Retail sales in the US were unchanged in July, which prompted us to dive into our chart library to figure out what may be going on underneath the surface of the economy. Job growth has been pretty solid this year, which when combined with increases in hours worked, has led to a an almost 4% year over year increase in personal income. So what gives?

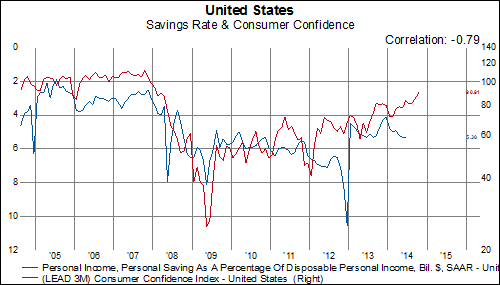

Answer: The savings rate has been rising all year. In December 2013, the savings rate was 4.1% and by June 2014 it had risen to 5.3%. An increase in the savings rate is a headwind to consumption and in turn GDP growth. What's interesting is that all year, while the savings rate has been increasing, consumer confidence has been increasing too. In the chart below, we plot the savings rate (inverted) against the US consumer confidence index.

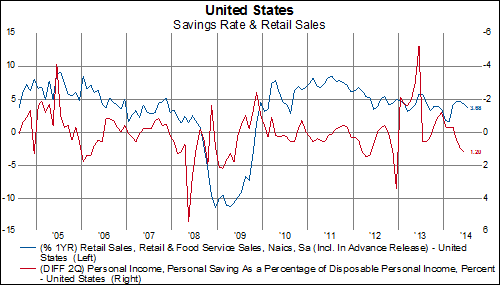

The second derivative of the savings rate on a six months basis is +1.2%. In the chart below, we plot the momentum of the savings rate against the year over year increase in retail sales. The notch down in retail sales growth is understandable given the change in consumer behavior toward greater savings.

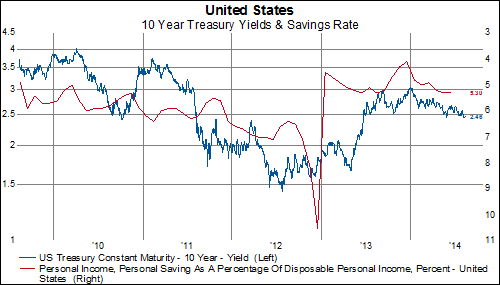

The increase in the savings rate is an important consideration when looking at interest rates. In the chart below, we plot the savings rate against 10 year US Treasury bond yields. While not a perfect overlay, the general relationship is apparent--a rising savings rate corresponds to falling interest rates. Perhaps this change in consumer behavior is what the bond market is responding to... not a fluky 4% growth quarter, where a third of the increase was inventory accumulation anyway. July retail sales data would suggest the inventory accumulation in the second quarter was the unwanted variety.

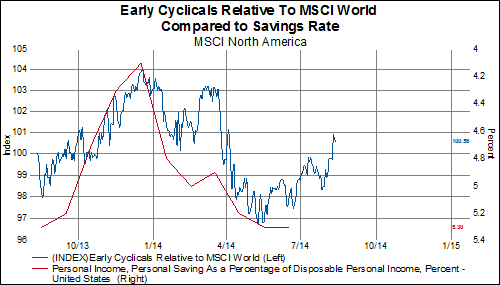

Over the last year, the savings rate has corresponded pretty well to the relative performance of the MSCI North America consumer discretionary sector. In the back half of 2013, while the savings rate fell 1.2% percentage points, consumer discretionary stocks in North America outperformed. In the first half of this year, as that trend reversed, so did relative performance. Perhaps the relative performance of consumer discretionary stocks over the last month has signaled a falling savings rate in the back half this year, or perhaps the drop in retailers today suggests the market is incorporating a more negative view of consumer behavior in the second half of the year.