This Big Picture special report investigates the use of the Cyclically-Adjusted Price-to-Earnings Ratio (CAPE) for the S&P 500 to assess the relative over- or under-valuation of the U.S. Market at present.

The CAPE, popularized by the 2013 Nobel Prize winner in Economics, Yale professor Robert Shiller in his (excellent) book Irrational Exuberance, divides the index’s present price by its average earnings over the previous 10-year period. Present CAPE values are knocking against historic high levels, leading some to believe that a market fall is near. This report explores why the CAPE is important and what it is saying about the future of the U.S. market.

All information provided herein is for information purposes only and should not be considered as investment advice or a recommendation to purchase or sell any specific security. Security example features are samples for presentation purposes and are intended to illustrate how to use YCharts data in the analysis of the valuation of public securities. While the information presented herein is believed to be reliable, no representations or warranty is made concerning the accuracy of any data presented.

Executive Summary

- The Cyclically-Adjusted Price-to-Earnings Ratio (CAPE) is bumping up against values that have previously preceded major market declines. Some observers take this to mean that a crash is imminent, but the real story is more nuanced.

- Price-to-earnings ratios—the CAPE included—are a shorthand way of expressing expectations for future earnings growth.

- CAPE’s implied growth rates were a fairly good estimator of future growth before the Great Depression and War Years, but have consistently underestimated actual earnings growth in the post-War period.

- Future growth rates as implied by the present CAPE value signify the market believes the U.S. economy will perpetually grow at the same average rate it has in the post-War period.

CAPE: A Brief Overview

The PE Ratio, as commonly used, has numerous issues which make its applicability for investing questionable. The most serious problem with the PE ratio brought up by Shiller in his best seller, is that a single year’s worth of earnings is too small of a window to get a true view of the power of a firm to generate profits over time. This inadequacy is due to a myriad of factors, including problems of accounting timing and cyclical changes to profitability. To correct for this “small window†issue, Shiller provides a statistic that has since come into common use in the financial industry: the cyclically-adjusted price-to-earnings ratio or CAPE (also sometimes known as the “Shiller PE†or “PE10â€).

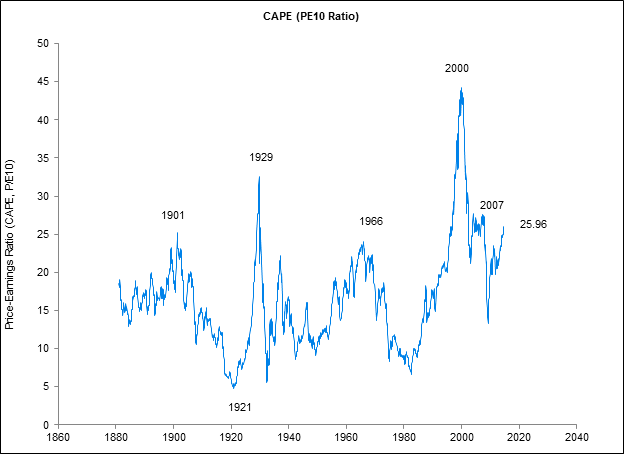

CAPEs are calculated by dividing the present price of a stock by the average earnings of that company over the previous 10-year period. In his book, Professor Shiller adjusts the prices of U.S. stocks and their earnings by inflation, and builds an historical series of the CAPE for the U.S. index starting in 1881. The charted data, which is available on YCharts or through Professor Shiller’s own website, is shown in Figure 1:

Figure 1. Source: Robert Shiller

Even casual observers’ eyes’ will be drawn to the two dates 1929 and 2000; it is also noteworthy that the present CAPE value of 25.96 is close to the 2007 value and is well above the historical average value of 16.6.

Professor Shiller is a skilled economist, well-versed and expert in the use of statistics to draw causal connections, and in his book, he draws a nuanced, measured conclusion from his study of the index CAPE numbers.[1]

How Not to Interpret the CAPE

Unlike Professor Shiller, Wall Street is not known for nuance, measured prognostication, or appropriate use of statistics, so various pundits look at Figure 1 and make the following argument without hint of reservation or doubt:

While this syllogism is valid, it might not be true. Financial ratios do not reflect constants of nature[2], so simply because the present value of a given ratio is higher or lower than an historical value of that ratio or a measure of its historical central tendency, holds little meaning.

