Janet Yellen began her prepared speech on monetary policy and the labor markets in Jackson Hole at 10:00am on Friday. Within minutes, analysts were offering insights into future interest rate policy. The equity markets dipped slightly only to recover quickly to pre-speech levels. The consensus view, which emerged after sifting through the release, was that Ms. Yellen’s view on interest rates may be a tad less dovish than previously expressed. With no video feeds emanating from the conference and with tepid market reaction, we asked ourselves, “Is she whispering or is she Yellen?”

Around 10:45am, the equity markets hit intra-day lows. Reports coming from NATO on Russian supply convoys entering Ukraine brought investors out of the myopia of monetary policy speech analysis. The equity markets ended the day lower as bonds rallied. Geopolitics once again proved that monetary policy is not the only thing affecting rates.

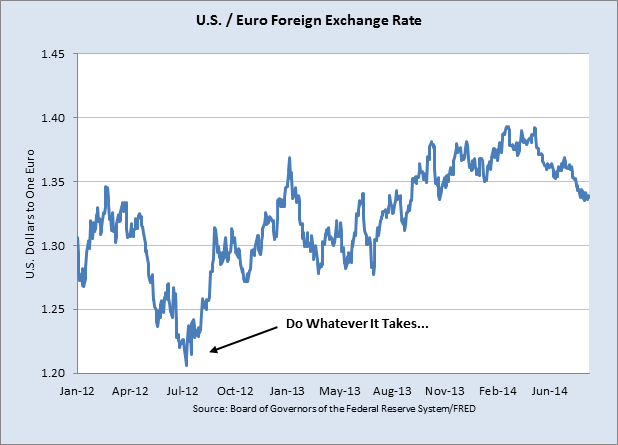

We previously discussed our thoughts on interest rates and Fed policy as well as our perspective on U.S. equity market valuations. Now as we turn to Europe, we examine the speech of Mario Draghi—the man who vowed in 2012 that the European Central Bank (ECB) would do whatever it takes to preserve the euro.

Ms. Yellen told the story of the labor market following the Great Recession and provided a few breadcrumbs as to how this narrative may unfold. Mr. Draghi presented a call to action. While Ms. Yellen has the unenviable task of dealing with the end of five years of balance sheet expansion, Mr. Draghi’s task is daunting—determining monetary policy for an 18 country monetary union. In the absence of a fiscal union, and with significant laws deterring the direct intervention of the ECB on Eurozone governments, Mr. Draghi must turn to measures less conventional than those available to The Bank of England, The Bank of Japan, or The Federal Reserve.

Balance sheet expansion has been carried through successive rounds of Long-Term Refinancing Operations (LTROs). This policy allowed the ECB to pump money into Eurozone banks to create a liquidity cushion. The ECB has created a veritable alphabet soup of policies to save the euro: Outright Monetary Policy (OMT), Targeted LTROs, and the European Stability Mechanism (ESM), which replaced the European Financial Stability Mechanism (EFSM) and the European Financial Stability Facility (EFSF). Now, along with TLTRO, Draghi is looking to buy asset-backed securities (ABS). However, Draghi emphasized that monetary policy, alone, was not a panacea for the euro zone. For Draghi, fiscal policy and national structural labor reforms must be addressed.

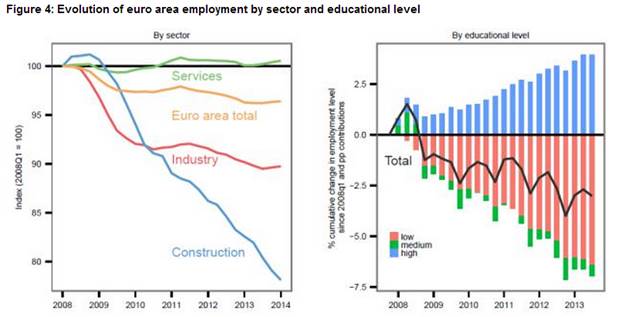

The main area where both Ms. Yellen and Mr. Draghi seem to agree is that there are structural difficulties for those who are unemployed in economies that are becoming more service oriented. While Ms. Yellen referred to the, “Phenomenon of ‘polarization’… the reduction in the relative number of middle-skill jobs,” Mr. Draghi produced charts showing the rise in need for high education level jobs as well as the declining need for low education jobs, specifically in the construction sector.

(Source: Unemployment in the euro area, speech by Mario Draghi, August 22, 2014)

Mr. Draghi emphasized the heterogeneous nature of the problem in the euro zone. He compared the unemployment rate in Germany at 5% with the unemployment rate in Spain at 25%. He discussed the response of Spain and Ireland to the Global Financial Crisis. He demonstrated that Ireland’s flexible labor market and quick adoption of structural reforms from the so-called Troika helped stabilize its recovery. He contrasted this with Spain and the inefficient labor markets that are only recently undergoing needed reformation. With the call for structural labor reforms, he backed away from certain austerity measures like high taxation and emphasized the need for others like the reduction in non-productive government expenditures, while insisting on the need for more education, job training, and economic coordination among member states.

