In April I had good results with Dare to Be Great II, starting from the base established in an earlier memo (Dare to Be Great, September 2006) and adding new thoughts that had occurred to me in the intervening years. Also in 2006 I wrote Risk, my first memo devoted entirely to this key subject. My thinking continued to develop, causing me to dedicate three chapters to risk among the twenty in my book The Most Important Thing. This memo adds to what I’ve previously written on the topic.

What Risk Really Means

In the 2006 memo and in the book, I argued against the purported identity between volatility and risk. Volatility is the academic’s choice for defining and measuring risk. I think this is the case largely because volatility is quantifiable and thus usable in the calculations and models of modern finance theory. In the book I called it “machinable,” and there is no substitute for the purposes of the calculations.

However, while volatility is quantifiable and machinable – and can also be an indicator or symptom of riskiness and even a specific form of risk – I think it falls far short as “the” definition of investment risk. In thinking about risk, we want to identify the thing that investors worry about and thus demand compensation for bearing. I don’t think most investors fear volatility. In fact, I’ve never heard anyone say, “The prospective return isn’t high enough to warrant bearing all that volatility.” What they fear is the possibility of permanent loss.

Permanent loss is very different from volatility or fluctuation. A downward fluctuation – which by definition is temporary – doesn’t present a big problem if the investor is able to hold on and come out the other side. A permanent loss – from which there won’t be a rebound – can occur for either of two reasons: (a) an otherwise-temporary dip is locked in when the investor sells during a downswing – whether because of a loss of conviction; requirements stemming from his timeframe; financial exigency; or emotional pressures, or (b) the investment itself is unable to recover for fundamental reasons. We can ride out volatility, but we never get a chance to undo a permanent loss.

Of course, the problem with defining risk as the possibility of permanent loss is that it lacks the very thing volatility offers: quantifiability. The probability of loss is no more measurable than the probability of rain. It can be modeled, and it can be estimated (and by experts pretty well), but it cannot be known.

In Dare to Be Great II, I described the time I spent advising a sovereign wealth fund about how to organize for the next thirty years. My presentation was built significantly around my conviction that risk can’t be quantified a priori. Another of their advisors, a professor from a business school north of New York, insisted it can. This is something I prefer not to debate, especially with people who’re sure they have the answer but haven’t bet much money on it.

One of the things the professor was sure could be quantified was the maximum a portfolio could fall under adverse circumstances. But how can this be so if we don’t know how adverse circumstances can be or how they will influence returns? We might say “the market probably won’t fall more than x% as long as things aren’t worse than y and z,” but how can an absolute limit be specified? I wonder if the professor had anticipated that the S&P 500 could fall 57% in the global crisis.

While writing the original memo on risk in 2006, an important thought came to me for the first time. Forget about a priori; if you define risk as anything other than volatility, it can’t be measured even after the fact. If you buy something for $10 and sell it a year later for $20, was it risky or not? The novice would say the profit proves it was safe, while the academic would say it was clearly risky, since the only way to make 100% in a year is by taking a lot of risk. I’d say it might have been a brilliant, safe investment that was sure to double or a risky dart throw that got lucky.

If you make an investment in 2012, you’ll know in 2014 whether you lost money (and how much), but you won’t know whether it was a risky investment – that is, what the probability of loss was at the time you made it. To continue the analogy, it may rain tomorrow, or it may not, but nothing that happens tomorrow will tell you what the probability of rain was as of today. And the risk of rain is a very good analogue (although I’m sure not perfect) for the risk of loss.

The Unknowable Future

It seems most people in the prediction business think the future is knowable, and all they have to do is be among the ones who know it. Alternatively, they may understand (consciously or unconsciously) that it’s not knowable but believe they have to act as if it is in order to make a living as an economist or investment manager.

On the other hand, I’m solidly convinced the future isn’t knowable. I side with John Kenneth Galbraith who said, “We have two classes of forecasters: Those who don’t know – and those who don’t know they don’t know.” There are several reasons for this inability to predict:

- We’re well aware of many factors that can influence future events, such as governmental actions, individuals’ spending decisions and changes in commodity prices. But these things are hard to predict, and I doubt anyone is capable of taking all of them into account at once. (People have suggested a parallel between this categorization and that of Donald Rumsfeld, who might have called these things “known unknowns”: the things we know we don’t know.)

- The future can also be influenced by events that aren’t on anyone’s radar today, such as calamities – natural or man-made – that can have great impact. The 9/11 attacks and the Fukushima disaster are two examples of things no one knew to think about. (These would be “unknown unknowns”: the things we don’t know we don’t know.)

- There’s far too much randomness at work in the world for future events to be predictable. As 2014 began, forecasters were sure the U.S. economy was gaining steam, but they were confounded when record cold weather caused GDP to fall 2.9% in the first quarter.

- And importantly, the connections between contributing influences and future outcomes are far too imprecise and variable for the results to be dependable.

That last point deserves discussion. Physics is a science, and for that reason an electrical engineer can guarantee you that if you flip a switch over here, a light will go on over there … every time. But there’s good reason why economics is called “the dismal science,” and in fact it isn’t much of a science at all. In just the last few years we’ve had opportunity to see – contrary to nearly unanimous expectations – that interest rates near zero can fail to produce a strong rebound in GDP, and that a reduction of bond buying on the part of the Fed can fail to bring on higher interest rates. In economics and investments, because of the key role played by human behavior, you just can’t say for sure that “if A, then B,” as you can in real science. The weakness of the connection between cause and effect makes outcomes uncertain. In other words, it introduces risk.