To assess the importance of the present CAPE level, we must take a closer look at the basic concept of the PE Ratio to see what it is telling us about how market participants view the world.

The PE Ratio as a Shorthand Growth Metric

According to financial theory and common sense, the price of an asset should be directly related to the profit the asset creates for its owners over its entire economic life. That economic life is perpetual for all companies assumed to be “going concerns.†To find the present value of the future earnings of a company in perpetuity, financial theorists use the Gordon Growth Model.

![]()

Equation 1

Where P = Price, E = Earnings, r = the discount rate of the asset, and g = the growth rate of the earnings.

Rearranging this equation, we see that the PE Ratio simply represents a relationship of the discount rate to the growth rate.

![]()

Equation 2

We can rearrange again to solve for the growth term:

![]()

Equation 3

We know the PE ratio of a stock, so to find the implied growth rate, we simply have to know what discount rate (r) to use. There are various ways of determining what a reasonable discount rate should be, but this author’s personal rule of thumb is to discount large capitalization stocks (or the index as a whole in this case) at a rate of 10%.

In essence, this approach looks at the discount rate as a hurdle over which a prospective investment should generate. According to Shiller’s data, the index has returned roughly 10% on average per year over the entire period (starting in 1871), so from an historical perspective, it is reasonable to assume that holding the index will allow one to enjoy returns of around 10%. If we can expect 10% annual returns, we should use that rate to discount future cash flows from similar investments.

With the assumption of a 10% discount rate, all of the terms on the right side of equation 3 are known, so can easily see what future earnings growth rate is implied by a given PE ratio.

Creating a table to calculate the growth implied by a few PE ratios is simple work:

| PE Ratio | 1 / PER | Implied Growth |

| 5 | 20% | -10% |

| 10 | 10% | 0% |

| 15 | 7% | 3% |

| 20 | 5% | 5% |

| 25 | 4% | 6% |

| 30 | 3% | 7% |

This table means that if a stock has a PE ratio of 15, the market as a whole expects its earnings to grow at 3% per year in perpetuity. Since the CAPE uses average earnings over the previous 10 years, a CAPE of 15 means that the market expects that a company (or the index in the case of the S&P 500) will be able to expand its average earnings of the last 10 years at a rate of 3% in perpetuity.

Now that we have a sense for what the CAPE is telling us about future expected growth, let’s go back to the question of whether we should worry about present CAPE readings.

What the CAPE Is Telling Us about Predicted Future Earnings Growth

Before we can link the CAPE to expectations about future growth, we convert Shiller’s real numbers to nominal ones. This is because the 10% discount rate that we mention in the previous section is based on nominal, rather than real growth rates.

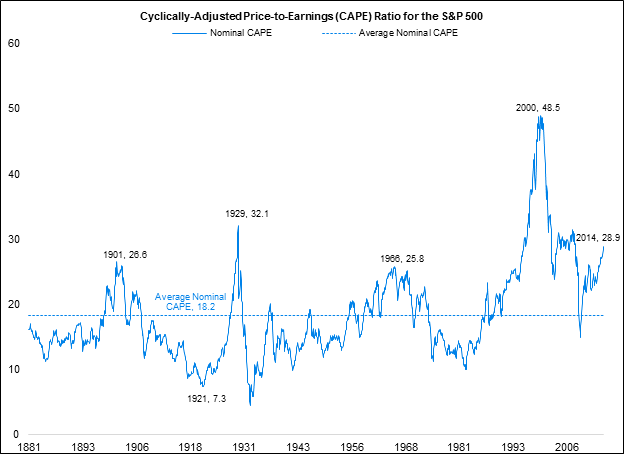

The adjusted CAPE chart in Figure 2 below has the same peaks as the chart in Figure 1, but the line is shifted.

Figure 2. Source: Robert Shiller, YCharts Research analysis

On a nominal basis, the average CAPE over this period—shown in Figure 2 by a dotted line—is 18.2, versus a present value of 28.9.

