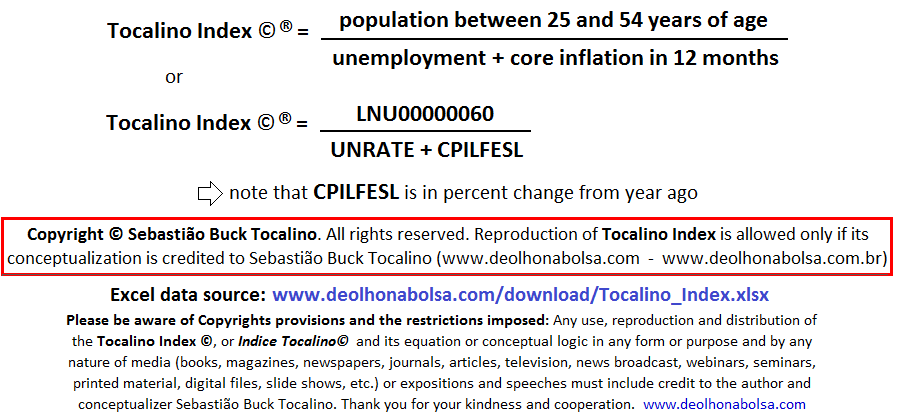

The Tocalino Index: applying Demographics to a variation on Arthur Melvin Okuns Misery

Among the many indicators that track the health of the economy, two are very popular due to the obvious affliction they may inflict on all of us regular Joes and Janes. They are: the inflation rate and the unemployment rate. Between the two of them, inflation is often the most conspicuous. After all, we routinely have to reach for our wallets to pay for our daily needs and those of our children, including education and a variety of goods and services. But, if the unemployment rate is somewhat less followed by those who hold on to a steady job, it is still the most distressing for the less fortunate ones who are out of work!

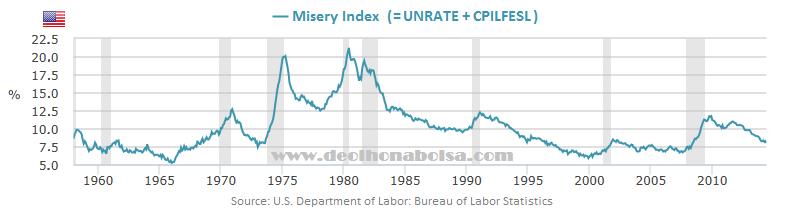

Arthur Melvin Okun was a professor of economics at the famous Yale University, later he was also an important economic advisor to presidents John F. Kennedy and Lyndon B. Johnson. Besides "Okun's Law", another well known contribution of his to the tracking of economic trends was the Misery Index. Its formulation could not be any simpler or more intuitive: it was just the sum of the unemployment rate and the inflation rate. Naturally, to be out of work and having to cope with an escalating cost of life is a sheer disastrous situation leading to social distress, therefore his obvious choice of name for this indicator: the Misery Index!

(Some economists may say that, with a delay of one year or so, this Misery Index, with its implicit social distress, would be a contributing factor to swings in the rate of crimes. I tend to believe that crime is still more related to cultural issues or, more frankly speaking, a considerable lack of culture!)

Personally, I don't usually pay much attention to this index and believe that few people actually do. Though we pay close attention to its two constituents individually. But for some time recently I have been glancing at the Misery Index and its downward trajectory in the US. It is clear that, in spite of all the insane efforts in printing money and keeping real interest rates negative and punitive for the more cautious and conservative majority of savers, inflation is still modest and below the target aimed by the FOMC and the Federal Reserve. By the end of June, the twelve-month inflation climbed a tad higher at 2.07%. Data relative to the closing of July is scheduled to be released only on August 19.

At the closing of June, to the cheers of everyone, the unemployment rate had also fallen to 6.1%. It did rise slightly to 6.2% in July, as reported last Friday.

Trying to avoid much of the noise in inflation data, I will adopt from now on the 12-month core inflation rate, which excludes the more disruptive cost swings of food and energy (due to the villainy of oil prices). The core inflation for the 12 months ended last June was of 1.93%. By using that same month's unemployment rate of 6.1%, the sum has resulted in a 8.03% Misery Index.

At that level, the Misery Index is smaller than all those that were witnessed between 1982 and July of 1996. In that 14-year period, US stocks showed a pretty decent uptrend. But lately, the Dow Jones Industrial Average© has been climbing much higher and steady. In my opinion, already aloof of whatever sound fundamentals could justify such behavior.

