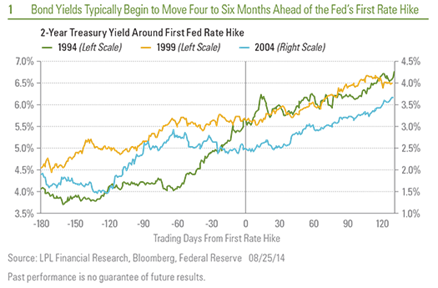

Historically, bond yields have begun to move more forcefully four to six months ahead of a first rate hike from the Fed.

We believe the rise in interest rates may begin sooner this cycle due to lower yields and more expensive valuations.

We favor capitalizing on year-to-date bond strength and recommend a defensive posture consisting of short to intermediate bonds.

Last week’s Federal Reserve (Fed) news was a reminder that the Fed remains on course to raise interest rates about one year from now. The release of minutes from the July 29 - 30, 2014, Fed meeting and Fed Chair Janet Yellen’s remarks at the Fed’s annual Jackson Hole Symposium were less market friendly than anticipated. The double dose of new information from the Fed was a modest disappointment for bond investors who expected a more market-friendly tone. Bond markets remain mispriced for an eventual Fed rate hike, and last week’s rise in high-quality bond yields was a reminder of the interest rate risk facing bond investors.

A rate hike remains about one year away, according to both Fed guidance and interest rate futures markets, but it still raises the question of when bond markets will move forcefully in response to Fed interest rate hikes. Yields have declined for most bonds, year-to-date, but expectations for higher interest rates have not wavered.

When Will Rates Rise?

So when will bond yields really move in response to Fed rate hikes? Over the last 20 years, bond yields began to increase approximately four to six months ahead of the Fed’s first interest rate increase [Figure 1]. The 2-year Treasury note is among the most sensitive to Fed changes to the fed funds target rate and therefore is a useful guide to market reaction. A steadier rise in interest rates occurs once the first rate hike has passed, but in 1994, that steady rise began roughly two months before the first increase. Figure 1 shows the number of trading days, so adding back weekends gets us to calendar days and the four- to six-month period mentioned above.

The reaction among longer-term bonds, such as the 10-year Treasury, is similar but not identical. In 1994, the reaction in the 10-year yield came closer to three months prior to the Fed’s first rate hike, while in 1999 and 2004, the reaction came similarly four to six months before [Figure 2]. Like the 2-year yield, the rise in the 10-year yield was steadier just after the first rate increase in 1994 and 1999, but in 2004, a 1.0% rise in the 10-year yield was constrained to a period just before and after the first rate hike.

In 2004, the 10-year Treasury yield began to decline again despite ongoing Fed rate hikes leading a befuddled Alan Greenspan to famously label it a “conundrum.” Intermediate and long Treasury yields, however, resumed their rise in 2005, in response to continued Fed interest rate hikes before peaking in 2006.

Another takeaway from Figure 2 is that the rise in 10-year yields was more limited in time span. In 1999 and 2004, the 10-year yield peaked within one to three months after the first rate increase -- a reminder that longer-term bonds are less influenced by the Fed and more by economic growth and inflation expectations. In 1994, the 10-year Treasury yield peaked 10 months after the first rate hike -- perhaps a reflection of an aggressive and quick Fed rate hike schedule (which is not expected in the current environment) and the Fed continuing to emphasize a go-slow approach.

Caveat Emptor

Of course, every historical period is unique, reaction may not follow historical form, and investors need to beware. The prevailing environment is quite different from others and involves a range of Fed stimulus that may be halted or reversed as the Fed gradually attempts to normalize policy. Bond purchases are expected to end in October 2014, and the Fed may eventually change its guidance from being on hold for a “considerable” period to signaling that a rate hike is drawing near. Both events may act as a catalyst to higher yields.

Other Fed tools, such as paying interest on excess bank reserves and the reverse repurchase facility, cloud potential market reaction. Additionally, the latest indication from the Fed is that it may maintain an overnight interest rate range, rather than set a specific rate, which may soften the potential market reaction.

We believe the rise in interest rates may begin sooner in anticipation of an interest rate hike. Bond valuations, although off the peak of early May 2013, remain very expensive by historical comparison, and the bond market has already priced in a Fed that may take longer than anticipated to raise interest rates. Along with lower yield levels compared with history, this makes the bond market vulnerable to rising rates. Timing such a move is very difficult, even with history as a guide. We favor a defensive stance in the bond market capitalizing on year-to-date strength and positioning with short to intermediate bonds to protect against the threat of rising interest rates.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values and yields will decline as interest rates rise, and bonds are subject to availability and change in price.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by any Government Agency | Not a Bank/Credit Union Deposit

Tracking # 1-302163 (Exp. 08/15)