“Overall, it is hard to avoid the sense of a puzzling disconnect between the markets’ buoyancy and underlying economic developments globally.”

- Bank for International Settlements, 84th Annual Report, June 2014

Dear Client,

Even after a second quarter rebound, gross domestic product (GDP) growth is barely positive for the first half of 2014. That has not stopped the S&P 500 from climbing to new highs. In fact, GDP growth has been weak for the entire “recovery” and, while improved, corporate sales and earnings also leave something to be desired. Stock market returns look better still, but only when compared to these weak results. Looking over a longer timeframe, the US equity market is approaching fifteen years of low single-digit returns.

Despite the unfriendly environment, US entrepreneurship remains strong and there are pockets of very robust secular growth. We even think there are a few bargains to be found in an equity market at all-time highs. We discuss those topics, as well as the challenge of GDP forecasting, signs of trouble in securities markets, and portfolio adjustments below.

First, here is the performance table for the Grey Owl Opportunity Strategy as of June 30, 2014[1]:

| Q2 | YTD | TTM | Cumulative Since 10/06 Inception | |

| Grey Owl Opportunity Strategy (net fees) | 1.55% | 7.19% | 15.38% | 63.83% |

| Spider Trust S&P 500 (SPY) | 5.16% | 6.95% | 24.40% | 66.97% |

| iShares MSCI World (ACWI and MXWD) | 5.09% | 6.04% | 23.20% | 46.49% |

A Quick Review of the Past (Almost) Seven Years

The Bank for International Settlements (BIS) recently weighed in on the state of the global economy, markets, and central bank intervention. The organization published its 84th Annual Report[2] in June.

The report is relatively informative, grounded in sober reality, and presented in a straightforward manner (unlike much of the commentary out of the US Federal Reserve which can be incredibly difficult to parse). A few quotes from the overview sum up the report and largely match our view of the world. The emphasis is ours.

“The global economy has shown encouraging signs over the past year. But its malaise persists, as the legacy of the Great Financial Crisis and the forces that led up to it remain unresolved.”

“By mid-2014, investors again exhibited strong risk-taking in their search for yield: most emerging market economies stabilized, global equity markets reached new highs and credit spreads continued to narrow.”

“Overall, it is hard to avoid the sense of a puzzling disconnect between the markets’ buoyancy and underlying economic developments globally.”

Within the report, several data points about the US economy are worth highlighting: [3]

· US real GDP is up a mere 5.9% from its 2007 peak

· US employment level is still lower than the 2007 peak – by -0.8%

(Note: this is the number of employed people, NOT the unemployment rate which is more frequently referenced)

· Gross debt in the US is up 42% over the same period

From our perspective this paints a pretty clear picture. Despite a significant increase in debt levels, growth has been very slow (more on this later). Because of the significant increase in debt levels, the foundation for future growth is wobbly.

Turning to Howard Silverblatt’s S&P 500 Earnings and Estimate Report, we get a picture of corporate sales and earnings growth. The last cycle peak for per share[4] quarterly earnings occurred in the second quarter of 2007 (at about the same point that GDP peaked). From that quarter through the first quarter of 2014:

· Sales grew 9.5%

· Operating earnings grew 13.6%[5]

While economic growth was slow over the past seven years, corporations were able to extract a bit more out of the topline and still a bit more out of the bottom line. Businesses have done yeoman’s work navigating a difficult environment and squeezing every last ounce of value out of both labor and assets. Corporate executives have creatively worked to lower their tax burdens. They have taken advantage of low interest rates to refinance debt. In other words, they have done everything they can to increase profitability. Looking forward, with profit margins at historically high levels and tax and interest expense at historically low levels, how many more levers can corporations pull?