Next, we use Equation 3 to find that the growth rate implied by these CAPE values.

| CAPE | 1 / CAPE | Implied Growth |

| 18.2 | 5.5% | 4.5% |

| 28.9 | 3.5% | 6.5% |

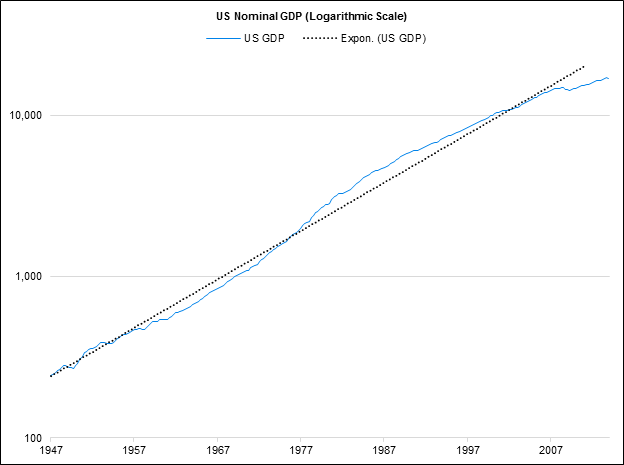

The 6.5% implied growth figure should seem familiar to you. It is, in fact, the average annual growth in nominal GDP in the post-War period (1Q47 – 1Q14) as shown by the slope of the black dotted trend line in Figure 3 below.

Figure 3. Source: Bureau of Economic Analysis, YCharts Research analysis

In short, considering the nominal GDP growth rate shown Figure 3, we can frame the present value of the CAPE as a sign that market participants are—using their capital as voting chits—predicting that the U.S. economy will perpetually grow at about the same rate it has in the post-War period.

CAPE’s Historical Predictive Efficacy

If the market is presently predicting perpetual future earnings growth for the S&P 500 of 6.5%, it makes sense to ask how good a predictor of future earnings growth the CAPE has been historically.

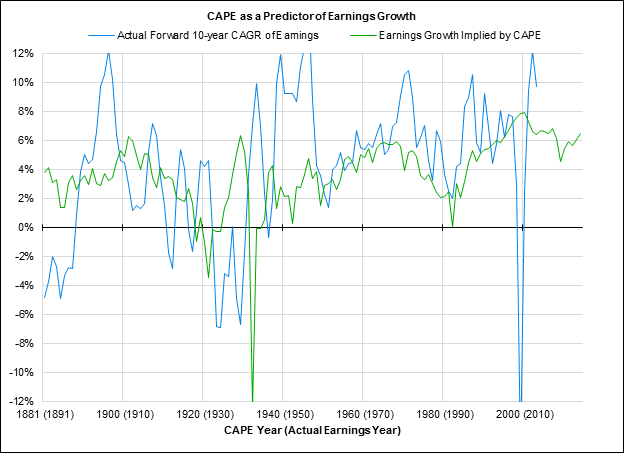

Because the CAPE is an average of 10 years of historical earnings data, we use a forward time period of 10 years and look at actual earnings growth of the index over that period. A graph of these data appear below in Figure 4.

Figure 4. Source: Robert Shiller, YCharts Research analysis (Only one date per year—June 30—for the sake of visual clarity. Extreme values have also been left off the graph for clarity’s sake.)

On the horizontal axis, we list the date on which the CAPE-implied growth ‘prediction’—shown by the green line—was taken. On the same axis, in parentheses, we show the date of the end of the subsequent 10-year period; the actual growth rate of earnings over the intervening 10-year period—the value associated with the date in parentheses—is represented by the blue line.

In other words, the first year for which a CAPE was calculated was 1881. At that point in time, the equity market was pricing stocks as if underlying corporate earnings would grow at a rate of just about 4% per year (green line). In 1891—ten years later—when the actual growth rate was known, earnings had actually fallen by more than 4% per year on average (blue line). This 800+ basis point spread between predicted and actual shows that the CAPE value in 1881 made a very poor prediction of the actual earnings growth rate in the subsequent 10 years.

The blue actual earnings growth rate line ends in 2004 since the 10-year CAGR starting in 2005 cannot yet be calculated. The green implied growth rate line continues on to the present and we can confirm that it presently reads 6.5%.

