For many foundations and individual investors, the usefulness of a portfolio lies in its ability to provide cash flow to support charitable activities or to cover living expenses. Like a wise orchard farmer, investors are looking to harvest apples from the branches without damaging the orchard. These investors place a premium on receiving current income without undermining their ability to receive similar amounts—adjusted for inflation— in the future. The term “sustainable spending” describes a measure of wealth in terms of the real spending that a portfolio can sustain over time. This measure differs markedly from measuring wealth in terms of the market value of a portfolio. This is an important distinction for income-focused investors. This article will explore how dividend is the key to managing wealth in terms of sustainable spending and how global dividend paying stocks, in particular, are a great equity investment for a sustainable spending strategy.

Why Dividend is the Key

Dividend is the key to a sustainable spending strategy for two primary reasons: it is the best metric for determining sustainable spending, and it helps investors “weather the storm”.

Determining Sustainable Spending:

It is crucial to properly calculate a sustainable withdrawal amount. Although most foundations and individual investors focus on a percentage of market value to calculate distributions, we strongly advocate the Global Orchard approach, which is our sustainable spending rate strategy of 130% of dividends. That is, organizations and individuals can increase the probability of sustainable spending through a simple, two-part plan: investors would spend all of their dividends and a portion of their capital equal to 30% of the dividend. The rest of the capital is allowed to grow. A key strength to this approach is that dividend income makes distribution calculations relatively straightforward. Just as important, there is too much risk of overspending when basing distributions on a percentage of market value since stock prices can fluctuate widely.