Equities have performed better still. Our guess is this is mostly due to a “Pavlovian” response to low interest rates supplied by the Federal Reserve. None-the-less, and somewhat amazingly given the challenging environment and the increased risk associated with increased leverage across the entire system, the S&P 500 is up 20% from its 2007 peak. Yes, multiples have actually expanded since 2007![6]

Yet, despite recent strength, US equities have provided meager returns for almost a decade and a half. Updating the graph from our fourth quarter 2013 letter, it is clear that the last fourteen and a half years still show the S&P 500 providing “equity-like volatility with fixed income returns.” Since the beginning of 2000 through the second quarter of 2014, the annualized total return for the S&P 500 index has been just 3.95%. In order to achieve this skimpy return, investors had to suffer through two 50%+ peak to trough declines. This is compared to the 9.55% compound annual return achieved from 1928 – 2013.[7] Something much closer to the magic 10% equity investors still seem to expect.

Figure 1 - The S&P 500 has compounded at 3.95% for the last fourteen and a half years, suffering two 50%+ drawdowns in the process. Source: Bloomberg.

Secular Growth in a Low-Growth World – EBAY

While the overall economy’s slow growth presents an investment headwind, there are still opportunities. Of course, sales growth is not a prerequisite for investment success. Plenty of people have gotten rich buying depleting assets like oil wells. Price paid is always the determining factor. But, secular[8] growth has its merits, particularly in a world where growth is scarce. A growing company with a competitive business advantage can reinvest capital at a high rate. Owners can compound their return rather than continually look for the next place to put the proceeds of their royalty stream (to use the oil well analogy again).

Two of the most powerful secular growth trends today are the shift from offline retail to e-commerce and the shift from physical currency to cashless transactions. eBay (EBAY) is well positioned to take advantage of both of these trends.

The first half of this year was full of noise and distractions for EBAY: publicly hostile correspondence with activist investor Carl Icahn (who did make some good points), a security breach that forced a system-wide password reset, and a new algorithm from Google that had a detrimental impact on search results for eBay listings. Despite these challenges, EBAY grew Enabled Commerce Volume (ECV) 26% year over year in the second quarter. This is up from 20% in the first quarter of 2013. And, it is significantly better than the already strong growth in ecommerce. The US Census Bureau estimates ecommerce grew 15% in the first quarter compared to 2.4% for all retail sales.[9]