Given the near-infinite number of factors that influence the future, the great deal of randomness present, and the weakness of the linkages, it’s my solid belief that future events cannot be predicted with any consistency. In particular, predictions of important divergences from trends and norms can’t be made with anything approaching the accuracy required for them to be helpful.

Coping with the Unknowable Future

Here’s the essential conundrum: investing requires us to decide how to position a portfolio for future developments, but the future isn’t knowable.

Taken to slightly greater detail:

- Investing requires the taking of positions that will be affected by future developments.

- The existence of negative possibilities surrounding those future developments presents risk.

- Intelligent investors pursue prospective returns that they think compensate them for bearing the risk of negative future developments.

- But future developments are unpredictable.

How can investors deal with the limitations on their ability to know the future? The answer lies in the fact that not being able to know the future doesn’t mean we can’t deal with it. It’s one thing to know what’s going to happen and something very different to have a feeling for the range of possible outcomes and the likelihood of each one happening. Saying we can’t do the former doesn’t mean we can’t do the latter.

The information we’re able to estimate – the list of events that might happen and how likely each one is – can be used to construct a probability distribution. Key point number one in this memo is that the future should be viewed not as a fixed outcome that’s destined to happen and capable of being predicted, but as a range of possibilities and, hopefully on the basis of insight into their respective likelihoods, as a probability distribution.

Since the future isn’t fixed and future events can’t be predicted, risk cannot be quantified with any precision. I made the point in Risk, and I want to emphasize it here, that risk estimation has to be the province of experienced experts, and their work product will by necessity be subjective, imprecise, and more qualitative than quantitative (even if it’s expressed in numbers).

There’s little I believe in more than Albert Einstein’s observation: “Not everything that counts can be counted, and not everything that can be counted counts.” I’d rather have an order-of-magnitude approximation of risk from an expert than a precise figure from a highly educated statistician who knows less about the underlying investments. British philosopher and logician Carveth Read put it this way: “It is better to be vaguely right than exactly wrong.”

By the way, in my personal life I tend to incorporate another of Einstein’s comments: “I never think of the future – it comes soon enough.” We can’t take that approach as investors, however. We have to think about the future. We just shouldn’t accord too much significance to our opinions.

We can’t know what will happen. We can know something about the possible outcomes (and how likely they are). People who have more insight into these things than others are likely to make superior investors. As I said in the last paragraph of The Most Important Thing:

Only investors with unusual insight can regularly divine the probability distribution that governs future events and sense when the potential returns compensate for the risks that lurk in the distribution’s negative left-hand tail.

In other words, in order to achieve superior results, an investor must be able – with some regularity – to find asymmetries: instances when the upside potential exceeds the downside risk. That’s what successful investing is all about.

Thinking in Terms of Diverse Outcomes

It’s the indeterminate nature of future events that creates investment risk. It goes without saying that if we knew everything that was going to happen, there wouldn’t be any risk.

The return on a stock will be a function of the relationship between the price today and the cash flows (income and sale proceeds) it will produce in the future. The future cash flows, in turn, will be a function of the fundamental performance of the company and the way its stock is priced given that performance. We invest on the basis of expectations regarding these things. It’s tautological to say that if the company’s earnings and the valuation of those earnings meet our targets, the return will be as expected. The risk in the investment therefore comes from the possibility that one or both will come in lower than we think.

To oversimplify, investors in a given company may have an expectation that if A happens, that’ll make B happen, and if C and D also happen, then the result will be E. Factor A may be the pace at which a new product finds an audience. That will determine factor B, the growth of sales. If A is positive, B should be positive. Then if C (the cost of raw materials) is on target, earnings should grow as expected, and if D (investors’ valuation of the earnings) also meets expectations, the result should be a rising share price, giving us the return we seek (E).

We may have a sense for the probability distributions governing future developments, and thus a feeling for the likely outcome regarding each of developments A through E. The problem is that for each of these, there can be lots of outcomes other than the ones we consider most likely. The possibility of less-good outcomes is the source of risk. That leads me to my second key point, as expressed by Elroy Dimson, a professor at the London Business School: “Risk means more things can happen than will happen.” This brief, pithy sentence contains a great deal of wisdom.

Here’s how I put it in No Different This Time – The Lessons of ’07 (December 2007):

No ambiguity is evident when we view the past. Only the things that happened happened. But that definiteness doesn’t mean the process that creates outcomes is clear-cut and dependable. Many things could have happened in each case in the past, and the fact that only one did happen understates the variability that existed. What I mean to say (inspired by Nicolas Nassim Taleb’s Fooled by Randomness) is that the history that took place is only one version of what it could have been. If you accept this, then the relevance of history to the future is much more limited than may appear to be the case.

People who rely heavily on forecasts seem to think there’s only one possibility, meaning risk can be eliminated if they just figure out which one it is. The rest of us know many possibilities exist today, and it’s not knowable which of them will occur. Further, things are subject to change, meaning there will be new possibilities tomorrow. This uncertainty as to which of the possibilities will occur is the source of risk in investing.

Even a Probability Distribution Isn’t Enough

I’ve stressed the importance of viewing the future as a probability distribution rather than a single predetermined outcome. It’s still essential to bear in mind key point number three: Knowing the probabilities doesn’t mean you know what’s going to happen. For example, every good backgammon player knows the probabilities governing throws of the dice. They know there are 36 possible outcomes, and that six of them add up to the number seven (1-6, 2-5, 3-4, 4-3, 5-2 and 6-1). Thus the chance of throwing a seven on any toss is 6 in 36, or 16.7%. There’s absolutely no doubt about that. But even though we know the probability of each number, we’re far from knowing what number will come up on a given roll.