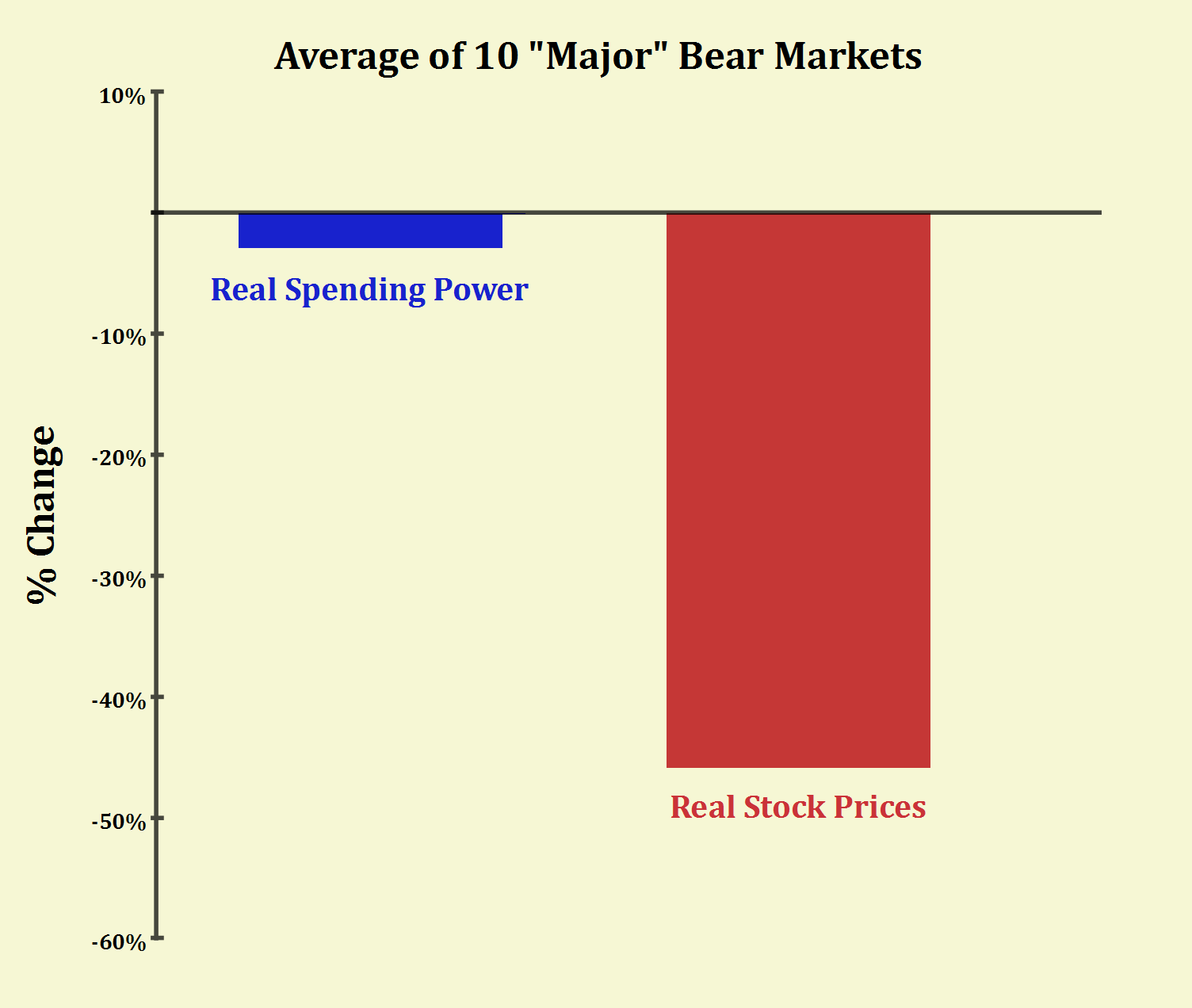

The following chart summarizes the results of the last ten “major” bear markets. For the purposes of this article, “major” bear markets are defined as markets that declined by more than 30%. Of these bear markets, on average, real stock prices dropped by nearly half, while real spending power barely changed.

So, an investor with a $1 million portfolio with a 3% dividend yield receives $30,000 a year in income. If that portfolio were to decline in value to $700,000, it is still generating the same amount of cash yield, assuming there have been no changes to holdings or their underlying earnings and dividends. Conversely, if the portfolio value doubled from $1 million to $2 million, the long-term spending power would still not change. In other words, dividends provide stability within the context of our Orchard sustainable spending strategy.

The reality is, while bear market drawdowns dramatically affect wealth in terms of market value, they have little impact on wealth as viewed from the perspective of sustainable spending.

Weathering the Storm:

We believe it is important to distinguish between a lasting loss of capital and a transitory loss of value. It can certainly be difficult for investors to stay the course when times get tough. Investors often abandon sound long-term positions because of their inability or unwillingness to weather the storm, and once assets are sold, they are no longer there to benefit from inevitable recoveries. Income helps investors “weather the storm” in two ways: providing cash so investors are not forced to sell their holdings (liquidity risk) and providing a price floor vies-a-vie dividend yields to protect against ill-timed capitulation (behavioral risk).

Forced Out – Liquidity Risk:

Liquidity risk includes the likelihood that an investor does not have enough cash to sustain spending, even though total assets are sufficient to do so. A portfolio with little or no income has a high degree of liquidity risk, especially from the standpoint of investors interested in spending power. The importance of liquidity cannot be overstated, especially with the new modes of investing. The increasing use of illiquid, non-traditional assets adds further strains on cash resources because private equity capital calls can increase as exit opportunities dry up. This strain on cash resources is further compounded as hedge funds throw up “gates” to limit withdrawals right when investors need cash most. Given the popularity of these types of investments, it is surprising how little attention is paid to liquidity. This is probably because most investors simply assume that they can always sell stocks or bonds to meet cash needs. This thinking could be tactically unsound. A core tenant of investing in illiquid and/or higher risk assets is that in the long run, they will offer higher returns. Of course, for investors to realize the ultimate benefit of the long-term math, they must have the ability to hold their positions long-term. If positions must be sold in the short run to cover cash needs, they would not be held long enough for the mathematical averages to ultimately play out. The following simplified example demonstrates this principal.

| PORTFOLIO A | PORTFOLIO B | |||

| With Dividends | Without Dividends | |||

| Beginning Value | $100 | $100 | ||

| Equity market declines 50% during year 1 | ($50) | ($50) | ||

| Dividend Income In Year 1 | $3 | $0 | ||

| Spending Rate - 5% of beginning value | ($5) | ($5) | ||

| Ending Value - Year 1 | $48 | $45 | ||

| Equity market doubles in year 2 | $48 | $45 | ||

| Dividend Income In Year 2 | $3 | $0 | ||

| Spending Rate - 5% of beginning value | ($2) | ($2) | ||

| Ending Value - Year 2 | $97 | $88 | ||

| Assumptions: | ||||

| 1. Spending is 5% of beginning value, paid at year end | ||||

| 2. Dividends yield is 3% | ||||

| 3. Equity Market declines 50% in year one | ||||

| 6. Equity market doubles in year two. | ||||

Because the investor of Portfolio A had dividends to augment her spending needs, she was forced to sell less of her holdings to sustain her lifestyle. The investor of Portfolio B, however, did not have the benefits of dividends and his portfolio ended up 9% less than his companion after two years.