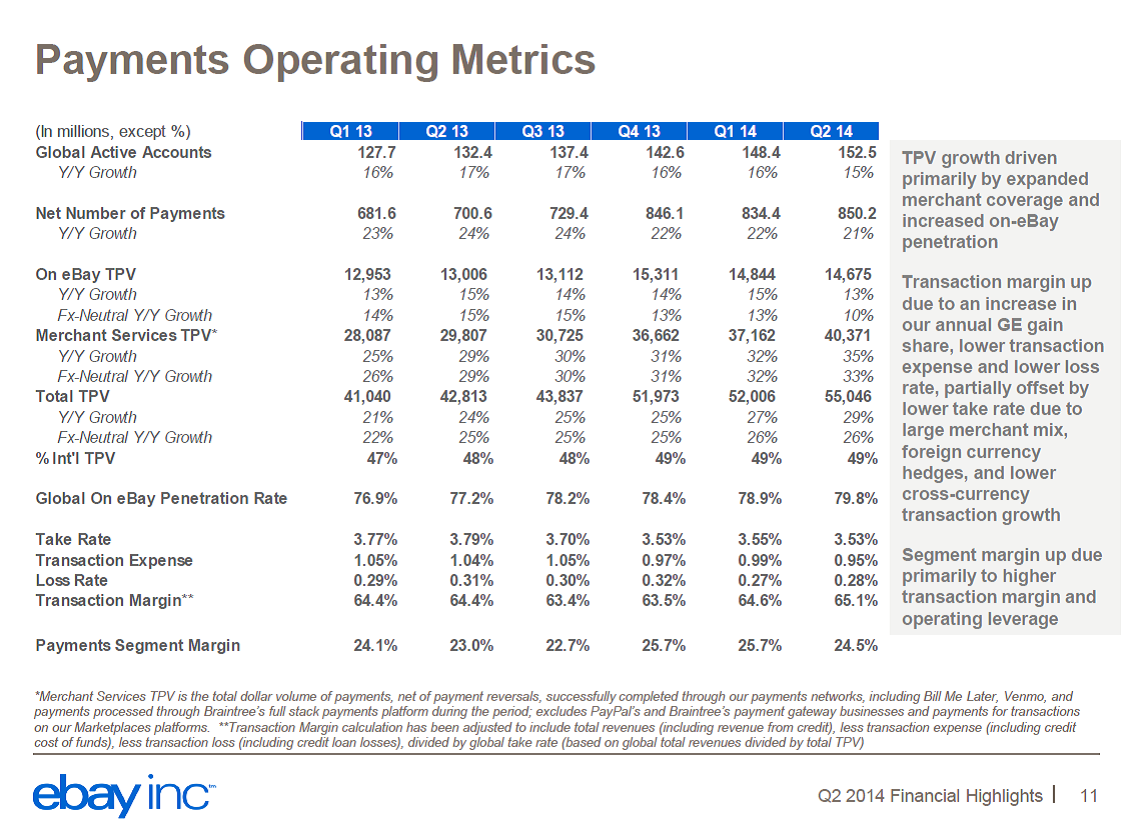

While EBAY’s company-wide trends are strong, PayPal’s trends are even stronger. Every single metric is solid, but we are particularly excited to see Merchant Services Total Payment Volume growing at an accelerated rate – from 26% year over year in the first quarter of 2013 to 33% in the second quarter of 2014. This tells us that PayPal is NOT just being used within eBay’s Marketplaces. More and more, it is being used across ecommerce (and even offline) to facilitate payments.

![]()

Figure 2 - EBAY's payment metrics slide from their Q2 2014 earnings call shows strong growth in merchant services TPV.

We first discussed our eBay (EBAY) position in our third quarter 2013 letter. At the time of that letter, EBAY shares traded just above $50. We wrote, “We initially purchased eBay (EBAY) shares in December 2011. At the time, eBay was unloved trading at 18x 2011 earnings per share and just 12x 2012’s prospective earnings. Since then, eBay’s shares have returned over 75%, but that return was all in 2012. Shares have been flat throughout 2013.” It is now nine months later and we can add, shares were flat for all of 2013, as well as the first two quarters of 2014. In other words, our EBAY investment has not produced results for six quarters. However, intrinsic value has grown significantly. This is the more important metric for the long-term investor.

While the economy is growing at low-single digit rates, EBAY’s industry (ecommerce) is growing in the mid-teens, and EBAY’s participation in this industry (it’s ECV) is growing in the mid-20s. Yet, EBAY trades at the same multiple as the S&P 500. With the S&P 500 at all-time highs and growth scarce, there are few bargains. We think EBAY is one.

How important is GDP forecasting?

Legend has it, Charlie Munger[10] admitted to spending five minutes a year thinking about macro-economics. He also says those are five wasted minutes. Many value investors took that approach and totally missed the 2007 housing bubble. Further, they compounded their error by investing in financial companies that looked cheap based on traditional value metrics after stocks had sold off, but well before several large bankruptcies. Most value investors now admit it is important to spend some time understanding the bigger macro-economic picture. After all, stock market corrections often coincide with recessions. Unfortunately, it has been near impossible for “experts” to predict GDP growth rates and it may be getting harder still. Rather than trying to predict the next quarter, year, or exact turning point, we think it is more important to understand the general environment and to be aware of the buildup of excesses.

Predicting GDP growth is incredibly difficult. In his terrific book, The Signal and the Noise, author Nate Silver describes the historical fallibility of economic growth forecasts that come out of the Federal Reserve Bank of Philadelphia’s Survey of Professional Forecasters. One might suppose that this group is the “best of the best” as far as this type of economic prediction is considered. Still, the November 2007 forecast for the year 2008 indicated a 2.4% expected growth rate for 2008. As we now know, the actual outcome was -3.3%. The inaccuracy is not limited to 2008. In fact, it appears systemic. Silver cites a study that found the economists’ predictions fell outside of a 90% probability interval half of the time since the survey began in 1968. Silver writes, “There is almost no chance that the economists have simply been unlucky; they fundamentally overstate the reliability of their predictions.” Said differently, the organization (the Federal Reserve) that most relies on GDP forecasts to “steer” the economy on our behalf is pretty lousy at GDP forecasting.