Backgammon players are usually quite happy to make a move that will enable them to win unless the opponent rolls twelve, since only one combination of the dice will produce it: 6-6. The probability of rolling twelve is thus only 1 in 36, or less than 3%. But twelve does come up from time to time, and the people it turns into losers end up complaining about having done the “right” thing but lost. As my friend Bruce Newberg says, “There’s a big difference between probability and outcome.” Unlikely things happen – and likely things fail to happen – all the time. Probabilities are likelihoods and very far from certainties.

It’s true with dice, and it’s true in investing … and not a bad start toward conveying the essence of risk. Think again about the quote above from Elroy Dimson: “Risk means more things can happen than will happen.” I find it particularly helpful to invert Dimson’s observation for key point number four: Even though many things can happen, only one will.

In Dare to Be Great II, I discussed the fact that economic decisions are usually best made on the basis of “expected value”: you multiply each potential outcome by its probability, sum the results, and select the path with the highest total. But while expected value weights all of the possible outcomes on the basis of their likelihood, there may be some individual outcomes that absolutely cannot be tolerated. Even though many things can happen, only one will … and if something unacceptable can happen on the path with the highest expected value, we may not be able to choose on that basis. We may have to shun that path in order to avoid the extreme negative outcome. I always say I have no interest in being a skydiver who’s successful 95% of the time.

Investment performance (like life in general) is a lot like choosing a lottery winner by pulling one ticket from a bowlful. The process through which the winning ticket is chosen can be influenced by physical processes, and also by randomness. But it never amounts to anything but one ticket picked from among many. Superior investors have a better sense for the tickets in the bowl, and thus for whether it’s worth buying a ticket in a lottery. Lesser investors have less of a sense for the probability distribution and for whether the likelihood of winning the prize compensates for the risk that the cost of the ticket will be lost.

Risk and Return

Both in the 2006 memo on risk and in my book, I showed two graphics that together make clear the nature of investment risk. People have told me they’re the best thing in the book, and since readers of this memo might have not seen the old one or read the book, I’m going to repeat them here.

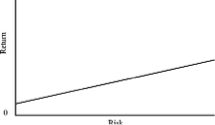

The first one below shows the relationship between risk and return as it is conventionally represented. The line slopes upward to the right, meaning the two are “positively correlated”: as risk increases, return increases.

In both the old memo and the book, I went to great lengths to clarify what this is often – but erroneously – taken to mean. We hear it all the time: “Riskier investments produce higher returns” and “If you want to make more money, take more risk.”

Both of these formulations are terrible. In brief, if riskier investments could be counted on to produce higher returns, they wouldn’t be riskier. Misplaced reliance on the benefits of risk bearing has led investors to some very unpleasant surprises.

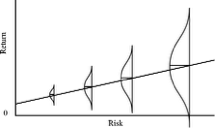

However, there’s another, better way to describe this relationship: “Investments that seem riskier have to appear likely to deliver higher returns, or else people won’t make them.” This makes perfect sense. If the market is rational, the price of a seemingly risky asset will be set low enough that the reward for holding it seems adequate to compensate for the risk present. But note the word “appear.” We’re talking about investors’ opinions regarding future return, not facts. Risky investments are – by definition – far from certain to deliver on their promise of high returns. For that reason, I think the graphic below does a much better job of portraying reality:

Here the underlying relationship between risk and return reflects the same positive general tendency as the first graphic, but the result of each investment is shown as a range of possibilities, not the single outcome suggested by the upward-sloping line. At each point along the horizontal risk axis, an investment’s prospective return is shown as a bell-shaped probability distribution turned on its side.

The conclusions are obvious from inspection. As you move to the right, increasing the risk:

- the expected return increases (as with the traditional graphic),

- the range of possible outcomes becomes wider, and

- the less-good outcomes become worse.

This is the essence of investment risk. Riskier investments are ones where the investor is less secure regarding the eventual outcome and faces the possibility of faring worse than those who stick to safer investments, and even of losing money. These investments are undertaken because the expected return is higher. But things may happen other than that which is hoped for. Some of the possibilities are superior to the expected return, but others are decidedly unattractive.

The first graph’s upward-sloping line indicates the underlying directionality of the risk/return relationship. But there’s a lot more to consider than the fact that expected returns rise along with perceived risk, and in that regard the first graph is highly misleading. The second graph shows both the underlying trend and the increasing potential for actual returns to deviate from expectations. While the expected return rises along with risk, so does the probability of lower returns … and even of losses. This way of looking at things reflects Professor Dimson’s dictum that more than one thing can happen. That’s reality in an unpredictable world.

The Many Forms of Risk

The possibility of permanent loss may be the main risk in investing, but it’s not the only risk. I can think of lots of other risks, many of which contribute to – or are components of – that main risk.

In the past, in addition to the risk of permanent loss, I’ve mentioned the risk of falling short. Some investors face return requirements in order to make necessary payouts, as in the case of pension funds, endowments and insurance companies. Others have more basic needs, like generating enough income to live on.

Some investors with needs – particularly those who live on their income, and especially in today’s low-return environment – face a serious conundrum. If they put their money into safe investments, their returns may be inadequate. But if they take on incremental risk in pursuit of a higher return, they face the possibility of a still-lower return, and perhaps of permanent diminution of their capital, rendering their subsequent income lower still. There’s no easy way to resolve this conundrum.