Capitulation – Behavioral Risk:

Recent experience teaches us that losses have been consistently larger and more frequent than the brightest mathematicians or most prestigious advisors have expected, and seemingly impossible events occur with alarming frequency. The 1987 stock market crash was a 20-standard-deviation event, and the odds of the 1998 Russian debt crisis were 20 million to 1. Understandably, many investors found the disparity between their expectations and experience unnerving, and all too often, this disparity led to ill-timed portfolio changes. The fields of psychology and behavioral finance provide some explanation. Research found that people experience the pain of losses more acutely than the pleasure of gains. As such, when investors experience large losses, there is a tendency to capitulate, and once this occurs, temporary losses in value become permanent losses of capital.

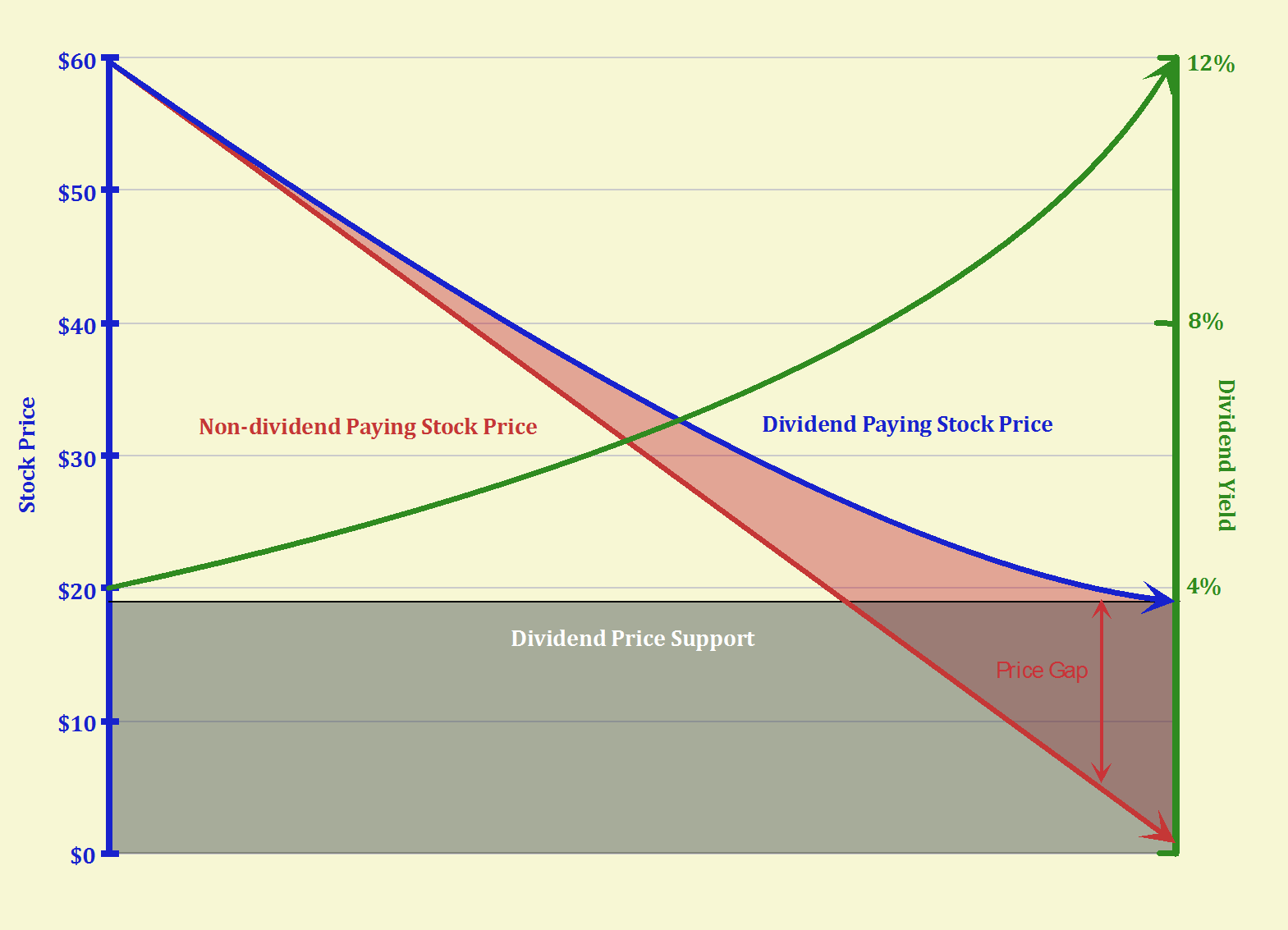

Dividend income provides some protection against this inclination. In our March 12, 2014 “Global Dividend Insights”, we explained why global dividend portfolios lowered volatility and offered protection in down markets. To summarize, the dividend yield creates a price floor as investors seeking cash flow flock to stocks with high yield. The lower the stock price drops, the higher the dividend yield becomes (dividend yield = dividend payment in $/stock price), and the more attractive the stock appears to these investors. As shown in the graph below, the rising yield provides an increasing price gap (distance between blue and pink lines) during falling markets as investors seeking cash flow flock to these stocks. This dynamic effectively creates a price floor, an advantage missing in non-dividend paying stocks. A non-dividend paying stock can drop to zero without much support. However, as stock prices approach zero on a dividend-paying stock, its yield would increase dramatically – a deal too good to pass up. This concept is illustrated in the following graph; where the dividend yield (green line) increases from 4 percent to 12 percent as the stock price (blue line) drops from $60 dollars to $20 dollars.

In rising markets, investors do not have to sacrifice appreciation to gain the benefits of yield. This reality debunks the conventional idea that dividend paying stocks suffer from slow growth. Arnott and Asness [2003] found that high payout rates often precede earnings growth, while low payout rates can be attributable to slower earnings growth. In other words, dividend paying stocks were not necessarily slow-growers with lower upside potential. In fact, that was the exception rather than the rule. Perhaps some companies that do not pay dividends do not generate sufficient free cash flows, or perhaps their business models have large cash burn rates.

