- Global Risk Aversion Lifts Municipal Market

- Geopolitical risks threaten global financial recovery

- “Good news” now “bad news” for stocks

- Municipal bond yields dragged lower by U.S. Treasury safe haven trade

- Municipal market technicals will continue to support market

The U.S. economy continues to accelerate. Employment growth is strengthening; over 200,000 jobs are now being created every month, helping to push the unemployment rate down to almost 6%. A surprisingly strong 4% gain in second quarter GDP more than offset the first quarter’s 2.1% contraction. Corporate America reflects the improving macro fundamentals. Second quarter corporate earnings were better than forecast. Unfortunately for stock investors, the normal positive correlation between economic growth and equity performance has derailed. “Good news” is now interpreted as “bad news,” as evidenced by the sharp decline in global equity markets over the past few weeks; many indices have relinquished their gains for the year. Investor bullishness is being reconsidered.

Besides accelerating economic growth, recent higher labor cost readings have added to the unease. There is growing concern within the financial markets that policy makers are behind the curve and the Fed will be forced to play catch-up by raising rates sooner than forecast. The Fed remains the primary driver of the economic recovery by maintaining short-term interest rates close to zero and making large purchases of Treasury securities for its own account. The central bank is preparing to conclude its debt purchasing program in October. Now a growing consensus believes the Fed’s hand will be forced on rates, and the first move will occur in early 2015 if wage costs move higher and the unemployment rate drops below 6%.

Normally, bond prices should be expected to decline given the degree of economic strength. To the contrary, debt markets are not faltering. In response to heightened international risks, U.S. Treasury yields declined last week to their lowest levels in over a year.

So, why are stocks and bonds behaving contrary to rational expectations? Geopolitical concerns are exhibiting much greater financial market influence than the underlying economic fundamentals. International unrest has caused stock prices to plunge and bonds to rally. The potential fallout from the latest sanctions levied against Russia could significantly alter global growth, especially in Europe, which is struggling to maintain its economic equilibrium. The latest announced sanctions are quite severe and retaliation from Moscow should be a concern. The impact on European business could be significant and might possibly get worse if Russia elects to curtail exports of natural gas in addition to recently imposed food and agriculture sanctions. The European economy is not as strong as perceived. Double-digit unemployment persists in the Euro area. The European Central Bank has added more monetary stimulus; meanwhile Italy’s economy has fallen back into recession. Global markets are exhibiting legitimate nervousness over escalating tensions with Russia, and more recently Iraq.

Geopolitical risks and the potential for more global economic weakness should stay the Fed’s hand. The resumption of U.S. military intervention in Iraq has further unnerved markets. Our interest rate outlook remains unchanged, and we are maintaining our view that the Fed will not accelerate its timetable on moving short-term rates. Janet Yellen, the Fed Chair, has reasserted her commitment to maintain current policy for a “considerable time.” She has noted the existence of excess slack in the labor force, evidenced by negligible wage gains and the large number of recently employed people who are only working part-time. The recovery in housing has been a key factor sustaining the economic rebound. Recent data suggests sales are softening in some regions. The combination of declining stocks and weaker housing could negatively impact consumer confidence. The Fed should be concerned about the ability of consumers to sustain their current spending levels.

With geopolitical risks intensifying, investors are opting for safe havens such as U.S. Treasury securities. Bond yields should not be expected to significantly increase anytime soon, at least as long as international tensions remain elevated. Since we do not anticipate a meaningful upward move in Treasury rates, municipal bond prices should also benefit. Yields are likely to remain close to current levels and even possibly move lower. Strong market technical factors will also provide support.

As has been the norm all year, fewer bonds are being sold by tax-exempt issuers. This condition has created a supply/demand imbalance. Bond sales for 2014 are now estimated to be only $300 billion, 7% below the previous year. More importantly, net new issuance supply is predicted to be negative, meaning more bonds are being retired than issued in the market. The improving U.S. economy is positively impacting state and local government coffers. Higher tax receipts have reduced borrowing needs. Sources report there is still plenty of investible cash on the sidelines, ready to be redeployed into the market. Secondary market trading activity also remains very light and below levels generated in previous years. A shortage of securities, continued strong investor demand, and plenty of available cash from August bond maturities should combine to keep the municipal market well-supported.

Many mutual funds added to their cash reserves last month in anticipation of a possible wave of shareholder redemptions. Concerns about the latest developments involving Puerto Rico debt resulted in an investor exodus from some long-term and high yield funds. Fortunately, the anticipated outflows did not materialize to a significant degree, and funds are the recipients of investors’ cash. Over the past four weeks, tax-exempt funds have received an average of over $500 million per week. Continuing equity weakness might induce investors to shift more stock assets to bonds, which would boost the amount of money to be deployed. Yields could continue to drift lower.