There are actually two possible causes of inadequate returns: (a) targeting a high return and being thwarted by negative events and (b) targeting a low return and achieving it. In other words, investors face not one but two major risks: the risk of losing money and the risk of missing opportunities. Either can be eliminated but not both. And leaning too far in order to avoid one can set you up to be victimized by the other.

Potential opportunity costs – the result of missing opportunities – usually aren’t taken as seriously as real potential losses. But they do deserve attention. Put another way, we have to consider the risk of not taking enough risk.

These days, the fear of losing money seems to have receded (since the crisis is all of six years in the past), and the fear of missing opportunities is riding high, given the paltry returns available on safe, mundane investments. Thus a new risk has arisen: FOMO risk, or the risk that comes from excessive fear of missing out. It’s important to worry about missing opportunities, since people who don’t can invest too conservatively. But when that worry becomes excessive, FOMO can drive an investor to do things he shouldn’t do and often doesn’t understand, just because others are doing them: if he doesn’t jump on the bandwagon, he may be left behind to live with envy.

Over the last three years, Oaktree’s response to the paucity of return has been to develop a suite of five credit strategies that we hope will produce a 10% return, either net or gross (we can’t claim to be more precise than that). I call them collectively the “ten percent solution,” after a Sherlock Holmes story called The Seven-Per-Cent Solution (we aim to do better). Talking to clients about these strategies and helping them choose between them has required me to focus on their risks.

“Just a minute,” you might say, “the ten-year Treasury is paying just 2½% and, as Jeremy Grantham says, the risk-free rate is also return-free. How, then, can you target returns in the vicinity of 10%?” The answer is that it can’t be done without taking risk of some kind – and there are several candidates. I’ll list below a few risks that we’re consciously bearing in order to generate the returns our clients desire:

-

Today’s ultra-low interest rates imply low returns for anyone who invests in what are deemed safe fixed income instruments. So Oaktree’s pursuit of attractive returns centers on accepting and managing credit risk, or the risk that a borrower will be unable to pay interest and repay principal as scheduled. Treasurys are assumed to be free of credit risk, and most high grade corporates are thought to be nearly so. Thus those who intelligently accept incremental credit risk must do so with the expectation that the incremental return promised as compensation will prove sufficient.

Voluntarily accepting credit risk has been at the core of what Oaktree has done since its beginning in 1995 (and in fact since the seed was planted in 1978, when I initiated Citibank’s high yield bond effort). But bearing credit risk will lead to attractive returns only if it’s done well. Our activities are based on two beliefs: (a) that because the investing establishment is averse to credit risk, the incremental returns we receive for bearing it will compensate generously for the risk entailed and (b) that credit risk is manageable – i.e., unlike the general future, credit risk can be gauged by experts (like us) and reduced through credit selection. It wouldn’t make sense to voluntarily bear incremental credit risk if either of these two beliefs were lacking.

-

Another way to access attractive returns in today’s low-rate environment is to bear illiquidity risk in order to take advantage of investors’ normal dislike for illiquidity (superior returns often follow from investor aversion). Institutions that held a lot of illiquid assets suffered considerably in the crisis of 2008, when they couldn’t sell them; thus many developed a strong aversion to them and in some cases imposed limitations on their representation in portfolios. Additionally, today the flow of retail money is playing a big part in driving up asset prices and driving down returns. Since retail money has a harder time making its way to illiquid assets, this has made the returns on the latter appear more attractive. It’s noteworthy that there aren’t mutual funds or ETFs for many of the things we’re investing in.

-

Some strategies introduce it voluntarily and some can’t get away from it: concentration risk. “Everyone knows” diversification is a good thing, since it reduces the impact on results of a negative development. But some people eschew the safety that comes with diversification in favor of concentrating their investments in assets or with managers they expect to outperform. And some investment strategies don’t permit full diversification because of the limitations of their subject markets. Thus problems – if and when they occur – will be bigger per se.

-

Especially given today’s low interest rates, borrowing additional capital to enhance returns is another way to potentially increase returns. But doing so introduces leverage risk. Leverage adds to risk two ways. The first is magnification: people are attracted to leverage because it will magnify gains, but under unfavorable outcomes it will magnify losses instead.

The second way in which leverage adds to risk stems from funding risk, one of the classic reasons for financial disaster. The stage is set when someone borrows short-term funds to make a long-term investment. If the funds have to be repaid at an awkward time – due to their maturity, a margin call, or some other reason – and the purchased assets can’t be sold in a timely fashion (or can only be sold at a depressed price), an investment that might otherwise have been successful can be cut short and end in sorrow. Little or nothing may remain of the sale proceeds once the leverage has been repaid, in which case the investor’s equity will be decimated. This is commonly called a meltdown. It’s the primary reason for the saying, “Never forget the six-foot-tall man who drowned crossing the stream that was five feet deep on average.” In times of crisis, success over the long run can become irrelevant.

-

When credit risk, illiquidity risk, concentration risk and leverage risk are borne intelligently, it is in the hope that the investor’s skill will be sufficient to produce success. If so, the potential incremental returns that appear to be offered as risk compensation will turn into realized incremental returns (per the graphic at the top of page 6). That’s the only reason anyone would do these things.

As the graphic at the bottom of page 6 illustrates, however, investing further out on the risk curve exposes one to a broader range of investment outcomes. In an efficient market, returns are tethered to the market average; in an inefficient market, they’re not. Inefficient markets offer the possibility that an investor will escape from the “gravitational pull” of the market’s average return, but that can be either for the better or for the worse. Superior investors – those with “alpha,” or the personal skill needed to achieve outsized returns for a given level of risk – have scope to perform well above the mean return, while inferior investors can come out far below. So hiring an investment manager introduces manager risk: the risk of picking the wrong one. It’s possible to pay management fees but get decisions that detract from results rather than add.