These lines may seem to be nothing more than squiggles on the page, but splitting the series into pre- and post-War periods, an interesting story emerges.

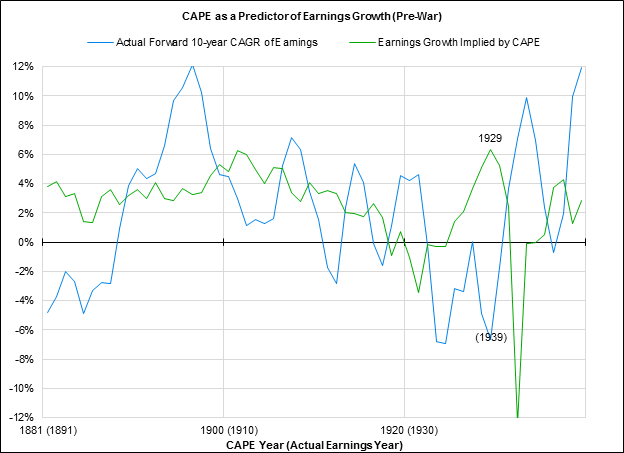

Figure 5. Source: Robert Shiller, YCharts Research analysis

The striking feature of this chart is what a reliable predictor the CAPE turned out to be during much of this period. For instance, the average CAPE-implied growth rate from 1881-1900 was 3.4% and the average actual 10-year CAGR from 1891-1910 was 3.1%—a difference of only 30 basis points.

We see, of course, the 6%+ perpetual growth rate implied by the CAPE in 1929 and note that earnings instead generated an average contraction of over 6% in the following 10 years until 1939, but in general, the blue line seems to vary above and below the green line at roughly equidistant measure. This means that average earnings growth implied (via the CAPE) by market participants was, over time, close to the actual growth rate of earnings.

Over the entire time period shown here, 10-year CAGRs in actual earnings averaged 2.3%. In comparison, the average earnings growth rate implied by the CAPE was 2.5%. Market expectations, on average, slightly exceeded actual growth and actual earnings growth was fairly low.

Let us now compare this pre-War picture with the post-War one.

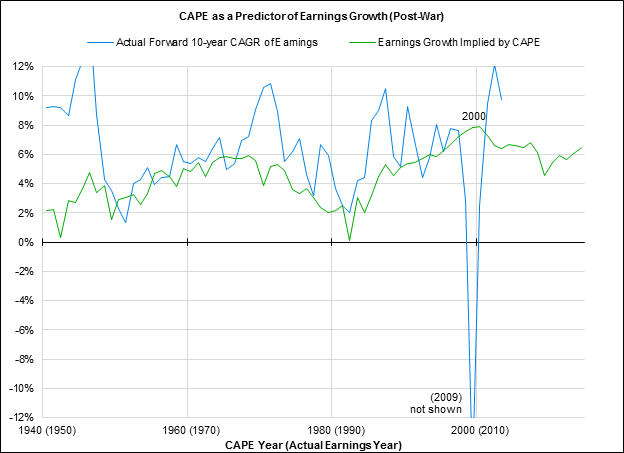

Figure 6. Source: Robert Shiller, YCharts Research analysis

The striking feature of this chart is what a poor predictor the CAPE has generally been during the post-War period—demonstrated by the fact that the green implied growth line is almost always (80% of observations) below that of the blue actual growth line. Average implied earnings growth for the fifty-year period covering 1940-1990 is a measly 3.8% compared to an actual earnings growth rate of 6.5% over this period.[3]

The discrepancy is most marked during the first fifty years of the series. However, beginning around the start of the first Clinton administration, the market looks as though it finally got the 50-year old news flash that corporate profits were growing at a rate much higher than it had been pricing in. Equity prices subsequently inflated (shown by the steadily rising implied growth line) in order to bring implied growth rates closer to the post-War historical average.

The market began to overshoot—as the market is wont to do—and bid index prices high enough to imply perpetual earnings growth of (an irrationally exuberant) 8% per year in 2000.[4] In comparison, actual earnings growth recorded a 10-year CAGR of -15.8% in the years from 1999 to 2009—such an extreme drop that it is literally off our chart.