Armed with the combination of downside protection and a strategy focused on sustainable spending versus market values, investors are more likely to stay the course.

Why Global Dividend Stocks

While dividend is key, it is global dividend that provides the full benefits of income to the sustainable spending approach. To optimize income generation while minimizing portfolio risks, investors should consider global dividends, i.e. dividend paying stocks on a global basis. Global dividends have the distinct advantage of being everywhere at once; whenever one market in the world thrives, an investor in global dividends reaps benefits even if the investor is halfway across the road. Further, any decline in one market is often offset by a growth in another. In short, a global approach gives investors a larger universe from which to find value and yield. Furthermore, due to different global executive incentive programs, companies in some countries have a greater tendency to opt for dividends as opposed to other forms of returning cash to investors. For example, European companies tend to reward key employees with stocks. The payment of dividends then benefits executives as well as shareholders, making dividend payments just as attractive to executives as they are to dividend investors. American companies, by contrast, tend to reward executives with stock options. In such a situation, executives are keener on the rise of stock prices, making stock buy back an attractive option for executives.

Lastly, with periodic rebalancing and reinvesting income into additional dividend paying stocks after market declines, investors can get a “raise” in annual income. This phenomenon is prevalent among US companies, but is even more common among non-US companies. In 2012, Rob Arnottt claimed that annual income can be boosted about three-fourths of the time: 24 out of 33 years in the United States (73%) and 22 out of 28 (79%) years in the international markets.

Conclusion

For those focused on the spending power of the portfolio, as our Global Orchard strategy advocates, most of the massive market gyrations of recent past were non-events. Stability and resilience are key concepts to the Global Orchard strategy of sustainable spending. For sustainable spending, it is more important to focus on income generation of the portfolio (dividend payments) then the rate of change of the market value. Among other benefits, dividends fortify investors’ cash flow and emotional abilities to weather the whipping winds of storms. In particular, global dividends offer the most benefits because global dividends provide not only a larger universe to find quality but perhaps also higher dividends. In the end, for long term sustainable spending, it is about harvesting fruit without damaging the orchard. Global dividends can act as protective barriers to protect the trees from the whims and violence of the market storms.

© Soledad Investment Management