Some or all of the above risks are potentially entailed in our new credit strategies. Parsing them allows investors to choose among the strategies and accept the risks they’re more comfortable with. The process can be quite informative.

Our oldest “new strategy” is Enhanced Income, where we use leverage to magnify the return from a portfolio of senior loans. We think senior loans have the lowest credit risk of anything Oaktree deals with, since they’re senior-most among their issuer’s debt and historically have produced very few credit losses. Further, they’re among our most liquid assets, meaning we face relatively little illiquidity risk, and being active in a broad public market permits us to diversify, reducing concentration risk. Given the relatively high degree of safety stemming from these loans’ seniority, returns aren’t overly dependent on the presence of alpha, meaning Enhanced Income entails less manager risk than some other strategies. But to have a chance at the healthy return we’re pursuing in Enhanced Income requires us to take some risk, and what we’re left with is leverage risk. The 3-to-1 leverage in Enhanced Income Fund II will magnify the negative impact of any credit losses (of course we hope there won’t be many). However, we’re not worried about a meltdown, since the current environment allows us to avoid funding risk; we can (a) borrow for a term that exceeds the duration of the underlying investments and (b) do so without the threat of margin calls related to price declines.

Strategic Credit, Mezzanine Finance, European Private Debt and Real Estate Debt are the other four components of our “ten percent solution.”

- All four entail some degree of credit risk, illiquidity risk (they all invest heavily or entirely in private debt) and concentration risk (as their market niches offer only a modest number of investment opportunities, and securing them in today’s competitive environment is a challenge).

- The Real Estate Debt Fund can only lever up to 1-to-1, and the other three borrow only small amounts and for short-term purposes, so none of them entails significant leverage risk.

- However, in order to succeed they’ll all require a high level of skill from their managers in identifying return prospects and keeping risk under control. Thus they all entail manager risk. Our response is to entrust these portfolios only to managers who’ve been with us for years.

It’s reasonable – essential, really – to study the risk entailed in every investment and accept the amounts and types of risk that you’re comfortable with (assuming this can be discerned). It’s not reasonable to expect highly superior returns without bearing some incremental risk.

I touched above on concentration risk, but we should also think about the flip side: the risk of over-diversification. If you have just a few holdings in a portfolio, or if an institution employs just a few managers, one bad decision can do significant damage to results. But if you have a very large number of holdings or managers, no one of them can have much of a positive impact on performance. Nobody invests in just the one stock or manager they expect to perform best, but as the number of positions is expanded, the standards for inclusion may decline. Peter Lynch coined the term “diworstification” to describe the process through which lesser investments are added to portfolios, making the potential risk-adjusted return worse.

While I don’t think volatility and risk are synonymous, there’s no doubt that volatility does present risk. If circumstances cause you to sell a volatile investment at the wrong time, you might turn a downward fluctuation into a permanent loss. Moreover, even in the absence of a need for liquidity, volatility can prey on investors’ emotions, reducing the probability they’ll do the right thing. And in the short run, it can be very hard to differentiate between a downward fluctuation and a permanent loss. Often this can really be done only in retrospect. Thus it’s clear that a professional investor may have to bear consequences for a temporary downward fluctuation simply because of its resemblance to a permanent loss. When you’re under pressure, the distinction between “volatility” and “loss” can seem only semantic. Volatility is not “the” definition of investment risk, as I said earlier, but it isn’t irrelevant.

One example of a risk connected with volatility – or the deviation of price from what might be intrinsic value – is basis risk. Arbitrageurs customarily set up positions where they’re long one asset and short a related asset. The two assets are expected to move roughly in parallel, except that the one that’s slightly cheaper should make more money for the investor in the long run than the other loses, producing a small net gain with little risk. Because these trades are considered so low in risk, they’re often levered up to the sky. But sometimes the prices of the two assets diverge to an unexpected extent, and the equity invested in the trade evaporates. That unexpected divergence is basis risk, and it’s what happened to Long-Term Capital Management in 1998, one of the most famous meltdowns of all time. As Long-Term’s chairman John Meriwether said at the time, “the Fund added to its positions in anticipation of convergence, yet … the trades diverged dramatically.” This benign-sounding explanation was behind a collapse some thought capable of bringing down the global financial system.

Long-Term’s failure was also attributable to model risk. Decisions can be turned over to quants or financial engineers who either (a) conclude wrongly that an unsystematic process can be modeled or (b) employ the wrong model. During the financial crisis, models often assumed that events would occur according to a “normal distribution,” but extreme “tail events” occurred much more often than the normal distribution says they will. Not only can extreme events exceed a model’s assumptions, but excessive belief in a model’s efficacy can induce people to take risks they would never take on the basis of qualitative judgment. They’re often disappointed to find they had put too much faith in a statistical sure thing.

Model risk can arise from black swan risk, for which I borrow the title of Nassim Nicholas Taleb’s popular second book. People tend to confuse “never been seen” with “impossible,” and the consequences can be dire when something occurs for the first time. That’s part of the reason why people lost so much in highly levered subprime mortgage securities. The fact that a nationwide spate of mortgage defaults hadn’t happened convinced investors that it couldn’t happen, and their certainty caused them to take actions so imprudent that it had to happen.