What was challenging work prior to the massive monetary and fiscal interventions begun by the government in 2009 and continuing through today, has perhaps become impossible. In an October 2013 piece titled When Economic Data Is Worse Than Useless, investment manager John Hussman lays out the case that indicators that were positively correlated with subsequent economic activity in past cycles have become negatively correlated with subsequent economic activity in the current cycle. He describes the phenomenon this way:

“Normally, the dynamic runs something like this: leading economic measures deteriorate; the economy subsequently deteriorates; leading economic measures improve; and the economy subsequently improves. The result is a positive correlation between leading measures and subsequent activity.

In contrast, the recent dynamic runs something like this: leading economic measures deteriorate; the Fed responds with some massive intervention that is unprecedented in scale; economic activity and leading measures temporarily improve; but since these improvements were entirely artificial, the improvement is quickly followed by fresh deterioration in both economic activity and leading measures. The result is an inverse correlation between leading measures and subsequent activity.”

So, while we profess no ability to predict GDP from quarter to quarter or year to year, we do know that the current recovery has been weak by historical standards. The long-term real GDP growth trend is 3.5% including both booms and busts. Real GDP grew at 2.25% for the four year period from 2010 to 2013 – i.e. the current “boom.” Given current debt levels, low growth is likely to continue for several years (but it is not necessarily a multi-decade phenomenon).

So what’s the deal with 2014 GDP?

First quarter GDP was negative, but as of Wednesday July 30th’s strong first estimate of second quarter GDP, it looks like the US economy continues to grow at a modest pace. Everyone should be prepared for significant revisions to the second quarter number, so it is still very difficult to tell where things stand.

The first estimate at GDP is released one month after the quarter ends. It is then revised many times over the next few months and then less frequently over the next few years. That first estimate is more like a “guess” and it often winds up being as inaccurate as the forecasts that precede it.

With the three most meaningful revisions behind us, we now have what should be a reasonable picture of first quarter 2014 gross domestic product (GDP). The economy shrank 2.1% in the first three months of 2014 compared to the fourth quarter of 2013. To put that into context, this is only the second time since the recovery began in the second half of 2009 that GDP shrank from one quarter to the next. In the first quarter of 2011, GDP shrank 1.3%. It then quickly bounced 3.2% in the second quarter. Expectations were for a similar bounce in second quarter 2014. Leading into Wednesday’s first estimate, Bloomberg consensus for second quarter growth was 3.25%.

Contrary to the consensus however, some early data showed the second quarter number had the potential to surprise to the downside. Economist Gary Shilling tweeted on June 26, “Real consumer spending -0.1% in May after -0.2% in April. Consumption is 70% of GDP. 2Q GDP could be negative after -2.9%[11] 1Q. A recession?”

Yet, there was logic to the consensus’ more bullish argument. One of the 78 contributors to the Bloomberg consensus is Barclays. Explaining their 3% estimate (down from 4% earlier in July and very close to consensus) in the July 18 “Barclays Global Economics Weekly,” they argued that June’s retail sales numbers and the upward revisions in April and May’s numbers showed core (i.e. excluding auto) retail sales growing at a 6.7% quarterly rate – the strongest reading in three years.

Frankly, prior to Wednesday July 30, when the first estimate of second quarter GDP was released, we had no clue whether the consensus or skeptics would prove correct. As it turns out, the “advance estimate” for second quarter GDP came in at a consensus-beating 4%. As the Wall Street Journal stated, “An upturn in inventory building by businesses and an acceleration in consumer spending led the broad gains…”

None-the-less, the picture is probably still murky. Revisions can be large. Remember, the current estimate of -2.1% for the first quarter began as 0.1% growth when the first, “advance” estimate for Q1 was released in late April. It then went all the way down to -2.9%, before the third and most recent revision “increased” it to -2.1%.

