Key Points

- Equities have continued to grind higher as earnings season has been largely better than expected. However, with sentiment in the extreme optimism zone and the late summer void in full force, risks of hitting an air pocket are elevated, much as we saw recently.

- Economic growth rebounded sharply in the second quarter, and now we should get a better view on "trend" growth. The Federal Reserve maintained its tapering of quantitative easing, but with labor market conditions getting tighter, inflation could become a bigger concern if wage gains pick up.

- The European economy has worsened, with recent German data adding to the angst. But China's improved performance bolsters our view that Chinese equities remain quite attractive for a risk tolerant investor.

We are entering one of the traditional biggest seasonal voids. The Fed won't meet again until September, U.S. legislators are going on recess, European politicians and citizens en masse go on vacation, and Americans squeeze in their last trips before school begins. This often results in lower trading activity, which would argue for a low-volatility, low-drama market environment to persist near-term.

The market seems to have a binary feel to it; with the possibility of a pullback near-term elevated; but with an equally possible "melt-up" developing. Much of the good news appears to be reflected in stock prices that are hovering around fair value. But the Fed is further along on its path toward monetary policy normalization, which has historically brought some market volatility. In addition, any disappointing economic data, a continued escalation of geopolitical issues, renewed debt concerns in Europe, Chinese growth worries, or a host of other issues could ignite nervousness. Investors worried about such a possibility may want to consider the various protective portfolio strategies available in order to hedge against some of the downside risk, but we don't recommend trying to time the market and we remain optimistic over the medium-to-longer term.

Steady as she goes

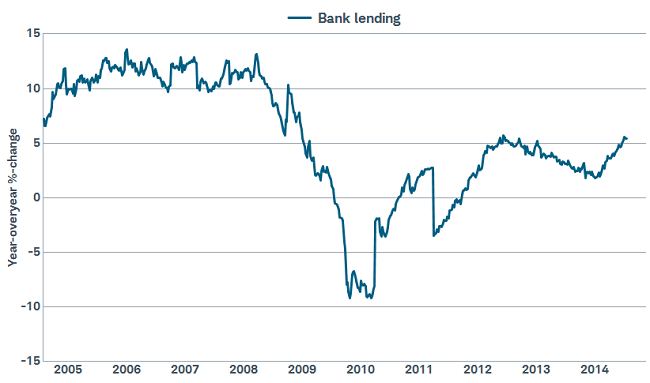

Our economic outlook underscores why we continue to believe stocks will move higher over the intermediate and longer term. Second quarter real (inflation-adjusted) gross domestic product (GDP) rebounded to an above-consensus 4.0% annualized growth rate, while the disappointing first quarter reading was revised from -2.9% to -2.1%. Both readings are likely anomalies to some degree, with the third quarter looking to be more of a "clean" reading on the underlying trend. However, it's encouraging that in addition to the positive revision to the first quarter, the final two quarters of 2013 were also revised nicely higher. Growth continues, but not at such a rate as to push the Fed to accelerate their normalization process, leaving us with abundant liquidity. This continues to be illustrated by robust merger and acquisition activity and near-record low interest rates around the world as large cash piles have to find a place to land. We are encouraged that this liquidity appears to be starting to work its way through the economy—particularly lending growth having picked up sharply—which should lead to the velocity of money, and economic growth, improving.

Bank lending indicates more money being put to work

Source: FactSet, Federal Reserve. As of July 26, 2014.

Improving corporate confidence has also resulted in the labor market continuing to improve. According to the Bureau of Labor Statistics, 209,000 jobs were added in July, a bit lower than expectations but the previous two months' gains were revised slightly higher, while the unemployment rate ticked up to 6.2% from 6.1% as the participation rate inched higher. Although it's still too early to see a definitive trend in wages, we are seeing growing stories of workers finally getting increases after several years of no growth, which should help to increase spending, and further ignite a self-sustaining economic expansion.

In contrast, the housing recovery has taken a breather, with June existing home sales rising 2.6%;, but new home sales falling 8.1%, while May's sharp increase was revised downward. After two years of almost unimpeded growth, some housing metrics have stumbled. Post-bubble adjustment processes typically are bumpy, but with affordability still high and inventories still low, we think the risk of another major pullback in housing is relatively low.

QE nearing its end, what's next?