What do heterogeneity, labor reforms, and fiscal reform mean for investors? Europe is essentially a two-speed economy, and the number of countries supporting the periphery is dwindling. In France, François Holland’s combination of excessive taxation and opulent government spending has killed growth. Germany is the last man standing, a pseudo-Atlas asked to carry the continent on its shoulders. Germany has been adamant in its opposition to quantitative easing measures and in support of government austerity. Many analysts have pointed to Draghi’s esoteric requests for Germany to do more to help the periphery.

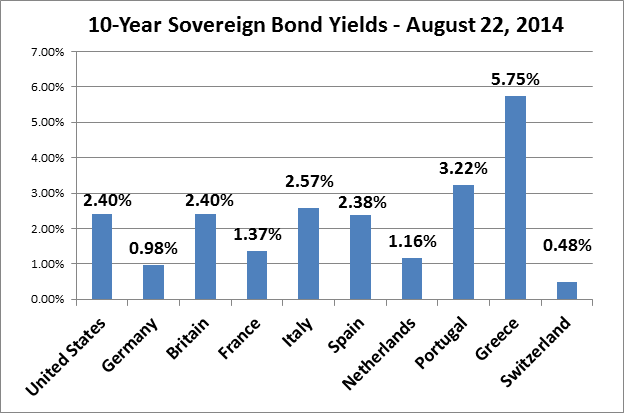

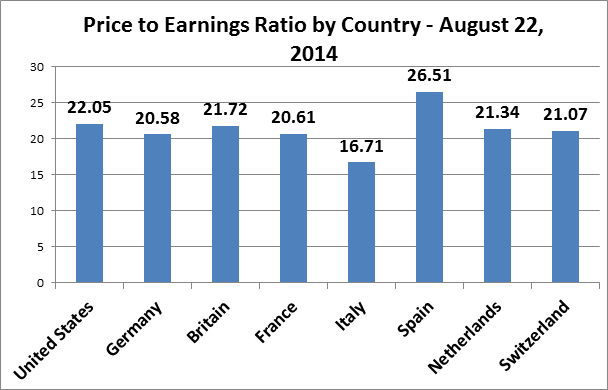

The peripheral markets, the former PIIGS—Portugal, Italy, Ireland, Greece, and Spain—have seen rallies in the equity markets disappear over the past few months, while the bonds increasingly look less attractive. The Price to Earnings (P/E) ratios are normalizing , while the bond yields range from the dismal 0.98% of Germany to the bizarre 2.38% yield in Spain (as of Friday, the BBB rated 10-year sovereign debt of Spain was yielding two (2) basis points below the AA rated 10-year U.S. Treasury).

(Source: Bloomberg)

A recent equity sell-off has occurred across the euro zone. This has brought P/E levels in tandem with the United States. However, one may wish to refer to our piece on U.S. equity valuations referenced above as well as to the last paragraph of Mr. Draghi’s piece: “The long-term cohesion of the euro area depends on each country in the union achieving a sustainably high level of employment. And given the high costs if the cohesion of the union is threatened, all countries should have an interest in achieving this.”

(Source: iShares Country ETFs):

Mr. Draghi attempted to channel the sense of leadership that followed his vow on the preservation of the euro in July of 2012. In 2012, his speech worked. The euro hit a nadir and rallied for almost two years. However, the euro like the associated equity markets appears to be in free fall. We would stay away from the euro at this level. We are of the opinion that it may be forming a base, but this base will be temporary. Our bias on the euro is towards the downside. Equity market valuations are for the most part on parity with the United States. With the recent sell-off, we think buying broad baskets of Eurozone equities as akin to trying to catch the proverbial falling knife. As a union, the U.S. appears to be addressing structural labor market reforms better than much of the euro zone.

This piece addresses the equity and bond markets in Europe following Mr. Draghi’s speech at Jackson Hole. While the prospects of the broader markets do not seem attractive, not all equities are created equal. Careful fundamental analysis may yield significant value, especially in the smaller capitalization stocks where the absence of analysts can create an information advantage. Similarly, we outline a broad stroke on 10-year sovereign bond yields. With the 10-year German Bund yielding less than one percent and Draghi’s urgent call for inflation, we believe that shorting euro-Bund futures (a bet on rising German rates) could be prudential. This piece does not discuss whether or not select sovereigns, supranational, or credit instruments may be attractive, though we plan to discuss the corporate bond market, the municipal market, and alternative investment strategies in the near future. As with equities and oft-repeated here: Not All Bonds Are Created Equal.

Good Fortune!

Bob Andres is editor of The Andres Review and founder of Andres Capital. Bob’s career includes stops as: chief investment officer at Merion Wealth Partners, chief investment strategist at Envestnet (PMC division), co-founder at Martindale Andres & Co., a firm he grew to $2.4 billion before its sale, President at Merrill Lynch Mortgage Capital, etc. He has been quoted and featured in various media: CNBC, Fox Business, Barron’s, Institutional Investor, etc.

© Andres Capital Management