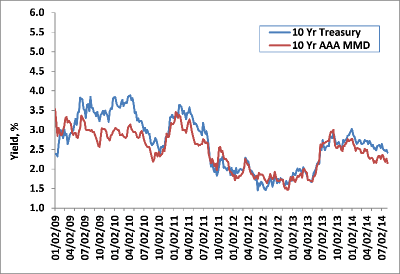

In a week devoid of meaningful economic data, financial markets were once again led by intensifying geopolitical events. With stock indices across the globe recording losses of 1%-3% on the week, US ten year yields declined to a low of 2.35% on Friday—a new low for 2014 and the lowest such point since June 2013. Since the onset of the Ukraine crisis in February, and later followed by the Iraq/ ISIS and the Israel/ Gaza conflicts, global sovereign yields have declined to levels unthinkable at the turn of the year.

Despite dropping nearly 15 basis points on the week, ten year US Treasuries look relatively attractive when measured against other industrialized nations like France (1.45%), Germany (1.05%), and Japan (0.50%).

Weekly Change: 10Y Treasury Yields vs. 10Y AAA MMD

Source: Bloomberg, Thomson Reuters and Castleton Partners

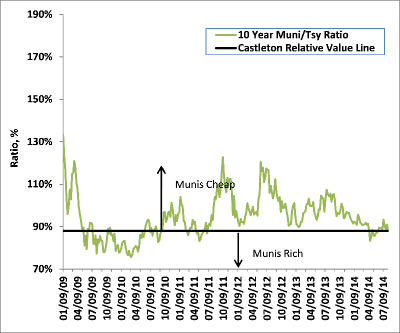

Ratio of 10Y Muni Yield to 10Y Treasury Yield

Source: Bloomberg, Thomson Reuters and Castleton Partners

Tax-Exempt

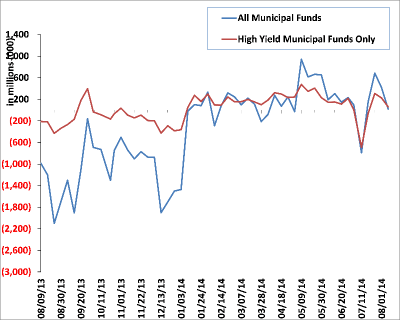

The municipal market registered another strong week—further adding to an already impressive 2014, as intermediate benchmark yields fell 9 basis to yield 2.15%. Last week’s limited offerings of new supply ($5B) was meet with strong investor demand, fueled by the strength in Treasuries and sizable reinvestment monies from August 1st coupon and maturity payments. New subscriptions from mutual funds recorded just +$19 million of net new flows. Though slowing as well, high yield tax exempt funds continue to outpace the broader muni fund categories with +$60 million of new money.

With primary supply down nearly 25% so far in 2014, secondary activity in the muni market continues to exhibit aggressive bidding: longer dated maturities have been the most sought after and credit spreads are narrowing. Thursday’s activity alone recorded over $11.7 billion in trading activity (MSRB), the highest such level in nearly a month. The sizable outperformance to date in credit is best measured by the Barclays Muni Index and its returns by rating category: AAA (4.71%), AA (6.03%), A (7.39%), and BBB (10.39%).

Attention on all things Puerto Rico continues, especially for investors in power authority bonds (PREPA) and next week’s key date of August 14th, when PREPA’s $600 million in outstanding bank lines of credit are due. As for the Puerto Rico economy at large, the Treasury reported that July’s revenues—the first month of fiscal year 2015—totaled $624 million; exceeding July 2013’s revenue by $129 million (26%). The number exceeded budgeted estimates by $37 million. Sales and use taxes, those revenues which are used to support Cofina debt, rose by 5.7% relative to one year ago.

Supply this week is expected to total over $6.5 billion, with refunding deals accounting for nearly 60% of total supply. New York leads all states, with two sizable loans: $900 million New York City GO’s (Aa2/AA) and $835 million Port Authority of NY & NJ (Aa3/AA-).

