Consumer Spending & Economic Recoveries: What They Mean Going Forward

As a follow-up to the discussion on the rollover of the duration of the unemployed, the byproduct of an accelerating improvement in the undercurrents of the job market is consumer spending. The measure of consumption has a primary correlation to wages and income workers receive. As such, the benign improvement in wages has an obvious correlation to the benign improvement in consumption. There is a strong secondary driver which we will discuss shortly.

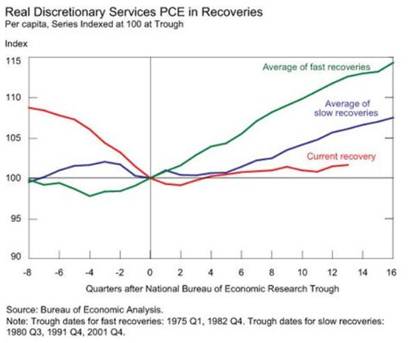

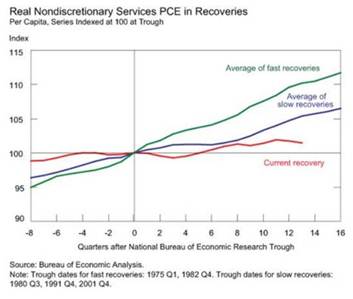

Last week the Federal Reserve of New York posted a comparison of the current recovery in discretionary and nondiscretionary Personal Consumption Expenditures (PCE) versus recent fast and slow economic recoveries.

First, we all understand that whether through quantitative analysis or just innate gut instincts, the economic recovery has been slow and steady. What the New York Fed’s charts show is a direct correlation between spending that “comes in like a lion,” and “comes out like a lamb.” The times when spending were above average, the recovery was less than what a slow recovery has looked like historically. Conversely, the slower the spending was heading into a recession relative to its average, the better and faster the recovery.

To get to the brass tax, one will look at the above charts in one of two ways.

1. The first is that this recovery is slow in the primary recovery function of recession and that is increased consumption which buoys the economy in a more accelerated fashion.

The cycle goes:

- Increased consumption leads to increased earnings

- Increased earnings leads to increased hiring

- Increased hiring leads to increased wages

- Increased wages leads to increased sentiment

- Back to increased consumption

In the current situation, we see the slower consumption rate not letting the cycle fully get started.

2. The easy (and wrong) answer is that we are perpetually stuck in this holding pattern for the foreseeable future. Though this may be correct in the current environment, the slow and steady gains in the job market should ultimately lead to a more accelerated consumption level mirroring traditional recoveries. We need to see some incremental gains as we have had in the last year to continue this.

These two charts epitomize the “glass half full vs. glass half empty” argument. The Pessimist will see this as it is as good as it gets and has nothing but downside, while the optimist will see it as a baseline from which it can only get better. I can empathize with both sides; however, when I take into consideration the following variables, it appears to me that upside outweighs the negative potential outcomes.

- Disposable Income has averaged 5.35% annually since 1946, but has averaged half of that since the end of the last recession. The short-term measures which include a weather-hindered negative GDP print in the first quarter have surged to show a YTD annualized gain of 5.05%.

- Liquidity continues to increase backstop to economic decline: household total deposits now stand at $9.783 trillion (net worth at $81.7 trillion); commercial banks hold $2.895 trillion in cash and have $1.92 trillion in excess reserves being held at the Federal Reserve. Non-financial corporations have a $19.09 trillion net worth. As well, they continue to have a positive funding gap which translates to not needing to access capital markets for funding operations.

- Leverage ratios on the household front are considerably benign thanks to interest rates and a conservative outlook; Total debt service ratio for households is at an all-time low since being measured in 1980.

Though the short-term trading pattern continues to show a range at best, the longer term fundamentals continue to show potential for growth while maintaining a positive baseline. The talks of bubbles and cataclysmic risks ranging from the apathetic investor, the Federal Reserve draining the punch bowl, geopolitical tensions and general midterm election rhetoric should – counter intuitively – be welcomed.

In my opinion, the more that talk of risks permeates conversations and headlines, the less likely a burst will take place.

CRN: 2014-0812-4363R

This commentary is for informational purposes only. All investments are subject to risk and past performance is no guarantee of future results. Please see the Disclosures webpage for additional risk information. At www.aamlive.com/blog/about/disclosures. For additional commentary or financial resources, please visit www.aamlive.com