Highway drivers who shift lanes when traffic slows rarely get home faster. Likewise, investors who try to time market moves don’t improve returns with any consistency. Rebalancing to thoughtful asset allocation targets is the best way to keep your portfolio in the fast lane.

Summer has arrived and with it road trips to graduations, weddings and vacation spots. Over the past two months, I have traveled the major interstates along the Eastern seaboard from Maine to Virginia, which has given me plenty of time to reflect on the driving patterns of those around me as well as my own tendencies. When the traffic in my lane slows, I have sometimes given in to the temptation to change lanes, hoping to regain speed and shave time from an eight (or 12) hour drive. Yet, without fail, after a few minutes I notice the lane I left is now speeding up, my new lane has slowed down and as I glance to my left or right I see the same cars I did before I became an “active” lane changer. I quietly chastise myself, pick a lane and stay there.

LOOKING FOR THE FAST LANE

There are a lot of parallels between lane changing in search of speed and tactical market timing in search of higher portfolio returns. Most drivers are anxious to arrive at their destination and are not traveling slowly in order to take in the sights. Most investors want to maximize returns. The temptation to be in the “right lane at the right time” can be overpowering because we know that, if our timing is good, we can shorten our trip. Likewise, shifting back and forth from stocks to bonds can enhance return — if we time it right. Yet the efforts of many other drivers attempting exactly the same thing makes it hard to actually get home sooner with frequent lane changing.

Likewise, the activity of many other investors trying to outmaneuver the market and each other makes it very difficult to boost our returns through market timing with any degree of consistency.

FIGHTING THE URGE TO SHIFT EXPOSURES

Today, investors may look at the market and feel an urge to shift lanes, lightening up equity exposure and tactically moving into bonds. This urge may in fact be a strong one. After all, the U.S. equity market has recently climbed to an all-time high. The S&P 500 Index is up over 180% since the post-financial-crisis low in March 2009. And stocks have risen steadily without a meaningful correction for nearly three years. Is the market reflecting a goldilocks economy and calm geopolitical waters? Will stocks keep climbing, even absent stronger personal income gains, employment growth and durable expansion in corporate profits? We think not.

In fact, economic and geopolitical risks abound and stocks seem to have priced in a world of good news with little room for disappointment. No market goes straight up forever and we think it’s entirely reasonable to expect an equity market correction of 10% to 20% sometime during the next 12 to 18 months. In fact, we believe CBIS participants should plan on one. Yet our advice remains the same: Don’t try to predict when a correction will occur. Avoid the temptation to change lanes and stray from your long-term asset allocation policy targets. Instead, prepare yourself emotionally and financially for an equity market correction and make decisive plans to address market volatility through a disciplined rebalancing policy.

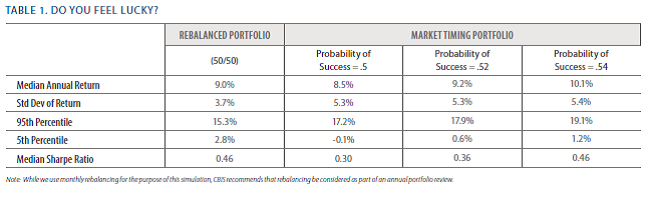

DO YOU FEEL LUCKY?

Our advice may seem unadventurous and even fatalistic. After all, many investors feel certain they have a good read on the markets and confidence in their convictions. Isn’t this the perfect time to express a bearish view? In an attempt to address this question, we reviewed the history of large market movements and simulated the “success rate” required to generate performance in excess of an investor who follows a disciplined rebalancing policy.

Since 1950, there have been 20 instances when the S&P 500 Index experienced a peak-to-trough decline of more than 10%. The average was 28%. Obviously, side-stepping these drops would lead to significantly higher long-term portfolio gains. The odds of picking market peaks and troughs, to the month, are admittedly very low. However, what if we enlarge the timing window to six months? Could an astute investor see a peak forming, exit six months ahead of time, then re-enter the market six months after the bottom?

While most would agree the ability to forecast market declines of 10% or more within a six month window would be deemed prescient, instead of avoiding a 28% decline this investor would have avoided a 3.4% average gain! This “lucky” investor, while correctly predicting a market decline of more than 10%, without perfect timing would have missed an average increase of 3.4%. In addition, this investor would have missed out on a market gain 60% of the time. Without perfect timing, one can be right and still be wrong!

A BROADER LOOK AT THE NUMBERS

A sample size of 20 periods is admittedly small, so we ran a statistical simulation to see just how successful a market timer would have to be to outperform a disciplined investor who rebalances. We simulated 5,000 five-year holding periods and compared the returns from a 50% equity/50% cash portfolio rebalanced monthly with a market timing portfolio shifted between 100% equity and 100% cash, with different probabilities of success. The summary statistics from

the simulation are shown in Table 1.

An investor who engages in timing with a 50/50 chance of success each month significantly underperforms, on average, the rebalanced portfolio — while experiencing higher volatility

and significantly more down-side risk (measured by the 5th percentile of annualized returns). The median returns from market timing are not greater until the success rate exceeds 52% (a very high rate over such a large sample size), yet the distribution of returns is still more volatile with lower returns in the tails. Not until the market timer’s success rate exceeds 54% does the additional return compensate for the additional volatility, as measured by the median Sharpe Ratio. Combined with the fact that market prices are determined every second of every day by market participants, all of whom are looking to gain an edge, a success rate of 54% would be very difficult to achieve.

AVOIDING TEMPTATION

The results of successful market timing and the strength of our occasional convictions that “this time I’ll be right” make it tempting indeed. Yet the odds of consistent success are very low and the risk of failure and painful down-side surprise is high. Even though CBIS anticipates a market correction of 10% to 20% over the next 12 to 18 months, we do not recommend that participants deviate from well-considered long-run asset allocation targets. Prepare instead to address volatility by rigorously following a rebalancing policy. This is the best way to capitalize on volatility while reaching your financial goals at maximum speed.

© Christian Brothers Investment Services