With the labor market improving, the Federal Reserve continued to pare back its bond buying program known as Quantitative Easing (QE), with the end forecasted to come in October. With that baked into expectations, attention is now squarely on the next step and when that first interest rate hike will occur. Fed Chairwoman Yellen seems set on assuring the markets that the first hike won't likely occur until sometime in mid-2015. However, comments from some Fed members as well as signs of growing inflation indicate hikes could come sooner than expected. If that is partly triggered by an inflation scare, we believe it would be a short-term phenomenon. In fact, history has shown that stocks traditionally do quite well in the months leading up to and immediately following the first rate hike in a tightening cycle.

Investors have probably heard more about tax inversions in the last month than in the previous decade as the noncompetitive U.S. corporate tax code comes to light. Instead of making the tax code more competitive globally, the initial response was to try to enact laws to make it more difficult for companies to pursue this strategy—not exactly the business friendly approach we would like to see. But with midterm elections just around the corner now, it seems unlikely that anything of substance will be passed. So it looks like we'll be into 2015 before any remedy to this situation has a chance of coming to fruition.

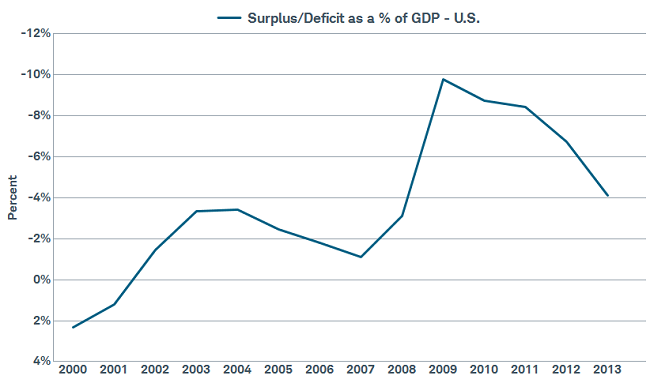

Perhaps in spite of Washington, as opposed to credit to lawmakers, the budget deficit has improved markedly, with 2013 having shown the biggest improvement in history. This is a baby step toward solving our country's longer-term debt problems, but it's a step nonetheless. Unfortunately, the pace of improvement is likely to fade and there remain serious structural issues—like entitlement reform—that need to be addressed.

It's something—deficit improves

Source: FactSet, U.S. Congressional Budget Office. As of July 26, 2014.

Europe: sentiment waning

In contrast to the United States, the prolonged stagnation in the eurozone is weighing on confidence and threatens to create a negatively self-fulfilling cycle. Declining German business confidence about future conditions, which has fallen from 108.2 in February to 103.4 in July, could restrain investment and hiring, diminish consumer spending and further weaken economic activity. Europe's leading economic indicators have started to stall, dragged down by what was assumed to be the strongman of Europe—Germany. At nearly 30% of eurozone GDP—what happens in Germany, matters for the region.

A closer examination of German exports, a key factor for the euro zone economy, shows numerous impediments to trade this year: U.S. weather in the first quarter, a Chinese shadow banking crackdown in the first quarter, Japan slowing in the second quarter as the sales tax was increased, and a strong euro. Geopolitical risks have intensified the dour mood of businesses. Notably, over 6,000 companies are active in Russia according to Reuters; and the Committee on Eastern European Economic Relations, a German industrial group, has said that the crisis could endanger up to 25,000 German jobs. Continued loopholes for Russia mean the new sectoral sanctions could remain ineffective in convincing Russia to de-escalate, sustaining an uncertain environment for businesses with ties to Russia.

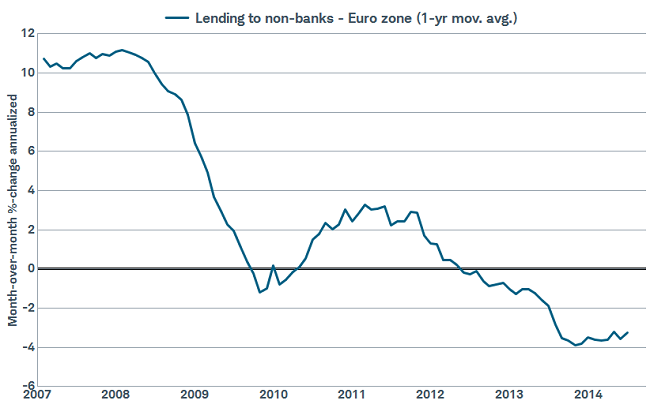

A bottoming in eurozone lending?

Source: FactSet, European Central Bank. As of July 28, 2014.