The bottom line is it is hard to know where the economy stands. Clearly, it has been supported by never-before-seen government intervention – both fiscal and monetary. Debt is at dangerous levels. We continue to believe that a portfolio designed to perform well in any environment at the expense of performing exceptionally well in a specific environment is the correct choice. The economy could move from slow growth to recession given the strains on the middle-class consumer. It could also accelerate. There is evidence the private sector has more than taken up the slack of reduced government spending. Increased business investment could lead to jobs and wage increases in a pro-cyclical manner. On the inflation side, any pick up in bank lending could unleash the gigantic, Federal Reserve-created monetary base and set off inflation. But, the debt overhang could overwhelm borrowers and lead to deflation. An “all-weather” portfolio is required.

Increasing Divergence within Securities Markets

Perhaps some parts of the market have become skeptical of the economic picture and valuations are beginning to weigh on securities. Or, perhaps the threat of quantitative easing (QE) ending within the next few months is starting to sink in.

While the S&P 500 continues its steady rise, there are waves beneath the surface. Market corrections never occur all at once. Typically, other sectors and asset classes lead the more “staid” large capitalization indices on the downside. Note – we are not calling for a market sell-off, just pointing out that some internal divergences are starting to develop.

The small capitalization Russell 2000 index is flat for the year, while the S&P 500 is up approximately 8%. The Russell 2000 is made up of more speculative names. This could be signaling investor unease and a shift to relative quality.

Figure 3 - The small capitalization Russell 2000 index is flat for the year.

Likewise, high-yield (“junk”) bonds are barely positive. Some analysts believe this is directly related to the Federal Reserve threatening to remove liquidity and/or raise interest rates. Corporations have been able to improve their cash flow by continually refinancing debt burdens at lower interest rates. If this game is up, credit quality may erode.

Figure 4 - JNK is the high-yield debt ETF. It is barely positive for the year. Some analysts speculate that this signals the end to the debt refinance boom and corporate balance sheets will soon be under pressure.

Portfolio Adjustments

Similar to last quarter, we made modest portfolio adjustments during the most recent three month period. On the buy side, we added to our positions in Annaly Capital Management Inc. (NLY), Express Scripts Holding Co. (ESRX), Post Holdings Inc. (POST), and Priceline.com Inc. (PCLN). We described our ESRX thesis in our third quarter 2013 letter. POST and PCLN were the highlights of our last letter.

We have never discussed our NLY position in detail. NLY is a mortgage real estate investment trust (REIT) that currently trades at a discount to book value and offers a current yield close to 11%. Importantly, mortgage REITs typically do well (and outperform US equities) during periods of slow growth and deflation. Given the discount to book and high current yield, we think it is a very inexpensive hedge.

The Vanguard emerging market exchange traded fund (ETF) ticker VWO, was our only new buy during the quarter. Emerging market equities have gone sideways for the past four years. Yet, earnings are growing at a faster rate than US equities’ earnings and they trade at a lower multiple. To top it off, emerging market equities typically outperform US equities in inflationary environments. It looks like another cheap hedge to us.

On the sell side, we sold the final stub of our World Wrestling Entertainment (WWE) position. We also closed out long-held positions in Novartis AG (NVS) and Pfizer Inc. (PFE), deciding to focus our healthcare investments in ESRX, Laboratory Corporation of America Holdings (LH), and Valeant Pharmaceuticals International, Inc. (VRX) where we see greater upside.

We also chose to sell the National Oilwell Varco, Inc. (NOV) spinoff NOW Inc. (DNOW) when it began trading in early June. We were enthusiastic supporters of the spinoff. It was yet one more example of exemplary capital allocation decision-making by NOV’s management team. We also think DNOW will be a terrific standalone company. Yet, in the mid-$30s, DNOW was pricing in margin expansion from 6% to 8% and almost $1B in accretive acquisitions. Both reasonable expectations, but they will require significant execution and they are already priced in the stock. We continue to hold NOV and are excited by their core business as well as the opportunity in floating production storage and offloading (FPSO) ships.

