Investing in foreign markets requires a constant questioning of many long-held assumptions that underpin traditional security analysis. This is particularly true in Asia’s bond market, where fundamental investors need to pay close attention to geographic idiosyncrasies during their due diligence process.

In this first part of our series addressing the trinity of risk and reward drivers in Asian fixed income—credit, currencies and interest rates—we will examine some complexities in credit analysis around accounting and corporate structure. In future commentaries, we will discuss the added layer of the macro-environment that comes into play when analyzing fixed income securities. Bond analysis requires not only a thorough understanding of a company’s strength, but also broader comprehension of the impact of movement in currencies and interest rates on fixed income securities.

Most aspects of credit research, such as the analysis of cash flows, liquidity, leverage and balance sheet strength, are no different in Asia than they are in any other region. However, there are other considerations that investors need to take into account to fully appreciate the inherent risks of investing in this market. For instance, applying many of the assumptions that we might implicitly or explicitly use from a U.S. GAAP-centric lens in conducting research on an Asian corporate borrower may actually lead to the wrong conclusions. So what are the pitfalls that investors need to be aware of when investing in Asian credit markets?

Because Chinese companies make up a sizeable portion of some Asian bond indices, and an even larger portion of the high-yield universe, we use specific examples of companies in China to illustrate challenges faced by investors. We also highlight three accounting and ownership structure practices that can serve as warning signs that a company’s governance may not be exemplary. The universe of Chinese issuers has grown rapidly in recent years and deepened to include both quasi-sovereign and corporate issuers. This provides us with one of the more timely examples of items faced by investors when conducting research: questions surrounding the ability to attach assets, the accuracy of Chinese accounting standards and investor rights.

While we do not profess to have all the answers, at least by asking the right questions, we can gain a better understanding of what we do not know.

Ownership Structures—Separating What You Actually Own from What You Don’t

-

Across Asia it is a “known known” that corporate ownership complexities can be significant and structures can take many forms. In China, for instance, the government restricts foreign ownership of businesses in a number of strategic industries, including1:

Wholesale and Retail Industries

Culture, Sports and Entertainment

Certain Manufacturing, including Food Processing, Beverages, Tobacco and Chemicals

Education

Financial Services

Real Estate

Scientific Research, Technical Service and Geological Exploration

Transportation, Warehousing and Postal Service

To get around these ownership restrictions, accountants and lawyers have devised a structure called the variable interest entity (VIE) to mimic economic ownership without physical asset ownership. One study found that approximately half of the Chinese companies listed in the U.S. use this type of structure, regardless of whether they need to or not.2

Despite their widespread use in China, VIEs have several risks. First, as an investor, your only asset is the contract used to provide economic ownership, and not the actual money making assets of the operating company. Second, the Chinese government has never explicitly approved the structure while local and industry regulators have selectively raised objections to VIEs. Third, given the structure’s intention of circumventing foreign investment restrictions, there are serious doubts as to their enforceability in a Chinese court. As credit investors in Asia, we look closely at corporate structures and where we find structures like the VIE, we carefully weigh the risk against the benefit of owning the company’s security.

One famous example of the inherent risk in VIE structures is the case of GigaMedia. After deciding to change its management team in China, the former head of GigaMedia’s online gaming business ran off with key documents, including the three VIE documents that the company needed to run its division in China. Without these documents, GigaMedia’s Chinese business ground to a halt. It could not enter into contracts or take any official corporate actions, including registering resolutions to remove the employee. Without the VIEs, GigaMedia couldn’t exercise control over its Chinese subsidiaries or its financial reporting process, so the company deconsolidated its results and completely wrote off its investment in those entities. The company filed lawsuits against its former employee in China, Hong Kong, Singapore and the British Virgin Islands, and eventually sold its interest in the Chinese business.

Accounting Issues—Differentiating Between Sloppy Accounting and Outright Fraud

Understanding accounting issues is also essential. While both lead to value destruction, it is important to draw a distinction between sloppy accounting and intentional fraud. Again, we use a Chinese company as an example of how ownership and jurisdiction relate to accounting fraud but highlight that such issues are common to markets across the world.

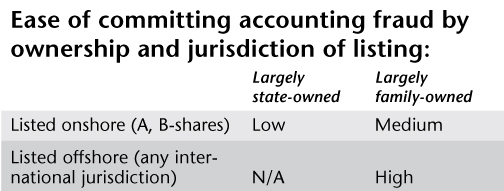

The majority of state-owned enterprises that are listed onshore have to file accounting documents with the State Administration for Industry & Commerce (SAIC), the Chinese equivalent of the U.S. Securities and Exchange Commission (SEC).