As long as we’re on the subject of things going wrong, we should touch on the subject of career risk. As I mentioned in Dare to Be Great II, “agents” who manage money for others can be penalized for investments that look like losers (that is, for both permanent losses and temporary downward fluctuations). Either of these unfortunate experiences can result in headline risk if the resulting losses are big enough to make it into the media, and some careers can’t withstand headline risk. Investors who lack the potential to share commensurately in investment successes face a reward asymmetry that can force them toward the safe end of the risk/return curve. They are likely to think more about the risk of losing money than about the risk of missing opportunities. Thus their portfolios may lean too far toward controlling risk and avoiding embarrassment (and they may not take enough chances to generate returns). There are consequences for these investors, as well as for those who employ them.

Event risk is another risk to worry about, something that was created by bond issuers about twenty years ago. Since corporate directors have a fiduciary responsibility to stockholders but not to bondholders, some think they can (and perhaps should) do anything that’s not explicitly prohibited to transfer value from bondholders to stockholders. Bondholders need covenants to shield them from this kind of pro-active plundering, but at times like today it can be hard to obtain strong protective covenants.

There are many ways for an investment to be unsuccessful. The two main ones are fundamental risk (relating to how a company or asset performs in the real world) and valuation risk (relating to how the market prices that performance). For years investors, fiduciaries and rule-makers acted on the belief that it’s safe to buy high-quality assets and risky to buy low-quality assets. But between 1968 and 1973, many investors in the “Nifty Fifty” (the stocks of the fifty fastest-growing and best companies in America) lost 80-90% of their money. Attitudes have evolved since then, and today there’s less of an assumption that high quality prevents fundamental risk, and much less preoccupation with quality for its own sake.

On the other hand, investors are more sensitive to the pivotal role played by price. At bottom, the riskiest thing is overpaying for an asset (regardless of its quality), and the best way to reduce risk is by paying a price that’s irrationally low (ditto). A low price provides a “margin of safety,” and that’s what risk-controlled investing is all about. Valuation risk should be easily combatted, since it’s largely within the investor’s control. All you have to do is refuse to buy if the price is too high given the fundamentals. “Who wouldn’t do that?” you might ask. Just think about the people who bought into the tech bubble.

Fundamental risk and valuation risk bear on the risk of losing money in an individual security or asset, but that’s far from the whole story. Correlation is the essential additional piece of the puzzle. Correlation is the degree to which an asset’s price will move in sympathy with the movements of others. The higher the correlation among its components, all other things being equal, the less effective diversification a portfolio has, and the more exposed it is to untoward developments.

An asset doesn’t have “a correlation.” Rather, it has a different correlation with every other asset. A bond has a certain correlation with a stock. One stock has a certain correlation with another stock (and a different correlation with a third). Stocks of one type (such as emerging market, high-tech or large-cap) are likely to be highly correlated with others within their category, but they may be either high or low in correlation with those in other categories. Bottom line: it’s hard to estimate the riskiness of a given asset, but many times harder to estimate its correlation with all the other assets in a portfolio, and thus the impact on performance of adding it to the portfolio. This is a real art.

Fixed income investors are directly exposed to another form of risk: interest rate risk. Higher interest rates mean lower bond prices – that relationship is absolute. The impact of changes in interest rates on asset classes other than fixed income is less direct and less obvious, but it also pervades the markets. Note that stocks usually go down when the Fed says the economy is performing strongly. Why? The thinking is that stronger economy = higher interest rates = more competition for stocks from bonds = lower stock valuations. Or it might be stronger economy = higher interest rates = reduced stimulus = weaker economy.

One of the reasons for increases in interest rates relates to purchasing power risk. Investors in securities (and especially long-term bonds) are exposed to the risk that if inflation rises, the amount they receive in the future will buy less than it could today. This causes investors to insist on higher interest rates and higher prospective returns to protect them against the loss of purchasing power. The result is lower prices.

Finally, I want to mention a new concept I hear about once in a while: upside risk. Forecasters are sometimes heard to say “the risk is on the upside.” At first this doesn’t seem to have much legitimacy, but it can be about the possibility that the economy may catch fire and do better than expected, earnings may come in above consensus, or the stock market may appreciate more than people think. Since these things are positives, there’s risk in being underexposed to them.

To move to the biggest of big pictures, I want to make a few over-arching comments about risk.

The first is that risk is counterintuitive.

- The riskiest thing in the world is the widespread belief that there’s no risk.

- Fear that the market is risky (and the prudent investor behavior that results) can render it quite safe.

- As an asset declines in price, making people view it as riskier, it becomes less risky (all else being equal).

- As an asset appreciates, causing people to think more highly of it, it becomes riskier.

- Holding only “safe” assets of one type can render a portfolio under-diversified and make it vulnerable to a single shock.

- Adding a few “risky” assets to a portfolio of safe assets can make it safer by increasing its diversification. Pointing this out was one of Professor William Sharpe’s great contributions.

The second is that risk aversion is the thing that keeps markets safe and sane.

- When investors are risk-conscious, they will demand generous risk premiums to compensate them for bearing risk. Thus the risk/return line will have a steep slope (the unit increase in prospective return per unit increase in perceived risk will be large) and the market should reward risk-bearing as theory asserts.

- But when people forget to be risk-conscious and fail to require compensation for bearing risk, they’ll make risky investments even if risk premiums are skimpy. The slope of the line will be gradual, and risk taking is likely to eventually be penalized, not rewarded.

- When risk aversion is running high, investors will perform extensive due diligence, make conservative assumptions, apply skepticism and deny capital to risky schemes.