Conclusion

Our posture remains balanced. The economic recovery has been weak, but it continues to improve. The foundation is built on significant government intervention. The footings are therefore weak. Asset class valuations are high across the board. However, nothing is so out of balance that a bet on a single outcome makes sense.

As we wrote last quarter:

“In addition to our portfolio of selective equities, we hold cash and gold (and longer dated Treasury bonds in our fixed income accounts and partnership) in an effort to create an “all-weather” portfolio. As we have repeatedly written, the current level of government intervention, both fiscal and monetary, has served to smooth volatility in the short-term, but this is at the expense of significantly increasing long-run volatility. We continue to structure portfolios in a way that will enable them to perform well whether the economy grows or shrinks and whether we experience inflation or deflation.”

*****

As always, if you have any thoughts regarding the above ideas or your specific portfolio that you would like to discuss, please feel free to call us at 1-888-GREY-OWL.

*****

Sincerely,

Grey Owl Capital Management, LLC

This newsletter contains general information that is not suitable for everyone. The information contained herein should not be construed as personalized investment advice. Past performance is no guarantee of future results. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock market involves the potential for gains and the risk of losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security. Any information prepared by any unaffiliated third party, whether linked to this newsletter or incorporated herein, is included for informational purposes only, and no representation is made as to the accuracy, timeliness, suitability, completeness, or relevance of that information.

The securities discussed above were holdings during the last quarter. The stocks we elect to highlight each quarter will not always be the highest performing stocks in the portfolio, but rather will have had some reported news or event of significance or are either new purchases or significant holdings (relative to position size) for which we choose to discuss our investment tactics. They do not necessarily represent all of the securities purchased, sold or recommended by the adviser, and the reader should not assume that investments in the securities identified and discussed were or will be profitable. A complete list of recommendations by Grey Owl Capital Management, LLC may be obtained by contacting the adviser at 1-888-473-9695.

Grey Owl Capital Management, LLC (“Grey Owl”) is an SEC registered investment adviser with its principal place of business in the Commonwealth of Virginia. Grey Owl and its representatives are in compliance with the current notice filing requirements imposed upon registered investment advisers by those states in which Grey Owl maintains clients. Grey Owl may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements. This newsletter is limited to the dissemination of general information pertaining to its investment advisory services. Any subsequent, direct communication by Grey Owl with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of Grey Owl, please contact Grey Owl or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov).

For additional information about Grey Owl, including fees and services, send for our disclosure statement as set forth on Form ADV using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

The performance information for the Grey Owl Opportunity Strategy presented in the table above is reflective of one account invested in our model and is not representative of all clients. While clients were invested in the same securities, this chart does not reflect a composite return. The returns presented are net of all adviser fees and include the reinvestment of dividends and income. Clients may also incur other transactions costs such as brokerage commissions, custodial costs, and other expenses. The net compounded impact of the deduction of such fees over time will be affected by the amount of the fees, the time period, and the investment performance. Grey Owl Capital Management registered as an investment adviser in May 2009. The performance results shown prior to May 2009 represent performance results of the account as managed by current Grey Owl investment adviser representatives during their employment with a prior firm. THE DATA SHOWN REPRESENTS PAST PERFORMANCE AND IS NO GUARANTEE OF FUTURE RESULTS. NO CURRENT OR PROSPECTIVE CLIENT SHOULD ASSUME THAT FUTURE PERFORMANCE RESULTS WILL BE PROFITABLE OR EQUAL THE PERFORMANCE PRESENTED HEREIN. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable.

The indices used are for comparing performance of the Grey Owl Opportunity Strategy (“Strategy”) on a relative basis. Reference to the indices is provided for your information only. There are significant differences between the indices and the Strategy, which does not invest in all or necessarily any of the securities that comprise the indices. In addition, the Strategy may have different and higher levels of risk. Reference to the indices does not imply that the Strategy will achieve returns or other results similar to the indices. The performance shown for the iShares MSCI World Index Fund (“Fund”) includes performance of the MSCI World Index prior to March 26, 2008, inception date of the Fund.