Because the SAIC has the ability to cross-reference filed accounting documents with tax records and other regulatory filings, accounting inconsistencies are relatively easy to catch. Furthermore, since it is unlikely that divergent groups of quasi-government employees will collude in order to carry out fraud at the company level, irregularities are more likely to be due to sloppy accounting than fraud.

In the case of family-owned businesses listed onshore, collusion within the same family might make fraud easier, but these businesses are listed in the same jurisdiction in which they operate, which makes cross checks of accounts possible. These companies have not only had more instances of fraud than state-run enterprises listed onshore, but they are also more likely to have instances of sloppy accounting.

The most precarious structures, however, are the family-owned businesses listed offshore. This includes businesses controlled by their founder, either through a controlling stake or a senior management position. These businesses typically require the most scrutiny; in addition to family members being able to collude more easily, the various jurisdictions, language barriers, local laws and accounting standards make it more difficult to cross check the companies. Most of the fraud uncovered in China benefited from the complexity these factors introduced. Sino-Forest, a commercial forest plantation operator, is one example that has received substantial media attention. With operations in China, a myriad of subsidiaries in the British Virgin Islands and a listing in Canada, auditing Sino-Forest’s financials and verifying its asset ownership proved to be challenging. Sino-Forest allegedly fabricated operations and used its subsidiaries to introduce complexity into the business and its accounting. Had investors focused on the movement of cash or the fact that its board was comprised of former audit partners with little experience in China, perhaps their losses could have been avoided.

As credit investors, we look for many things, including signs of leakage of cash, arrangements aimed at bypassing covenants, unusual accruals and the overall strength of corporate governance. We also help mitigate risk by ensuring that the bonds we buy are close to assets that we may have recourse to in a downside scenario.

Cross-holdings—Ownership Versus Control

There are many conglomerates in Asia, and whether they are state-owned enterprises or family-owned companies, cross-holdings among the various listed entities matter. When we look at some Chinese state-owned enterprises, for example, we find that even though the parent company may own less than 10% of a listed subsidiary’s shares, it can effectively control the entire company. How is that possible? In the hypothetical example below, parent entity A owns 50% of entity B, which owns 40% of entity C, which in turn owns 30% of entity D. The parent entity A technically only owns a 6% stake in the subsidiary entity D. But by having a blocking minority stake in entity C, which in turn has a blocking minority in entity D, the parent entity could exert undue influence relative to its small 6% ownership stake.

There are many “unknowns” in security analysis, particularly in Asia. Ultimately, we can never predict what a controlling shareholder may or may not do with related companies, but we can work to minimize the “known unknowns” by studying the specific situation in detail. As credit investors, we focus on each bond’s structure to understand the risk of an investment. We work to understand whether our bonds have recourse to the subsidiary or parent’s assets and what the recovery rate may be. We also analyze the covenants and whether they require cash to be used for some purposes and restrict it from being used for others. More broadly, we study what the track record of the controlling shareholder has been in dealing with minority investors across economic cycles.

As specialist investors in Asian credit markets, we understand what pitfalls to look for across the region. While the process of credit analysis is the same as in any market in the world, Asian credit is unique because of the challenges and opportunities it presents. We attempt to insulate ourselves from the “unknown unknowns” by focusing on the intricacies of companies and countries in the region. By knowing what we know, and knowing what we do not know, we can make more informed investment decisions. In so doing, investors who are well-versed on the region may find attractive investment opportunities in strong companies that are well-positioned in attractive Asian markets.

Satya Patel

Portfolio Manager

Matthews Asia

1 Catalogue of Prohibited Industries for Foreign Investment, BusinessForumChina, January 30, 2012

2 “Statistics on VIE Usage,” China Accounting Blog 2011

As of 8/15/2014 accounts managed by Matthews Asia did not hold a position in GigaMedia or Sino-Forest Corporation. Sources: Morrison and Foerster, August 15, 2013 “China VIEs: Recent Developments and Observations, Impact on Cross-Border Transactions,” by Charles Comey, Paul McKenzie, Sherry Yin and Michelle Yuan; Topics in Chinese Law, October 2011, “VIE Structures in China: What You Need to Know,” by David Roberts and Thomas Hall; Bloomberg, May 23, 2012, “Sino-Forest Engaged in ‘Fraudulant Scheme,’ OSC Alleges,” by Christopher Donville and Liezel Hill; Muddy Waters Research, June 2, 2011 Sino-Forest Report, Director of Research: Carson C. Block, Esq.

The views and information discussed in this article are as of the date of publication, are subject to change and may not reflect the writers' current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of any securities or any sectors mentioned herein.

The subject matter contained herein has been derived from several sources believed to be reliable and accurate at the time of compilation. Matthews International Capital Management, LLC does not accept any liability for losses either direct or consequential caused by the use of this information.