U.S. Oil Industry, Economy Feel Effects of Shale Revolution

The term “Shale Revolution” reflects the booming oil production from shale basins in the U.S. The rapid pace of oil output from these fields is spurring growth across the energy industry, providing a wide range of benefits to the U.S. economy and generating potential opportunities for investors.

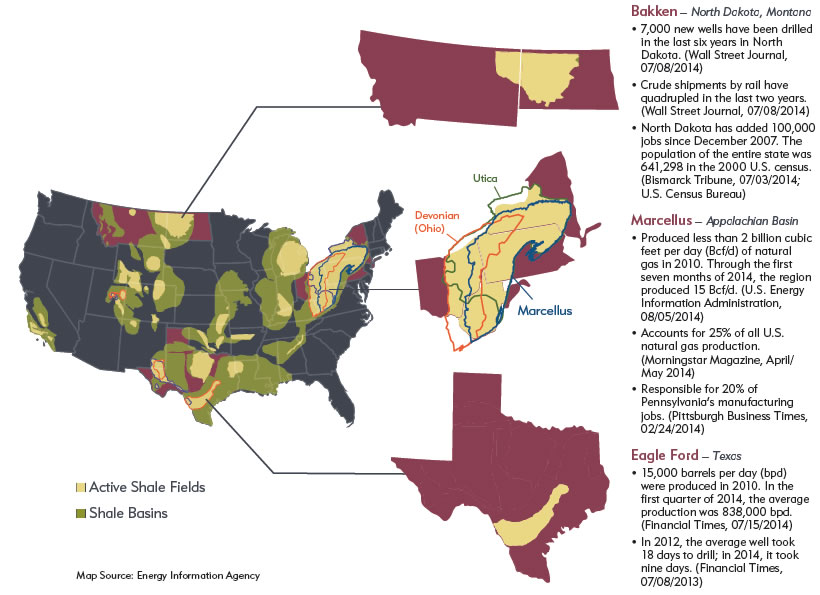

The shale revolution in the U.S. is based on rapidly growing oil production from the Bakken, Eagle Ford, Permian and other shale basins across the country. In general, output from these fields is growing faster than expected. This revolution is creating heavy spending on the energy industry’s infrastructure to exploit, handle and transport the additional oil and gas.

Shale is the major driver of almost everything in energy now. That includes capital spending by firms across the industry. That spending for many years was not leading to more oil production. In the U.S. shale basins now, however, more capital spending has meant increased production growth.

A great deal of the spending goes beyond developing oil and gas wells to include infrastructure such as pipelines and other transportation and processing facilities.

We think the shale revolution also is supporting what we would call an industrial renaissance in the U.S., led by low energy costs. In our view, this renaissance is creating opportunities for companies across the oil and gas industry, as well as for many outside the energy sector. For example, companies in chemicals, fertilizer, steel and aluminum are gaining the benefit of lower costs. Engineering and construction companies are generating revenue from energy infrastructure projects.

Even companies that supply and manage water and specialty sand are benefitting from hydraulic fracturing, or “fracking.” The process requires about 4 million pounds of sand and 4 million gallons of water per well, according to U.S. Environmental Protection Agency estimates. The water also must be treated when it comes out of the well.

We think the shale revolution is contributing to the U.S. economy in a variety of other ways. We’ve seen significant job growth in states with major shale basins such as North Dakota, Ohio, Texas and Pennsylvania. In fact, energy employment has seen a much more rapid recovery than total employment in the U.S. since the low point of the Great Recession, according to the U.S. Bureau of Labor Statistics.

In addition, lower energy costs provide benefits to consumers, help hold down inflation and contribute to reducing the U.S. trade deficit. The increased production can boost revenue for energy-producing states and for the federal government.