Amid the negatives, there are areas of support. Lending may be bottoming, as eurozone banks have been deleveraging ahead of the European Central Bank's (ECB) examination of bank balance sheets. A slower rate of decline in credit could gradually reduce a hindrance to economic growth. Additionally, the euro has fallen; which if sustained, could improve demand for exports, as well as corporate earnings, and diminish the drag on inflation. The ECB said the increase in the euro from 1.319 to 1.391 in the 14 months to March 2014 reduced inflation by 0.4%. The ECB has the option of eventually making outright bond purchases. But absent a significant downside threat to growth or inflation, we believe the ECB will wait to measure the effects of the Targeted Long-Term Refinancing Operations (TLTRO), which don't take effect until September.

The September 18 poll in Scotland to consider splitting from the United Kingdom could begin to garner attention. If Scotland voted to secede, this could create market volatility and threaten the UK's European Union (EU) membership. However, we believe there are significant hurdles; including uncertainty about Scotland's currency, EU membership, potential high debt-to-GDP, and fiscal deficits that could reduce support for full independence.

The near-term could continue to be difficult for European equities due to continued uncertainty with Russia. However, we believe the eurozone is on the mend and remain positive on European equities longer term.

China's stability excites some, concerns others

China's economic stabilization is a positive development for the global economy. Second quarter GDP improved slightly to 7.5% from 7.4%, as a result of a number of targeted stimulus measures: increased railway spending, accelerated full-year spending by local governments, an easing of credit issuance due to targeted reserve requirement rate (RRR) cuts for qualified banks, and changes to the way loan-to-deposit ratios are calculated. This has resulted in upside economic surprises, and prompted some economists to raise their GDP forecasts for 2014.

Accelerating credit issuance, however, is the source of both optimism and skepticism. Total credit as measured by total social financing grew 40% in June relative to May, and likely bolstered business confidence and reaccelerated spending. However, we are concerned about the tilt toward shorter-term and shadow financing. Of the 1.97 trillion yuan ($318 billion) of credit issued in June, 75% was shorter maturity—typically less linked to longer-term investment and more toward short-term cash flow needs. Non-bank sources, commonly referred to as the shadow banking system, accounted for 45% of total credit, up from 38% in May.

Another recent boost to China's growth—an increase in government spending—was driven by the central government, which surged 14.6% year-over-year in June from 8.7% in May; while local government spending continued to soften slightly. Spending by local governments is limited by constraints on the shadow banking system and land sales for funding. We are also discouraged by the reluctance to allow debt defaults, which delays problems short-term but could aggravate problems longer-term.

The correction in China's property market remains the biggest risk in our view, as the sector influences 23% of its GDP according to Moody's Analytics. Positively, measures have been introduced to address the slowdown; including easing home purchase restrictions (HPR), as well as some Shanghai lenders giving discounted mortgage rates for the first time since early 2012. Additionally, prior home price declines are attracting buyers and improving sales. However, we don't expect construction to reaccelerate, as the surge in property inventories could take a year to consolidate before developers feel compelled to begin new builds.

Chinese property developer stocks shrug off downturn

Source: FactSet, Shanghai Stock Exchange . As of July 28, 2014.

Interestingly, despite the downturn in the property market, the Shanghai Property Index was moving sideways until the recent rebound. We've also witnessed strong returns in the broader Chinese equity market, with the H-share index that trades in Hong Kong entering bull market territory, up over 20% from the March 20 low; validating our thesis that Chinese stocks were pricing in a lot of future negative news, as noted in our Investing Idea, "Why New Reforms Make Chinese Stocks Attractive."

Chinese policymakers remain committed to reform, particularly in the financial sector. Markets have been buoyed by a pilot for a cross-border stock exchange link called the Shanghai - Hong Kong Stock Connect (SHKSC), or "through train," that would allow local Chinese to invest in Hong Kong, and vice versa, as soon as October. Additionally, Chinese stocks tend to perform better in the second half of the year as stimulus is typically enacted to meet full-year growth targets; and stocks are trading near 10-year low valuations. We believe the risk/reward is favorable for owning Chinese stocks within a market weight to emerging market (EM) stocks.

Read more international commentary at www.schwab.com/oninternational.

So what?

Although Wall Street and other corners of the business and political world may empty over the next few weeks, risks of a pullback in U.S. equities have gone up. Although we believe it would represent a buying opportunity and are optimistic longer term due to improving economic growth, nervous investors may want to consider a hedging strategy. China's stock market performance has improved and we remain positive, while European economic data has been more concerning, although the stocks still look attractively valued in our view.

© Charles Schwab

www.schwab.com