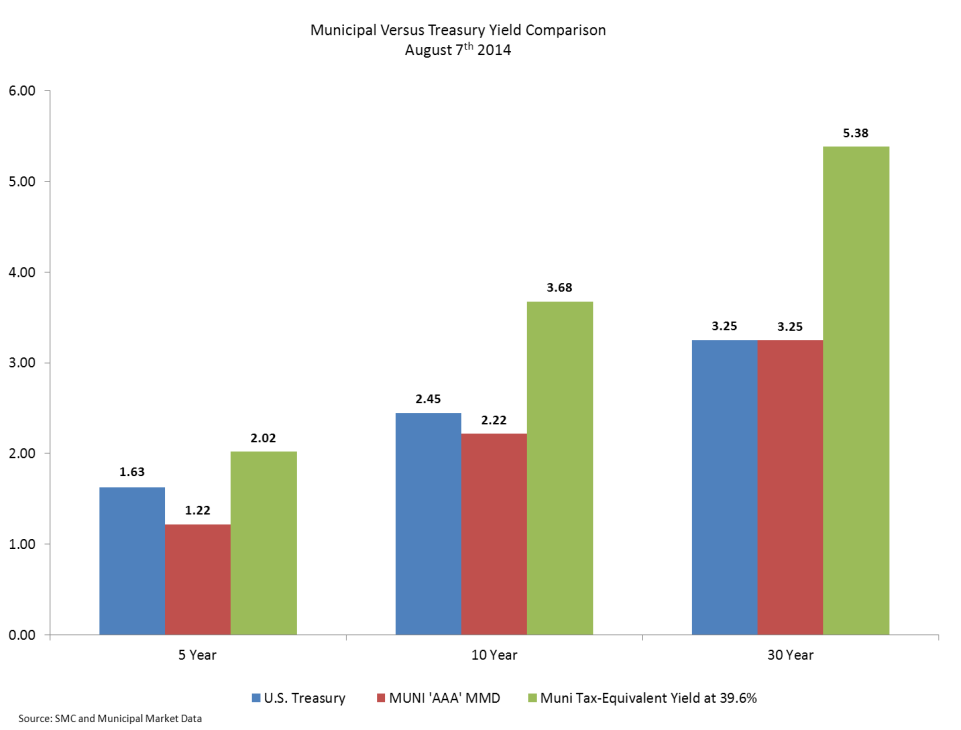

While municipal performance has been solid, Treasuries are posting even stronger returns as the international picture gets more precarious. Tax-exempt securities remain an attractive purchase relative to Treasury obligations, particularly further out on the maturity spectrum. Thirty-year “AAA”-rated tax-exempt municipal bonds can be purchased at the same yield (3.25%) as an equivalent maturity Treasury bond. On a “taxable equivalent basis,” a 3.25% tax-exempt yield adjusted for the highest federal tax rate plus healthcare surge (43.4%), equates to a 5.74% taxable yield.

Given the significant slowdown in general market trading activity, Puerto Rico issues have been receiving extra attention lately. Following the passage of the island’s restructuring legislation (Recovery Act) in late June, trading in Puerto Rico issues has been robust. After an initial sell-off, the market for Puerto Rico bonds has stabilized and yields have edged lower. In the absence of any new market-impacting developments, trading should subside and prices stabilize. There continues to be a large number of both buyers and sellers of the Commonwealth’s bonds. We are selectively purchasing insured credits due to the generous yield pick-up and security afford by the insurance guarantors.

Despite the potential restructuring of some speculative-rated Puerto Rico bonds, the high yield tax-exempt sector continues to be one of the strongest market performers, as evidenced by the 8.50% return this year registered by the Barclays Municipal High Yield Index. The rest of the high yield muni market has not been affected by the sell-off in Puerto Rico credits. With yields on higher-grade municipals still near generational lows, investors are stretching for the extra yield provided by lower- quality bonds. Municipals rated below investment grade are also getting a boost from a 50% drop in new high yield issuance this year, which is greater than the issuance contraction in higher quality credits.

Heightened international unrest and the likelihood of accelerating economic weakness in Europe will provide further support for fixed income securities. It is unlikely central banks will move from their current accommodative monetary positions anytime soon. We maintain our constructive municipal bond market view.

smcfixedincome.com/

Disclosures

The information provided in this commentary is not intended to be a complete summary of all available data. Certain information contained herein has been obtained from published sources and/or prepared by sources outside SMC Fixed Income Management (“SMC FIM”), a division of Spring Mountain Capital, LP, and certain information contained herein may not be updated through the date hereof. While such sources are believed to be reliable, no representations are made as to the accuracy or completeness thereof by SMC FIM or any of its respective affiliates, directors, officers, employees, partners, members or shareholders, and none of the former assumes any responsibility for the accuracy or completeness of such information. Nothing contained herein shall be relied upon as a promise or representation as to past or future performance.

This commentary does not constitute an offer to sell or a solicitation of an offer to purchase securities, or any other product sponsored or advised by SMC FIM or its affiliates, nor does it constitute an offer or a solicitation to otherwise provide investment advisory services. It should not be assumed that any of the securities transactions listed was or will prove to be profitable, or that the investment recommendations we make in the future will be profitable.

Statements contained in this commentary that are not historic facts are based on current expectations, estimates, projections, opinions and beliefs of SMC FIM. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Unless specified, any views reflected herein are those of SMC FIM and are subject to change without notice. SMC FIM is not under any obligation to update or keep current the information contained herein.

This commentary does not take into account any particular investor's investment objectives or tolerance for risk. The information contained in this commentary is presented solely with respect to the date of its preparation, or as of such earlier date specified in it, and may be changed or updated at any time without notice to any of the recipients of it (whether or not some other recipients receive changes or updates to the information in it).

No assurances can be made that any aims, assumptions, expectations and/or objectives described in this commentary will be realized. None of the authors, SMC FIM or any shareholders, partners, members, managers, directors, principals, personnel, trustees or agents of any of the foregoing shall be liable for any errors (to the fullest extent permitted by law and in the absence of willful misconduct) in the information, beliefs and/or opinions included in this commentary or for the consequences of relying on such information, beliefs or opinions.

Neither this commentary, nor any of the contents hereof, may be reproduced or used for any other purpose, or transmitted or disclosed in whole or in part to any third parties, in each case without the prior written consent of SMC FIM.

Copyright © 2014 Spring Mountain Capital, LP. All rights reserved.