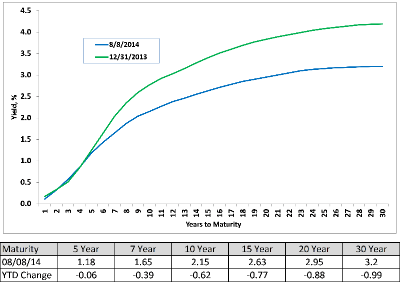

AAA Municipal Market Data (MMD) Yield Curve

Source: Thomson Reuters

Weekly Municipal Mutual Fund Flow Data

Source: Lipper AMG Data

Taxable

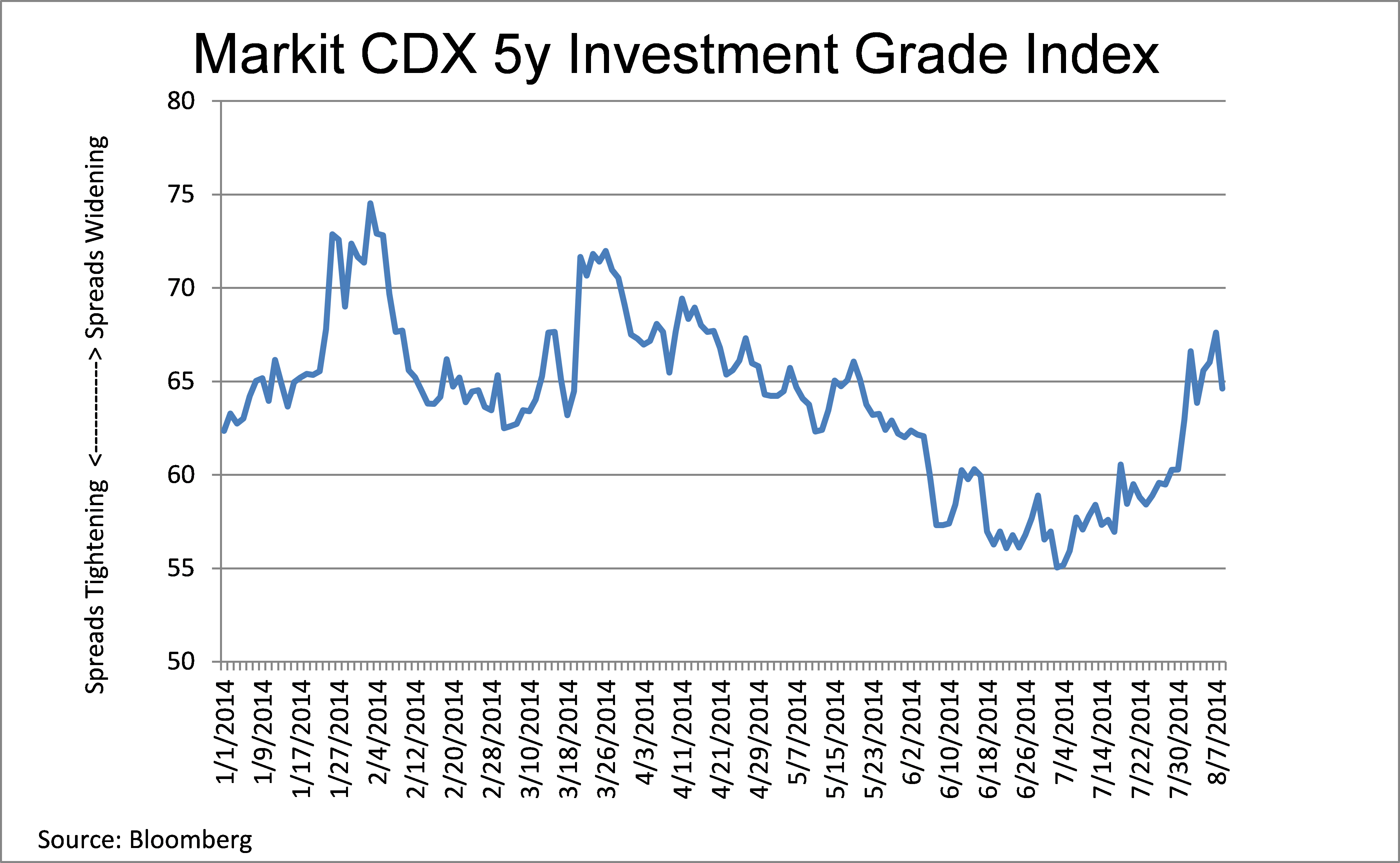

With risk-off sentiment negatively impacting returns and asset flows in equities and high yield, investment grade bonds held up relatively well last week, with spreads widening 5 basis points relative to Treasuries. Spread widening was consistent across all sectors and maturity points. With high grade spreads backing up over the last few weeks to levels last seen in April, things appear calm when measured against taxable high yield. Spreads in high yield have ballooned out nearly 90 basis points since mid-July, as equity volatility and investor uncertainty has increased substantially. As for fund flows, high grade flows remained positive at +$139 million, while high yield funds recorded their largest weekly withdrawal ever, at -$7.1 billion. Even loan funds—long a darling of front end investors—recorded their largest weekly withdrawal (-$1.5b) since August 2011. Domestic equities saw over $18 billion leave the mutual fund space.

Corporations, taking advantage of the sharp drop in rates, nearly tripled supply from the prior week, issuing $25 billion of new debt. Longer dated issuance, namely 10 year and 30 year, dominated the calendar, accounting for over 48% of supply. Citibank (3y +72), Berkshire Hathaway (5y +50), PG&E (30y +110) and Union Pacific (30y +100) were last week’s highest profile issuers.

© 2014 Castleton Partners, LLC. All rights reserved.

THE FOLLOWING NOTES AND DISCLOSURES ARE AN INTEGRAL PART OF THIS REPORT: Past performance is not a guarantee of future results. Different investments involve varying degrees of risk, including the risk of illiquidity and the risk that you could lose part or all of your investment. There can be no assurance that the future performance of any specific investment, investment strategy, or product (including those discussed herein or recommended or undertaken by Castleton Partners, LLC) will be profitable, equal any corresponding indicated historical performance, be suitable for your portfolio or individual situation, or prove successful. Charts, graphs and indices are included herein only for reference and do not constitute forecasts of the past or predicted future performance of any investment. Indices are not investments. Due to changing market conditions and other factors the content herein may no longer reflect Castleton Partners, LLC’s current opinions or positions. Nothing discussed herein is or is intended as tax, legal, accounting or personalized investment advice from Castleton Partners, LLC. Should you have any questions regarding the applicability of any specific issue discussed herein we encourage you to consult competent advisers of your choosing. Nothing herein is or is intended as an offer to sell or a solicitation of offers to buy any security. Castleton Partners, LLC’s current written disclosure statement including discussion of our advisory services and fees is available upon request.