growth sectors like technology, in which the growth in mobile computing around the globe is creating huge revenue opportunities for many companies to reach new customers, or the shift to cloud computing that is disrupting the multibillion-dollar traditional technology industry and changing the way companies think about how they use and invest in technology. Health care is another important area. The sector has been buoyed by a record number of new drugs coming to market, combined with strong demand for these drugs around the globe.

We also find multi-year growth opportunities in non-traditional growth sectors like energy or industrials. One of the big themes we have been focused on is the often-referenced “US manufacturing renaissance.” We believe this is as much an energy renaissance as a manufacturing renaissance, as it is being driven by the vast discoveries of shale gas and oil in the United States over the last five years. These discoveries have dramatically changed the energy landscape, and we believe they will have large implications on the US industrials sector over the next decade. This renaissance has driven growth for many energy exploration companies and the service companies that supply the energy sector.

Interestingly, from an investment standpoint, we believe the manufacturing renaissance will likely benefit many areas of the US economy, from the obvious industrials and energy sectors to the US consumer, who could benefit broadly from low inflation, improving employment prospects and more discretionary spending as high-quality jobs return to the United States. As we look out over the next three to five years, we see this manufacturing renaissance having far-reaching implications that could provide a nice tailwind to the US economy for many years to come.

Grant Bowers’s comments, opinions and analyses are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

To get insights from Franklin Templeton Investments delivered to your inbox, subscribe to the Beyond Bulls & Bears blog.

For timely investing tidbits, follow us on Twitter @FTI_US and on LinkedIn.

What Are the Risks?

Franklin Growth Opportunities Fund

All investments involve risks, including possible loss of principal. Growth stock prices reflect projections of future earnings or revenues, and can, therefore, fall dramatically if the company fails to meet those projections. Smaller, mid-sized and relatively new or unseasoned companies can be particularly sensitive to changing economic conditions, and their prospects for growth are less certain than those of larger, more established companies. Historically, these securities have experienced more price volatility than larger company stocks, especially over the short term. To the extent the fund focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a fund that invests in a wider variety of countries, regions, industries, sectors or investments. These and other risks are described more fully in the fund’s prospectus.

Investors should carefully consider a fund’s investment goals, risks, charges and expenses before investing. To obtain a summary prospectus and/or prospectus, which contains this and other information, talk to your financial advisor, call us at (800) DIAL BEN®/342-5236 or visit franklintempleton.com. Please carefully read a prospectus before you invest or send money.