The rapid growth in shale has reduced our focus on offshore drilling because many companies are finding it easier and less risky to invest in shale than in deepwater drilling. Costs for offshore wells have been increasing since the Deepwater Horizon explosion and oil spill in the Gulf of Mexico in 2010. Companies also are finding that the potential returns from drilling a deepwater well are declining. Many exploration & production (E&P) companies therefore are less willing to devote new capital to deepwater wells. We think this is likely to be cyclical, meaning enthusiasm for deepwater wells will come back at some point. But we believe the next couple of years will continue to show capital spending primarily in the shale basins.

The increased oil production in the U.S. has caused speculation about the potential to begin exporting oil. While the federal government has not approved exports, we think we are getting closer to that day. Our view on that has changed in just the last two years because of the shale oil boom.

Natural gas prices still languish

Production of natural gas continues to grow despite a reduction in the rig count to about a 19-year low. This increased output is another facet of increased oil production, which generates “associated gas.” The steady increase in oil-producing rigs means more natural gas as well as oil. That increased output, however, is keeping a lid on natural gas prices. They moved higher during the winter because of the severe weather and greater demand. While the weather-related demand drew down gas reserves, increased production has led to a rapid replenishment so far this summer.

We think there would need to be a significant change in natural gas fundamentals and additional demand to generate a dramatic price move higher. That said, we think we are nearing a low point for natural gas prices.

Moving forward, we think gas drilling will increase if the U.S. starts exporting more liquefied natural gas (LNG) and if there is increased use in chemical plants. In our view, that is 18 to 24 months in the future.

It’s worth noting that Saudi Arabia has indicated an intent to expand natural gas production in the next two to three years. This search reflects in part its use of domestic oil to generate electricity for utility and water desalination plants. If Saudi Arabia can find and burn natural gas in these plants, it could free up about 3 million barrels of oil for export. We think this also is an indication that it would be difficult for Saudi Arabia – the world’s largest oil producer – to expand its oil production dramatically now.

Outlook for steady oil prices

We do not expect a drop-off in demand for energy in the near future. Most of the growth is coming from developing countries now, including China, India and across the Middle East. Those countries alone include a total population estimated at 3 billion people. As they continue to grow their economies and pursue a more “western” lifestyle, they will continue to demand more energy.

We always are concerned about factors that could induce “demand destruction” from higher oil prices. In our view, oil prices must increase to represent spending of 8 to 10% of gross domestic product (GDP) before demand begins to decline. We think that would translate to an oil price of about $140 per barrel, far above the current price and not a price we expect in the near term.

As we’ve described, we think supply growth is likely to continue in North America from the shale oil fields in the U.S. and Canada. That will help maintain prices in the current narrow range around $100 per barrel. But we also don’t expect a significant decline in the oil price from that range. We think any price declines would prompt a drop in output worldwide to maintain the price.

Information is subject to change and is not intended to represent any past or future investment recommendations.

David Ginther is portfolio manager of Ivy Energy Fund.

Past performance is not a guarantee of future results. The opinions expressed are those of the Fund’s portfolio manager and are not meant as investment advice or to predict or project the future performance of any investment product. The opinions are current through Aug. 22, 2014, and are subject to change due to market conditions or other factors.

Investment return and principal value will fluctuate, and it is possible to lose money by investing.

Risk factors. As with any mutual fund, the value of the Fund’s shares will change, and you could lose money on your investment. Investing in companies involved in one specified sector may be more risky and volatile than an investment with greater diversification.

Investing in the energy sector can be riskier than other types of investment activities because of a range of factors, including price fluctuation caused by real and perceived inflationary trends and political developments, and the cost assumed by energy companies in complying with environmental safety regulations. These and other risks are more fully described in the Fund’s prospectus. Not all funds or fund classes may be offered at all broker/dealers.

Investors should consider the investment objectives, risks, charges and expenses of a fund carefully before investing. For a prospectus, or if available, a summary prospectus, containing this and other information for the Ivy Funds, call your financial advisor or visit www.ivyfunds.com. Please read the prospectus or summary prospectus carefully before investing.

© Ivy Investment Management Company