Over the entire time period shown here, 10-year CAGRs in actual earnings averaged 6.3%. In comparison, the average earnings growth rate implied by the CAPE was 4.4%. Market expectations, on average, materially underestimated actual earnings growth, and actual growth was much more robust than in the pre-War period.

In summary, it does look as though the CAPE was a good predictor of actual earnings growth rates in the pre-War period—doing a fair job of accurately pricing in future, tepid earnings growth. It also looks as though the CAPE was less effective in pricing in actual growth in earnings during most of the post-War period; on average expecting less earnings growth that eventually materialized. This tendency has seemingly reversed itself over the last 15 years, and the market is now pricing stocks as though earnings growth will continue to follow the post-War trend of 6.5% per year growth.

The Big Question

Looking at present value of the CAPE through the lens of projected future earnings growth is a more intelligent way of analyzing the data than the simple syllogism given on page 2. However, it still does not answer the question of how concerned you should be with present CAPE levels.

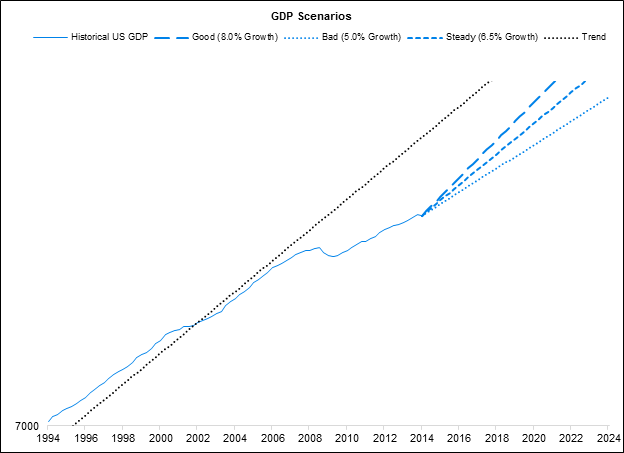

How concerned (or indeed how happy) you should be depends ultimately on your outlook for future growth. The U.S. economy’s growth rate has been below the post-War trend level since 2001, and dramatically so since 2008. Graphically, the three possible scenarios for economic growth over the next 10 years is shown in Figure 7 below.

Figure 7. Source: Bureau of Economic Analysis, YCharts Research analysis

Let’s start with the “Bad†scenario, which we have picked as nominal economic growth over the next ten years of 5%—PIMCO’s “New Normal†outlook, in other words. If the market comes to perceive this scenario as likely, present CAPE values are inappropriately high. This perception would likely force a revaluation of stocks downward and if this revaluation was perfect, it’s magnitude would be on the order of 25%.[5]

In the “Steady†scenario, economic growth follows the post-War trend and expands at roughly 6.5%. If market participants continue to believe this scenario is most likely in the future, growth rates implied by the CAPE are appropriate and the doom-and-gloom crew’s refrain that the sky is falling will not come true.

In the “Good†scenario, economic growth accelerates faster than the historical trend—at a rate of 8% per year.[6] If the market believes this is the most likely future course of the economy, the present CAPE is radically too low and market participants are making the same mistake that we have shown the majority of their post-War predecessors have made. A general shift toward this view would lead to a revaluation of stocks upward by roughly 25%.

Conclusion

While pundits may shriek about the impending market crash on cable business channels, it is clear that the CAPE is not implying unreasonable earnings growth rates vis-Ã -vis recent historical earnings growth. In fact, present levels of the CAPE indicate that most market participants believe that S&P earnings will continue to grow at about the rate they have over the entire post-War period.

While reasonable people may disagree as to whether this is a rational assumption (and if not, what catalyst will force the market to come to the correct conclusion), it is clear that the CAPE is not signaling a precipitous market fall simply because of its present value vis-Ã -vis its historical mean.

DISCLAIMER:

All information provided herein is for information purposes only and should not be considered as investment advice or a recommendation to purchase or sell any specific security. Security example features are samples for presentation purposes and are intended to illustrate how to use YCharts data in the analysis of the valuation of public securities. While the information presented herein is believed to be reliable, no representations or warranty is made concerning the accuracy of any data presented.