Since both unemployment and inflation are contrary to the advancement of the economy, for the next chart I chose to invert the Misery Index. Turning it upside down should make it easier to compare its outline to that of the stock market. The Dow Jones index was adjusted for inflation, so that it represents better the real evolution in terms of purchasing power and cost of life throughout the years. Despite some pretty good coincidence in the timing of peaks and troughs, the Misery Index was still of no help or usefulness in the endeavor of better assessing the precification of stock indices.

As I have written and explained in many occasions, I do pay a lot of attention to the relationship between demographics and the economy. In a different paper I had updated the charts of aggregate annual consumption and the contributing share of households according to the age bracket of the reference person (chief provider for the house and family).

We can see 10 years of compiled data indicating that there is a growing trend of consumption expenditures from early adulthood up to the 45-54 age bracket. Beyond that, general expenditures tend to reverse and shrink with aging. It seems logical then to imply that the economy shall have more impetus with a growing number of 25 to 54-year old people in the population and, vice-versa, less strength as that cohort of the population starts to dwindle.

We may gather that economic advancement is directly proportional to the number of people between ages of 25 and 54 in the US, but inversely proportional to the rate of unemployment and inflation. With this in mind, I set out to calculate the ratio of that total number of people to the sum of core inflation plus unemployment rate, just to find out whatever the outcome would be.

In theory, by proposing and introducing more information and context to the equation, this approach was far more promising and realistic than the old and limited Misery Index created by Art Okun several decades ago.

Inflation is expected and natural, therefore less of a purely malignant distortion, when triggered by an acceleration of the population growth. This represents a physiological increase of demand on consumption. In terms of unemployment, to a certain degree, this may also indicate just some delay in catching up with the growth of the labor force. By calculating the ratio of these three variables, with the population as the numerator and the sum of unemployment plus core inflation as the denominator, it becomes easier to discard any irrelevances and focus better on the relevant trends of these variables put together.

And the results were indeed very interesting:

The relationship between this new indicator (Tocalino Index©, or Indice Tocalino©) and the behavior of the stock market index corrected for inflation seems clear for all to see. The important message here is that it shows the obvious benefit and necessity of taking the demographic profile into consideration when analyzing data that concerns the economy of a country and any reflections of it on the behavior of stock markets.

If the similar behavior of both indices above cannot be neglected nor denied, of course they do not draw a perfect match nor offer infallible clues. A cautionary approach is the golden rule with any economic indicator. And the longer in time the relationship holds on, the more comfortable we may feel to accept it. The restraining factor in producing a longer back history here was the data regarding core inflation, which I could find records only as far back as 1957.

The point that stands out recently is the noticeable gap between the rapid rise of the Dow Jones index and the lagging behavior of my own indicator from 2009 onward. Even if I take into account all the seemingly endless stimuli from the restless Federal Reserve, in my opinion the stock market still seems to be feeding more on some sort of paranoia, or complacency from lack of other investment alternatives, than any demographic, business and economic fundamentals could ever support.

I have no doubt that this matter can generate some heated discussions and a lot of passionate arguments from different people with different perspectives and interests...

Blaise Pascal was not just a great French mathematician, he was also a great philosopher who left us the generous legacy of his own wisdom. From so many of his rich thoughts, one shall always help us to keep an open mind:

"Nobody is so ignorant that has nothing to teach. And nobody is so wise that has nothing to learn."

For those who wish to dig into the simple equation and all its historical data (population, unemployment and core inflation) I offer my own Excel file for download and inspection at: www.deolhonabolsa.com/download/Tocalino_Index.xlsx

Please be aware of Copyrights provisions and the restrictions imposed: Any use, reproduction and distribution of the Tocalino Index©, or Indice Tocalino© and its equation or conceptual logic in any form or purpose and by any nature of media (books, magazines, newspapers, journals, articles, television, news broadcast, webinars, seminars, printed material, digital files, slide shows, etc.) or expositions and speeches must include credit to the author and conceptualizer Sebastião Buck Tocalino. Thank you for your kindness and cooperation!

Copyright © De Olho Na Bolsa (www.DeOlhoNaBolsa.com). All rights reserved.

This is not an investment recommendation! Data gathered here came from other accredited sources that we believe to be reliable, trustworthy, reputable and accessible to market participants.

De Olho Na Bolsa does not suggest buying or selling any stocks, bonds, derivatives or equities. We are not licensed to provide professional advice or strategies for trades, ventures and businesses. We hold no responsibility for whatever decisions may be made based on data, opinions and information gathered here.

INVESTMENT DECISIONS INVOLVE RISKS! For your safety we do suggest you get the professional advice and guidance of a reputable brokerage firm and portfolio manager. They shall be able to assist you in the process of decision making in trades and equity markets.