- But when risk tolerance is widespread instead, these things will fall by the wayside and deals will be done that set the scene for subsequent losses.

Simply put, risk is low when risk aversion and risk consciousness are high, and high when they’re low.

The third is that risk is often hidden and thus deceptive. Loss occurs when risk – the possibility of loss – collides with negative events. Thus the riskiness of an investment becomes apparent only when it is tested in a negative environment. It can be risky but not show losses as long as the environment remains salutary. The fact that an investment is susceptible to a serious negative development that will occur only infrequently – what I call “the improbable disaster” – can make it appear safer than it really is. Thus after several years of a benign environment, a risky investment can easily pass for safe. That’s why Warren Buffett famously said, “… you only find out who’s swimming naked when the tide goes out.”

Assembling a portfolio that incorporates risk control as well as the potential for gains is a great accomplishment. But it’s a hidden accomplishment most of the time, since risk only turns into loss occasionally … when the tide goes out.

The fourth is that risk is multi-faceted and hard to deal with. In this memo I’ve mentioned 24 different forms of risk: the risk of losing money, the risk of falling short, the risk of missing opportunities, FOMO risk, credit risk, illiquidity risk, concentration risk, leverage risk, funding risk, manager risk, over-diversification risk, risk associated with volatility, basis risk, model risk, black swan risk, career risk, headline risk, event risk, fundamental risk, valuation risk, correlation risk, interest rate risk, purchasing power risk, and upside risk. And I’m sure I’ve omitted some. Many times these risks are overlapping, contrasting and hard to manage simultaneously. For example:

- Efforts to reduce the risk of losing money invariably increase the risk of missing out.

- Efforts to reduce fundamental risk by buying higher-quality assets often increase valuation risk, given that higher-quality assets often sell at elevated valuation metrics.

At bottom, it’s the inability to arrive at a single formula that simultaneously minimizes all the risks that makes investing the fascinating and challenging pursuit it is.

The fifth is that the task of managing risk shouldn’t be left to designated risk managers. I’m convinced outsiders to the fundamental investment process can’t know enough about the subject assets to make appropriate decisions regarding each one. All they can do is apply statistical models and norms. But those models may be the wrong ones for the underlying assets – or just plain faulty – and there’s little evidence that they add value. In particular, risk managers can try to estimate correlation and tell you how things will behave when combined in a portfolio. But they can fail to adequately anticipate the “fault lines” that run through portfolios. And anyway, as the old saying goes, “in times of crisis all correlations go to one” and everything collapses in unison.

“Value at Risk” was supposed to tell the banks how much they could lose on a very bad day. During the crisis, however, VaR was often shown to have understated the risk, since the assumptions hadn’t been harsh enough. Given the fact that risk managers are required at banks and de rigueur elsewhere, I think more money was spent on risk management in the early 2000s than in the rest of history combined … and yet we experienced the worst financial crisis in 80 years. Investors can calculate risk metrics like VaR and Sharpe ratios (we use them at Oaktree; they’re the best tools we have), but they shouldn’t put too much faith in them. The bottom line for me is that risk management should be the responsibility of every participant in the investment process, applying experience, judgment and knowledge of the underlying investments.

The sixth is that while risk should be dealt with constantly, investors are often tempted to do so only sporadically. Since risk only turns into loss when bad things happen, this can cause investors to apply risk control only when the future seems ominous. At other times they may opt to pile on risk in the expectation that good things lie ahead. But since we can’t predict the future, we never really know when risk control will be needed. Risk control is unnecessary in times when losses don’t occur, but that doesn’t mean it’s wrong to have it. The best analogy is to fire insurance: do you consider it a mistake to have paid the premium in a year in which your house didn’t burn down?

Taken together these six observations convince me that Charlie Munger’s trenchant comment on investing in general – “It’s not supposed to be easy. Anyone who finds it easy is stupid.” – is profoundly applicable to risk management. Effective risk management requires deep insight and a deft touch. It has to be based on a superior understanding of the probability distributions that will govern future events. Those who would achieve it have to have a good sense for what the crucial moving parts are, what will influence them, what outcomes are possible, and how likely each one is. Following on with Charlie’s idea, thinking risk control is easy is perhaps the greatest trap in investing, since excessive confidence that they have risk under control can make investors do very risky things.

Thus the key prerequisites for risk control also include humility, lack of hubris, and knowing what you don’t know. No one ever got into trouble for confessing a lack of prescience, being highly risk-conscious, and even investing scared. Risk control may restrain results during a rebound from crisis conditions or extreme under-valuations, when those who take the most risk generally make the most money. But it will also extend an investment career and increase the likelihood of long-term success. That’s why Oaktree was built on the belief that risk control is “the most important thing.”

Lastly while dealing in generalities, I want to point out that whereas risk control is indispensable, risk avoidance isn’t an appropriate goal. The reason is simple: risk avoidance usually goes hand-in-hand with return avoidance. While you shouldn’t expect to make money just for bearing risk, you also shouldn’t expect to make money without bearing risk.

At present I consider risk control more important than usual. To put it briefly:

- Today’s ultra-low interest rates have brought the prospective returns on money market instruments, Treasurys and high grade bonds to nearly zero.

- This has caused money to flood into riskier assets in search of higher returns.

- This, in turn, has caused some investors to drop their usual caution and engage in aggressive tactics.

- And this, finally, has caused standards in the capital markets to deteriorate, making it easy for issuers to place risky securities and – consequently – hard for investors to buy safe ones.

Warren Buffett put it best, and I regularly return to his statement on the subject:

…the less prudence with which others conduct their affairs, the greater the prudence with which we should conduct our own affairs.

