The hospital industry has traditionally been below average from an investment standpoint, given its high levels of regulation, capital intensity, and leverage. Pricing power with private insurers is dependent on local market share, while Medicaid and Medicare rates are non-negotiable. Over 80% of hospitals are non-profit, further limiting the potential for sustainably outsized margins. In short, these are investments for which we require a deeper discount to our estimate of the company’s intrinsic value (i.e. a wider margin of safety). Despite these dynamics, certain companies have proven adept at producing operating efficiencies or have carved out more attractive niches. One such business is LifePoint Hospitals, Inc. (LPNT), a rural hospital operator with dominant market share, attractive capital deployment opportunities, and an improving payor mix driven by the Affordable Care Act (ACA).

Despite vitriolic headlines, the ACA’s actual financial implications for healthcare companies are fairly clear. There are both positives and negatives for hospitals. On one hand, Medicaid expansion and commercial insurance exchange subsidies will reduce bad debt from the uninsured. On the other hand, reform embraces cost containment efforts such as accountable care organizations and high deductible plans, accelerating a pre-recession trend away from expensive inpatient settings to cheaper outpatient facilities. While the improving payor mix dominates the short-term outlook, patient shifting will remain an issue once the dust from reform settles. We believe LifePoint should disproportionately benefit from bad debt reduction while being comparatively insulated from cost pressure.

LifePoint was spun-off from HCA Holdings, Inc. in 1999. Its management team and Board are known for their patient and conservative culture, which is reflected in its balance sheet. LifePoint has also managed to avoid the recent investigations into aggressive coding practices faced by many of its peers. Being a rural operator is a double-edged sword. Labor force participation has been declining for much of rural America since the recession, and although markets are slowly recovering, weak wage growth has curtailed any bounce-back in private volumes. While urban counterparts are benefitting more quickly from the recovery, they face long-term competitive threats from cost transparency. Consumers are increasingly utilizing pricing apps and are more tolerant of narrow networks. Accordingly, non-profits and cheaper alternative settings such as outpatient clinics and diagnostic labs may pressure volumes. Here, LifePoint has an edge; the company is the sole provider in the vast majority of its markets. The next three years should see additional improvement from reform, and beyond that point, the lack of competition makes margin retrenchment less likely.

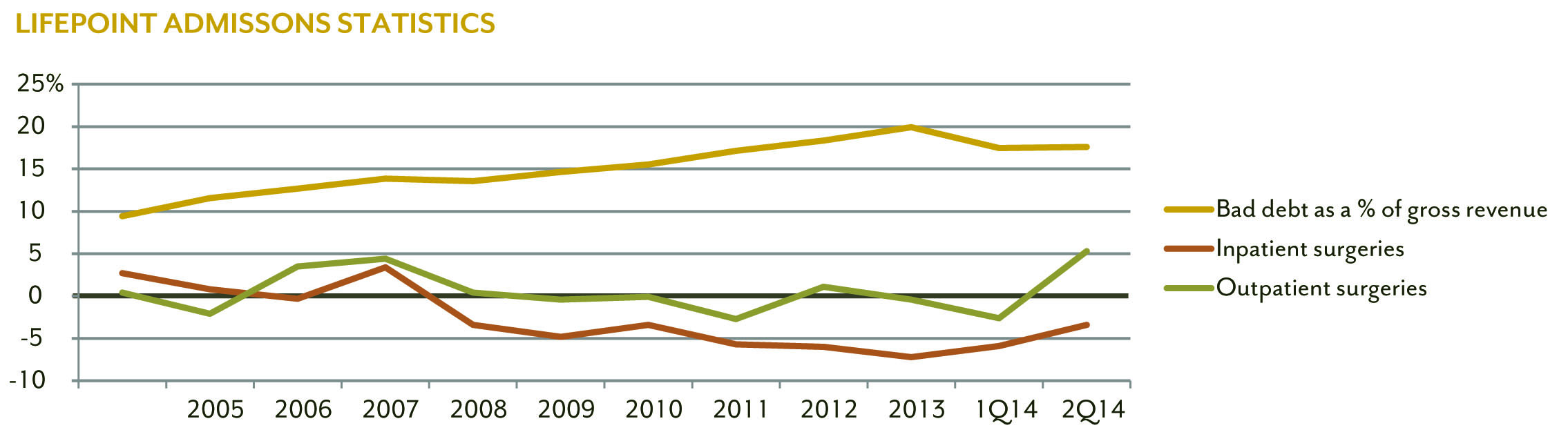

Note: Inpatient and outpatient surgeries are year-over-year same-hospital figures. Bad debt is adjusted to include charity care write-offs.

Source: Company documents

Tuning out the static over the initial healthcare exchange rollout and poor weather last winter, we examined LifePoint’s markets on a state level. Nearly 45% of the company’s beds were in states expanding Medicaid, and given the lower income profile of most rural areas, a large percentage of their uninsured patients (8% of total admissions) were eligible. Unlike commercial exchanges, Medicaid enrollment appeared to be moving along at a brisk pace, particularly in Kentucky, one of LifePoint’s largest states. We discussed outreach efforts with management and were impressed with their comprehensive plan to target LifePoint’s most frequent uninsured patients. Soft volumes appeared to be adequately priced into the stock, but the company was not receiving credit for their improving payor mix. During the second quarter call, management stated uninsured volumes declined by 67% in Medicaid expansion states, with the fiscal year 2014 benefit from the ACA expected to approach $50 million in earnings before interest, taxes, depreciation, and amortization (EBITDA) off a base of approximately $560 million.

LifePoint’s capital allocation is split between acquisitions and opportunistic share repurchases. The company’s new CFO, Leif Murphy, aggressively repurchased shares last winter when investors had unfounded concerns over exchange enrollment. The company has bought back $165 million in stock year-to-date, reducing share count by 5% versus the second quarter of 2013. We believe this was a prudent and timely use of cash given our view that the stock was undervalued.

M&A, the other use of capital, is a major source of growth for hospital systems. LifePoint has a unique advantage via a joint venture formed in 2011 with Duke University Health System, with the goal of building regional networks in growing, higher income rural markets. LifePoint takes the dominant financial stake (80%+), while Duke lends its clinical expertise and brand for the remaining interest. Hospitals are the largest employer in many rural communities in addition to being the sole medical provider. As such, an acquirer’s financial solvency and clinical support capabilities are the key factors when deciding between multiple bidders. Duke’s brand is also a way to stem patient outmigration. Rural hospitals suffer from the perception that they lag behind larger systems in areas such as robotic surgery, with higher acuity patients choosing to travel to urban systems for procedures. The combination of LifePoint’s capital investments and Duke’s clinical expertise will help convince the most lucrative patients to receive care locally.

We believe LifePoint’s strong free cash flow, flexible balance sheet, and conservative culture create adequate downside protection. These attributes, combined with LifePoint’s improving payor mix, dominant market share, and unique M&A strategy have the company well positioned for the reform era. Since the beginning of the year, shares have appreciated considerably and now appear to credit the company for its improving mix. We continue to see upside from stronger volumes, acquisitions, and Medicaid expansion in additional states.

The views expressed are those of the research analyst as of August 2014, are subject to change, and may differ from the views of other research analysts, portfolio managers or the firm as a whole. These opinions are not intended to be a forecast of future events, a guarantee of future results, or investment advice. DIAMOND HILL® is a registered trademark of Diamond Hill Investment Group, Inc.

© 2014 Diamond Hill Capital Management, Inc. All Rights Reserved.

© Diamond Hill Capital Management