While investor behavior hasn’t sunk to the depths seen just before the crisis (and, in my opinion, that contributed greatly to it), in many ways it has entered the zone of imprudence. To borrow a metaphor from Chuck Prince, Citigroup’s CEO from 2003 to 2007, anyone who’s totally unwilling to dance to today’s fast-paced music can find it challenging to put money to work.

It’s the job of investors to strike a proper balance between offense and defense, and between worrying about losing money and worrying about missing opportunity. Today I feel it’s important to pay more attention to loss prevention than to the pursuit of gain. For the last three years Oaktree’s mantra has been “move forward, but with caution.” At this time, in reiterating that mantra, I would increase the emphasis on those last three words: “but with caution.”

Economic and company fundamentals in the U.S. are fine today, and asset prices – while full – don’t seem to be at bubble levels. But when undemanding capital markets and a low level of risk aversion combine to encourage investors to engage in risky practices, something usually goes wrong eventually. Although I have no idea what could make the day of reckoning come sooner rather than later, I don’t think it’s too early to take today’s carefree market conditions into consideration. What I do know is that those conditions are creating a degree of risk for which there is no commensurate risk premium. We have to behave accordingly.

September 3, 2014

Legal Information and Disclosures

This memorandum, including the information contained herein, may not be copied, reproduced, republished, posted, transmitted, distributed, disseminated or disclosed, in whole or in part, to any other person in any way without the prior written consent of Oaktree Capital Management, L.P. (together with its affiliates, “Oaktree”).

This memorandum expresses the views of the author as of the date indicated and such views are subject to change without notice. Oaktree has no duty or obligation to update the information contained herein. Any reference to return goals is purely hypothetical and is not, and should not be considered, a guarantee nor a prediction or projection of future results. Actual returns often differ, in many cases materially, from any return goal as a result of many factors, including but not limited to the availability of suitable investments, the uncertainty of future operating results of investments, the timing of asset acquisitions and disposals, and the general economic conditions that prevail during the period that an investment is acquired, held or disposed of. You should bear in mind that returns goals are not indicative of future results, and there can be no assurance that the credit strategies will achieve comparable results, that return goals will be met or that the credit strategies will be able to implement its investment strategy or achieve its investment objectives. Moreover, wherever there is the potential for profit there is also the possibility of loss.

This memorandum is being made available for educational purposes only and does not constitute, and should not be construed as, an offer to sell, or a solicitation of an offer to buy, any securities, or an offer invitation or solicitation of any specific funds or the fund management services of Oaktree, or an offer or invitation to enter into any portfolio management mandate with Oaktree in any jurisdiction. Any offer of securities or funds may only be made pursuant to a confidential private placement memorandum, subscription documents and constituent documents in their final form.

An investment in any fund or the establishment of an account within Oaktree’s credit strategies is speculative and involves a high degree of risk. There can be no assurance that investments targeted by each of the strategies will increase in value, that significant losses will not be incurred or that the objectives of the strategies will be achieved. Moreover, a portfolio within one of the credit strategies may not be diversified among a wide range of issuers, industries and countries, making the portfolio subject to more rapid changes in value than would be the case if the portfolio was more diversified.

Many factors affect the demand and supply of securities and instruments targeted by the strategies discussed herein and their valuation. Interest rates and general economic activity may affect the value and number of investments made by such strategies. Such strategies discussed herein may target investments in companies whose capital structures may have significant leverage. Such investments are inherently more sensitive than others to declines in revenues and to increases in expenses and interest rates. In addition, such strategies may involve the use of leverage. While leverage presents opportunities for increasing total return, it may increase losses as well. Accordingly, any event that adversely affects the value of an investment would be magnified to the extent leverage is used. Such strategies may also involve securities or obligations of non-U.S. companies which may involve certain special risks. These factors may increase the likelihood of potential losses being incurred in connection with such investments. The investments that are part of such strategies could require substantial workout negotiations or restructuring in the event of a bankruptcy, which could entail significant risks, time commitments and costs. The investments targeted by such strategies may be thinly traded, may be subject to restrictions on resale or may be private securities. In such cases, the primary resale opportunities for such investments are privately negotiated transactions with a limited number of purchasers. This may restrict the disposition of investments in a timely fashion and at a favorable price. In addition, real estate-related investments can be seriously affected by interest rate fluctuations, bank liquidity, the availability of financing, and by regulatory or governmentally imposed factors such as a zoning change, an increase in property taxes, the imposition of height or density limitations, the requirement that buildings be accessible to disabled persons, the requirement for environmental impact studies, the potential costs of remediation of environmental contamination or damage, the imposition of special fines to reduce traffic congestion or to provide for housing, competition from other investors, changes in laws, wars, and earthquakes, typhoons, terrorist attacks or other similar events. Income from income-producing real estate may be adversely affected by general economic conditions, local conditions such as oversupply or reduction in demand for space in the area, competition from other available properties, and the owner provision of adequate maintenance and coverage by adequate insurance. Oaktree may be required for business or other reasons to foreclose on one or more mortgages held in such strategy’s portfolio. Foreclosures can be lengthy and expensive and borrowers often assert claims, counterclaims and defenses to delay or prevent foreclosure actions.

Responses to any inquiry that may involve the rendering of personalized investment advice or effecting or attempting to effect transactions in securities will not be made absent compliance with applicable laws or regulations (including broker dealer, investment adviser, or applicable agent or representative registration requirements), or applicable exemptions or exclusions therefrom.

Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Oaktree believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.